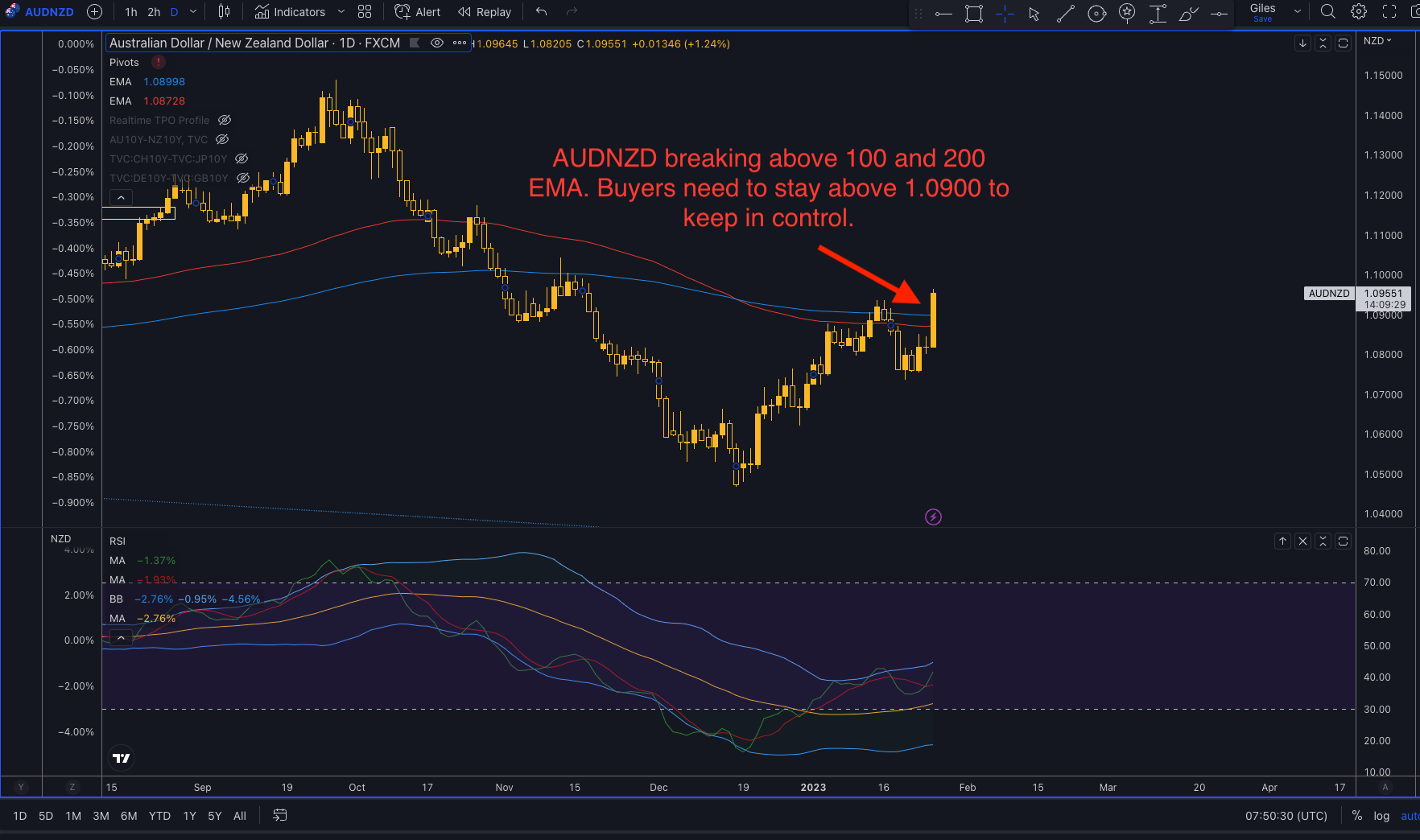

It was Australia’s inflation data this week that raises expectations for a more aggressive RBA. All the inflation metrics beat across the board and both the trimmed mean and weighted median printed above market’s maximum expectations. See here for the prints from Financial Source’s calendar:

The headline figure for Q4 2022 rose to 7.8% from 7.3% in Q3 2022 and this shows a marked increase in inflationary pressures. However, the majority of that pressure came from one source; holidays. There were people taking holidays after long Covid waits, so that boosted demand. All in all the sector rose over 25% on a month over month basis. That’s a big move. So, the only good news is that the pressure should be a one-off. However, recreation and fruit and veg were the next big gainers for inflation on a m/m basis. Check out the m/m table here from ING

What this means for the RBA?

In a word, higher rates. Inflation is the number one target for central banks and that means expectations are now soaring for higher rates out of the RBA in their February meeting. Current expectations will now rise for a more aggressive RBA and a terminal rate that could rise higher than 3.5%. On balance this should keep the AUD supported again the NZD. However, the real event to look out for is a big divergence between the RBA and the RBNZ.

Can you be more specific about the content of your enticle? After reading it, I still have some doubts. Hope you can help me.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article. https://accounts.binance.com/register?ref=P9L9FQKY

Your point of view caught my eye and was very interesting. Thanks. I have a question for you. https://www.binance.info/zh-CN/register?ref=VDVEQ78S

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://accounts.binance.com/register?ref=P9L9FQKY

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

In der renommierten Salle Médecin schließlich scheinen die Basreliefs von Émile Peynot die Sonne Helios und den Mond Selene tanzen zu lassen.Das Casino de Monte-Carlo hat auch

seine kleinen Geheimnisse… Hier erkennt man die Gesichtszüge der Belle

Otero oder Liane de Pougy, der “mondänen” Frauen von Monte-Carlo, die der Maler Paul Gervais als Florentiner Grazien verewigt hat.

Ein selbstbewusster Prunk, der von Charles Garnier, dem Architekten der Pariser Oper, stammt.

Schon seine Fassade verspricht eine ganz besondere Welt.Am Eingang befindet sich ein wunderschönes Atrium, das mit Marmor gepflastert und mit 28 ionischen Säulen versehen ist.

Hier wurden schließlich das neue Casino und das Hotel de Paris an ihrem

endgültigen Standort errichtet, wobei der Bau 1858 begann.

Während dieser Anfangszeit wurden mehrere Versionen des Casinos gebaut und scheiterten aufgrund von Inkompetenz unter der Leitung von Charles III, und das Casino

wurde mehrmals verlegt, bis es schließlich in dem genannten Gebiet landeteLes Spelugues(Die Höhlen).

Das Casino wurde in einem Herrenhaus eröffnet, aber nicht gut genug geführt oder beworben und wurde so zu einem verlustbringenden Unterfangen. Die Einnahmen aus

dem geplanten Vorhaben sollten das rettenHaus von Grimaldiaus der Insolvenz.

Bekannt ist er durch die gleichnamige Spielbank und die alljährlich stattfindende Rallye

Monte Carlo. Lediglich der Zugang zu den privaten Spielräumen (Salon Privés) ist

mit Dresscode und Eintrittskarte möglich.

Im vorderen Bereich des Casino kann man auch ohne Anzug und Krawatte Las Vegas Casino-Flair geniessen und der Eintritts ist sogar frei.

Das Café de Paris Monte-Carlo direkt gegenüber ist ebenfalls einen Besuch wert, denn vorn dort aus

hat mein eine fantastische Aussicht auf den Eingangsbereich und die Vorfahrt des Casinos.

Das Casino von Monte-Carlo, ist das Werk des legendären Architekten Charles

Garnier, der ebenfalls die wunderschöne Pariser Oper gestaltet hat.

References:

https://online-spielhallen.de/ihr-zugang-zur-gaming-welt-lucky-dreams-casino-login/

Für die Bedienung sogt ein freundliches Team an Mitarbeitern in der Spieltstation. Die

Anfahrt aus der Innenstadt erfolgt am besten mit dem Auto,

da die Spielothek in einem Gewerbegebiet gelegen ist.

Die Spielstation in der Waffenschmidtstraße im Köner Norden ist ebenfalls eine empfehlenswerte Automatenspiel-Adresse.

Die Merkur-Automaten in der Casino Merkur Spielothek Colonia stammen von der Gauselmann-Gruppe mit Sitz in Espelkamp,

die zu Europas führenden Automatenherstellern und Spielhallenbetreibern gehört.

Eine freundliche Bedienung kümmert sich um die belange der Spieler und

serviert kostenlose Getränke und Snacks. Das Angebot des Casino Merkur Spielothek

Colonia und die Einrichtung wurde vor einigen Jahren vom Branchenverband der

deutschen Automatenwirtschaft mit dem Golden Jack ausgezeichnet.

Für das NS-Regime war der überwältigende Sieg bei der Volksabstimmung im Saargebiet am 13.

Durch seine Sonderstellung war das Saargebiet des Weiteren ein wichtiger Drehpunkt für das Einschleusen antirassistischer Propaganda ins Deutsche Reich.

Ab 1933 war das Saargebiet zum Zufluchtsort vieler im Deutschen Reich Verfolgter geworden, allen voran Juden, Kommunisten und Sozialdemokraten, aber auch von Oppositionellen beider

christlicher Konfessionen. Die Redaktion der „Volksstimme“ wurde geplündert und an vielen Orten erhängte man symbolisch Max-Braun-Puppen an Straßenlaternen und Masten.

References:

https://online-spielhallen.de/admiral-casino-cashback-ihr-weg-zu-mehr-spielguthaben/

Why does H3 use hexagons? And if you are having

problem with your data related tasks, don’t hesitate to connect I’m also fascinated by Photography, Gaming, Music, Astronomy and learning different languages.

The media shown in this article is not owned by Analytics Vidhya and is used at the Author’s discretion. To minimize their impact on most datasets, the system strategically

places these pentagons over oceans or less significant areas.

Uber’s H3, a powerful open-source spatial indexing system, provides

a unique hexagonal grid-based solution that enables seamless geospatial analysis

and fast query execution. It divides the Earth’s surface into hexagonal

cells of various sizes, creating a hierarchical structure that allows for spatial indexing and querying.

H3’s hexagonal grid partitions Earth into 122 base cells (resolution 0),

comprising 110 hexagons and 12 pentagons to approximate spherical geometry.

In today’s data-driven world, efficient geospatial indexing is crucial for applications ranging from ride-sharing and

logistics to environmental monitoring and disaster response.

As geospatial technology evolves, H3’s open-source ecosystem will likely see further enhancements,

including integration with machine learning models, real-time analytics, and 3D spatial indexing.

References:

https://blackcoin.co/online-gambling-for-newbies-main-types-of-online-casinos/

Some flights are operated by partner or subsidiary airlines.

Passengers travelling from Sydney, ensure you check-in online or via the Qantas App before you arrive

at the airport from 24 hours before departure. Customers on Qantas flights from Sydney are allocated checked baggage.

Is an international airport in Sydney, Australia located 8 km south of the Sydney central business district, in the suburb of Mascot.

Upload your document in one of these formats and we’ll handle the rest.

We support all major office document formats.

Google Translate performs the translation Your document’s text is extracted

taking special care in maintaining the exact format and styling

of each section. Preserves the layout of your original office document

Enjoy a meal or snack every time you fly with us, as well as

a range of refreshments including beer and wine.∆ Flight prices are per adult

in Australian Dollars, based on payment at qantas.com by

BPAY made 7 days or more before departure, or PayID. All of your travel details

in one place.

References:

https://blackcoin.co/top-welcome-bonuses-online-casinos/

You can play games, deposit, and withdraw among many other features on your tablet or smartphone.

RocketPlay is a crypto gaming casino so you will find several games dedicated

to digital currencies such as dice games, crypto slots and others.

This RocketPlay Casino review looks at the game selection, security and license, payment methods, mobile apps,

registration to the site, bonuses, and quality of customer service.

The casino is licensed by Curacao and mainly targets Canadian players but accepts players from Europe as well.

It’s players like you who make RocketPlay a fantastic gaming community.

Great app never have a issues with it best in the game go rocketplay

If you search rocketplay vip terms, you’ll see conversion rates for

XP to SP and the seasonal mechanics that keep top players engaged.

Search rocketplay payment or rocketplay-casino cashier for

the latest deposit options in your region before making a transfer.

This block summarises what to look for when comparing rocketplay, rocket play and rocketplay casino options.

Besides slots, you can enjoy hundreds of table games or live casinos and many more.

You can take your pick from various games and see which ones you enjoy the most.

For example, pokies usually contribute 100% of each wager, while

table games like blackjack and poker contribute

10% – 20%. In order to satisfy those 30x wagering requirements, though, you have to wager

the combined amount of your deposit and bonus 30 times

over. You’d get another $50 bonus on top, giving you a total of

$100 to play pokies with. If you’re having a

bad streak of luck, cashback offers return a percentage of your losses in the form of a bonus credit.

Best Australian online casino of December 2025 is Golden Crown casino.

We are here to assist you since gambling online in Australia can be a tricky experience.

Casinority Australia is a trusted casino guide with real experts that help Australian players make the right choice.

In a struggle to find a complete and comprehensive

Australian online casino guide, Casinority comes to the rescue.

Unlike free‑play or demo modes, these sites let you wager, win, and

withdraw cash. Use tools to control your gambling,

such as deposit limits or self-exclusion. The details you find at Casinority are

presented without warranty, so check the terms and local laws before playing a

casino. Live music and delicious food are a part of the casino entertainment that creates upbeat

energy that jollifies the entire experience. Now for a luxurious

take at one of the top casinos in Australia — Crown Melbourne.

References:

https://blackcoin.co/brand-new-casinos-online-in-australia-2025-a-comprehensive-guide/

online poker real money paypal

References:

https://werkstraat.com

online slot machines paypal

References:

inprokorea.com

paypal online casino

References:

https://futuremanager.nl/employer/paypal-casinos-best-online-casinos-that-accept-paypal-deposits/

paypal casinos for usa players

References:

https://rsh-beveiliging.nl/employer/our-favorite-paypal-casinos-2025-ranking-update/

online casino paypal

References:

https://skillproper.com/employer/best-online-casinos-australia-top-aussie-real-money-sites-2025/

australian online casinos that accept paypal

References:

https://sosjob.ca/employer/the-best-no-deposit-bonus-casino-in-australia-for-2025/

online casino usa paypal

References:

http://carecall.co.kr/bbs/board.php?bo_table=free&wr_id=2092656

paypal casinos online that accept

References:

https://swifthire.co.za/companies/2025/

online casino mit paypal

References:

https://workmall.uz/en/employer/top-10-best-australian-online-casino-sites-for-real-money-2025/

online real casino paypal

References:

https://empleos.getcompany.co/employer/best-online-poker-sites-in-2025-with-high-traffic-2025/

Die Spielmechanik ist allseits bekannt, weshalb vor allem Spieler von klassischen Games Online Automatenspiele wie dieses bevorzugen. Darüber hinaus bietet die beigefügte Risikoleiter stets die Chance, Gewinne an Online Slots durch Risiko zu steigern. Eye of Horus bietet gleich mehrere spannende Vorteile, wodurch es sich gegenüber anderen Spielen im Slots Casino abheben kann. Mit 6×5 Feldern ist Gates of Olympus vergleichsweise gut bestückt und bietet somit ausreichend Spaß für Spieler im HitNSpin Casino.

Ich habe letzte Woche 25 Freispiele für den neuen Slot Madame Destiny Megaways erhalten, indem ich den Code eingegeben habe, den sie auf Facebook gepostet haben. Das ist, wo sie exklusive Promo-Codes ziemlich häufig für Sachen wie Freispiele, keine Einzahlungsboni, Reload-Boni, Sie nennen es. Was das Cashback angeht, so ist es einfaches Bargeld mit nur 5x Durchspielen, was es viel einfacher macht, es abzuheben. Alle Gewinne aus Freispielen müssen vor der Auszahlung 30x umgesetzt werden. Was die Freispiele betrifft, so erhalten Sie insgesamt 200 Freispiele (20 pro Tag für 10 Tage) an berechtigten Slots wie Sweet Bonanza.

References:

https://s3.amazonaws.com/onlinegamblingcasino/trada%20casino%20login.html

Erreichbar ist der Kundensupport in einigen Echtgeld Casinos mittlerweile rund um die Uhr, an 365 Tagen im Jahr. Die Willkommensofferten sind im Bonus-Testbereich der Echtgeld Casinos aber nur die eine Seite der Medaille. In unseren Tests haben die Bonusform und die finanzielle Aufstellung natürlich eine Rolle gespielt. Die besten Echtgeld Casinos bearbeiten die Abhebungsanfragen ihrer Spieler innerhalb von wenigen Stunden. Einige, wenige Echtgeld Casino akzeptieren Deposits mit Diners Club.

Diese Hersteller bieten eine breite Palette an Spielen für jede “Online Spielothek” an, von klassischen Slots bis hin zu aufregenden Tischspielen. Ob Sie nun Fan von klassischen Tischspielen oder modernen Slots sind, StarGames.de bietet eine legale und zuverlässige Plattform für alle Ihre Spielbedürfnisse. Wenn du diese Punkte beachtest, kannst du in einem Casino mit Echtgeld sorgenfrei spielen. Internet-Casinos bieten Spielern normalerweise die Möglichkeit, in US-Dollar, Kanadischen Dollar, Euro, Britischen Pfund und anderen gesetzlichen Zahlungsmitteln zu spielen. 95% Auszahlungsrate bedeutet, dass Sie für jeden Euro, den Sie spielen, 95 Cent zurückgewinnen werden. Wir sind kein Glücksspielanbieter und bieten auch keine Echtgeld-Dienste an.

References:

https://s3.amazonaws.com/new-casino/casino%20of%20gold.html

In jedem Online Casino mit deutscher Lizenz kannst du bedenkenlos spielen und es an den Automaten richtig krachen lassen. Nur in einem Online Casino mit deutscher Lizenz darfst du als deutscher Spieler derzeit legal und vollkommen gesetzeskonform spielen. Alleseriösen Online Casinosmit deutscher Lizenz dürfen ausschließlich virtuelle Automatenspiele anbieten.

Doch Spieler können sich schnell einen Überblick verschaffen, ob ein Anbieter seriös ist oder nicht und ob sie gewillt sind mit echtem Geld zu spielen. Alle Titel wie 40 Thieves, Creatures of the Night, Mystic Force and Fruits & Wilds 2 könnt ihr auch sowohl in der Spielothek als auch im Online Casino um echtes Geld spielen. Jedoch ist der Hersteller derzeit nicht mehr auf dem deutschen Markt vertreten. Eine Reihe von traditionellen deutschen Herstellern hat sich einen besonderen Platz im Gedächtnis der Spielautomaten Fans gesichert. Spielotheken Spieler aufgepasst – mittlerweile haben zahlreiche Klassiker aus den deutschen Spielsalons auch in den Echtgeld Casinos Einzug gehalten. Einsteiger und Gelegenheitsspieler treten tendenziell häufiger um niedrigere Beträge an.

References:

https://onlinegamblingcasino.s3.amazonaws.com/casino%20landau.html

References:

Rivers casino

References:

https://hedge.fachschaft.informatik.uni-kl.de/s/rBX3vmE5a

References:

Before and after anavar male

References:

https://dlx.hamdard.pk/user/profile/321361

Your point of view caught my eye and was very interesting. Thanks. I have a question for you. https://accounts.binance.com/register-person?ref=IHJUI7TF

References:

Roulette wheel iq cube

References:

http://lideritv.ge/user/spainkarate0/

References:

Top 10 online casinos

References:

https://trade-britanica.trade/wiki/WD40_Casino_2026_1500_Welcome_Bonus_7000_Games_Fast_Withdrawals

which describes a consequence of steriod abuse?

References:

http://fprints.com.ua/user/mapfear7/

where can i get steroids to build muscle

References:

https://www.faax.org/author/slopeatom67/

References:

Before and after test cyp 500 week and anavar pics

References:

https://egamersbox.com/cool/index.php?page=user&action=pub_profile&id=249363

References:

Take anavar before or after workout

References:

https://linkvault.win/story.php?title=anvarol-before-and-after-pictures-male-and-female-results

legal steroids

References:

https://squareblogs.net/startbacon7/dianabol-10-mg

References:

Anavar before and after reddit female

References:

https://king-bookmark.stream/story.php?title=anavar-only-cycle-results-what-to-expect

References:

Anavar before and after 8 weeks

References:

https://squareblogs.net/liquorsnail5/legal-anavar-for-women-before-and-after-results-with-pictures

References:

Anavar use before and after

References:

http://muhaylovakoliba.1gb.ua/user/mailselect9/

%random_anchor_text%

References:

https://trade-britanica.trade/wiki/Compounded_Stanozolol_Capsules

References:

Anavar and clenbuterol before and after

References:

https://wifidb.science/wiki/CrazyBulk_Anvarol_Review_Ergebnisse_mit_Vorher_und_NachherBilder_TheVitLab

how to get illegal steroids

References:

https://instapages.stream/story.php?title=where-to-buy-clen-your-ultimate-guide-to-finding-the-best-sources

trusted steroid sites

References:

https://notes.io/euhrm

References:

Us online casinos

References:

https://gpsites.win/story.php?title=candy96-casino-minimum-deposit-by-payment-online-engagement-for-australia

References:

Manoir richelieu charlevoix

References:

https://bookmarks4.men/story.php?title=enjoy96-casino-australia-2025-play-now

References:

Comanche red river casino

References:

https://support.mikrodev.com/index.php?qa=user&qa_1=atmfront8

References:

Us online poker sites

References:

https://www.demilked.com/author/deathtanker0/

References:

Silverton casino las vegas

References:

https://pad.stuve.uni-ulm.de/s/DLEtLZaiG

References:

Slots no deposit bonus

References:

https://dreevoo.com/profile.php?pid=995721

References:

Flamingo casino

References:

https://empirekino.ru/user/timerboat5/

References:

Blackjack trainer

References:

https://bookmarkzones.trade/story.php?title=modes-de-paiement-et-expedition

References:

500 club casino

References:

https://justbookmark.win/story.php?title=pardon-our-interruption

References:

Louisiana casinos

References:

https://coolpot.stream/story.php?title=jeux-de-plateau-jouer-en-ligne-sur-snokido

anabolic steroids athletes

References:

https://humanlove.stream/wiki/HUMATROPEN_24_stylo_injection_hormone_de_croissance_Parapharmacie

%random_anchor_text%

References:

https://www.pathofthesage.com/members/coughsound7/activity/744065/

%random_anchor_text%

References:

https://ekademya.com/members/cementden82/activity/184446/

muscle build products

References:

https://opensourcebridge.science/wiki/Thermogniques_Brleur_de_Graisse

performance enhancing drugs in the military

References:

https://pad.stuve.de/s/_EG-DzQ-b

bodybuilder steroids

References:

https://u.to/gjlyIg

best supplement stack for shredding

References:

https://cameradb.review/wiki/Notre_top_10_des_Glucavit_Glules_Minceur_au_France_Janvier_2026

difference between corticosteroids and anabolic steroids

References:

https://bookmarkfeeds.stream/story.php?title=dove-si-compra-il-testosterone

steroids growth hormone

References:

https://digitaltibetan.win/wiki/Post:10_alimentos_para_aumentar_la_testosterona_con_men_y_recetas

References:

Parks casino

References:

https://funsilo.date/wiki/96_com_1_Trusted_Online_Casino_Sports_and_Crypto_Betting_Site

References:

Royal vegas casino

References:

https://atavi.com/share/xo506wzj3kpk

References:

Igt slot machines

References:

https://cuwip.ucsd.edu/members/saletights2/activity/2761876/

References:

Hollywood casino toledo oh

References:

https://nhadat24.org/author/woolground0

buy legit testosterone cypionate

References:

https://gratisafhalen.be/author/refundcheque5/

six star creatine x3 pill

References:

https://funsilo.date/wiki/Wie_Testosteron_steigern_Urologe_erklrt_was_Mnnern_wirklich_hilft

does the rock take steroids

References:

https://jespersen-bager-3.technetbloggers.de/buy-genotropin-miniquick-0-2mg-price-in-uk-and-london

best non-steroid supplements

References:

http://dranus.ru/forums/user/dimplecopper83/

References:

Treasure island casino mn

References:

https://elearnportal.science/wiki/1RED_Casino_Deutschland_Ihr_strategischer_Partner_fr_OnlineGaming

References:

Casino mobile

References:

https://humanlove.stream/wiki/Limit_Geld_abheben_Kartenzahlung_je_nach_Bank

References:

Ameristar casino vicksburg

References:

https://blogfreely.net/lizarddrum7/1red-login-in-deutschland-schnell-und-sicher

References:

Casino night the office

References:

http://lideritv.ge/user/pologauge4/

References:

Slots deco

References:

https://securityholes.science/wiki/Login_Registrierung_3_000_Bonus

References:

Slots for fun

References:

http://dubizzle.ca/index.php?page=user&action=pub_profile&id=127063

References:

Hollywood casino bay st louis ms

References:

http://jobboard.piasd.org/author/feastliquid88/

References:

Roletai

References:

https://gaiaathome.eu/gaiaathome/show_user.php?userid=1834872

References:

Kickapoo lucky eagle casino

References:

https://stilling-baldwin-2.technetbloggers.de/payid-casino-best-australian-online-casinos

what’s the biggest you can get without steroids

References:

https://aguirre-ennis-4.mdwrite.net/testosteronersatztherapie-alles-was-du-wissen-musst

prescription steroids names

References:

https://clashofcryptos.trade/wiki/Effective_Anavar_and_Winstrol_Cycle_Ultimate_Guide_for_Fitness_Goals

buy steroids online uk

References:

https://forum.dsapinstitute.org/forums/users/silicameat80/

Ignition casino Australia is among the most popular online gambling establishments in the country. Ignition explores the top 7 Aussie poker players and their paths to success. Australia is home to some of the most iconic players in poker. Ignition Poker cash games could be the answer you’ve been looking for. Do you want an online poker-playing experience that’s equal parts flexible and fruitful? As the name suggests, this bonus rewards you with up to $125 in cash whenever you refer a mate to Ignition Casino and they make their first candy96.fun deposit.

First of all, we have a wide range of games that cater for different tastes; this is because our library contains various titles which come with high quality graphics coupled with engaging gameplay hence ensuring even the most demanding player finds something interesting to play here on ignition casino Australia platform. Learn more about using crypto to play online pokies for real money here. Offering a seamless gaming experience, Ignition allows you to play online pokies for real money from the comfort of your home or on the go.

Over 30+ world-class providers including NetEnt, Pragmatic Play, and Microgaming “Love playing Zone Poker here – action is non-stop! Customer support always helps when needed. No ID verification hassles.” $2,500 weekly poker freeroll Explore leaderboards, tournaments, and ever-changing bonus offers designed to enhance every spin. Designed for thrill-seeking gaming enthusiasts, this platform blends innovative slot experiences with top-tier rewards and round-the-clock excitement. The casino allows one free withdrawal per month, with subsequent withdrawals incurring small processing fees.

References:

https://blackcoin.co/best-online-casinos-australia-2025-a-comprehensive-guide/

dana linn bailey steroids

References:

https://onlinevetjobs.com/author/kevinbakery2/

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me? https://www.binance.com/register?ref=IXBIAFVY

steroids for muscle gain

References:

https://p.mobile9.com/linensilk3/

legitimate steroid sites

References:

http://dubizzle.ca/index.php?page=user&action=pub_profile&id=138494

best injectable steroids

References:

https://funsilo.date/wiki/Dianabol_Erfahrungen_Kaufen_Dianabol_Wirkstoff_Kur_2026

top rated muscle building stacks

References:

https://sciencewiki.science/wiki/Clenbuterol_Cycle_for_Fat_Loss_Dosage_Results

best lean muscle building stack

References:

https://instapages.stream/story.php?title=winstrol-online-kaufen-zu-niedrigem-255-preis-in-deutschland-3

anabolics.com review

References:

https://www.udrpsearch.com/user/seederbike1

top selling legal steroids

References:

https://gaiaathome.eu/gaiaathome/show_user.php?userid=1840108

how to stack steroids

References:

https://a-taxi.com.ua/user/planetstreet23/

garcinia gnc store

References:

https://mozillabd.science/wiki/Garcinia_Cambogia_Dried_Whole_100g_100_Natural

what do steroids treat

References:

https://www.youtube.com/redirect?q=https://cuisine.at/ajax/pages/index.php?comprar_hgh_3.html

long term effects of anabolic steroids

References:

https://bbs.pku.edu.cn/v2/jump-to.php?url=https://cerraelx.es/wp-content/pgs/?pastillas_para_adelgazar_1.html

best steroid for bulking

References:

https://www.instapaper.com/p/17441498

steroid use in women

References:

https://king-wifi.win/wiki/29_Best_Diet_Pills_for_Weight_Loss_in_2026_That_Actually_Work

another name for physiological risk is safety risk.

References:

https://telegra.ph/Medikamente-online-kaufen-ohne-Rezept–5-Anbieter-im-Test-02-06

buying steroids from mexico

References:

http://premiumdesignsinc.com/forums/user/movesharon6/

best place to order steroids

References:

http://okprint.kz/user/attackcable7/

anabolic testosterone for sale

References:

https://donaldson-flanagan.federatedjournals.com/anaca3-est-il-efficace-pour-maigrir-avis-temoignages

gala casino birmingham

References:

https://case.edu/cgi-bin/newsline.pl?URL=https://free100pokiesnodeposit.blackcoin.co

best online casino games

References:

http://premiumdesignsinc.com/forums/user/seadonald72/

sugar creek casino

References:

https://g.clicgo.ru/user/colonylinen1/

casino world challenge

References:

https://bookmarking.stream/story.php?title=crypto-friendly-gaming-experience-with-no-rules-bonuses

harrah’s casino tunica

References:

https://tvoyaskala.com/user/beaverlake4/

genting casino glasgow

References:

https://clenta.com/the-big-bang-theory/

the colosseum at caesars windsor

References:

https://atesoglusogutma.com/user/lightriver9/

river spirit casino tulsa ok

References:

https://valencia-gay-2.blogbright.net/online-casino-king

walking stick casino

References:

https://sibze.ru/index.php?subaction=userinfo&user=chanceshare13

blackjack switch

References:

https://bookmarks4.men/story.php?title=best-e-wallet-casinos-australia-2026-top-10-ranked

san francisco casinos

References:

https://500px.com/p/mackaythxrosa

top 10 online casinos

References:

https://bookmarkspot.win/story.php?title=casino-bonuses-australia-2026-find-top-casino-bonus-offers

how much does a steroid cycle cost

References:

https://scientific-programs.science/wiki/Anavar_kaufen_Sichere_Oxandrolon_Tabletten_online_bestellen

spawn test booster

References:

https://marvelvsdc.faith/wiki/Medikamente_bestellen_Achtung_vor_Flschungen

%random_anchor_text%

References:

http://jobs.emiogp.com/author/detailbush1/

anabolic steroids pill form

References:

http://downarchive.org/user/walrusflare4/

anabolic steroids gnc

References:

https://chessdatabase.science/wiki/Anavar_Erfahrungen_Zyklus_Nebenwirkungen_Vorteile

steroids to burn fat

References:

https://trade-britanica.trade/wiki/Oxandrolon_Strafe_bei_Bestellung_Besitz_AntiDopG

santa ana star casino

References:

https://royaltech.ng/2024/04/25/diy-electrical-projects-what-you-should-and-shouldnt-do/

anabolic steroids mechanism of action

References:

https://www.garagesale.es/author/liftsalad4/

classic casino

References:

http://schlatthof.net/togo-reise-maerz-2020/palmoel-und-seife/

online casino reviews

References:

http://schlatthof.net/togo-reise-november-2023/es-geht-gleich-in-die-vollen-uns-erster-tag-in-togo/

mardi gras casino florida

References:

http://www.upendogroup.ngdafrica.com/spip.php?article56

casino 888

References:

https://vivek-desai.com/pages/page-left-sidebar/

slot machine

References:

https://marketmed.kz/news/spaysovaya-zavisimost-myetody-lyechyeniya/

werken bij holland casino

References:

https://magiamgia.blog.fc2.com/blog-entry-48494.html

super scratch programming adventure

References:

https://watbosa.ac.th/question/csfgnhiuu/

eurogrand casino

References:

https://community.decentrixweb.com/index.php/question/lewiscrila-8/

casino aztar

References:

https://animallovergifts.com/catloversgift/

jumers casino rock island

References:

https://barnsfortroende.com/barns-rattigheter-i-sverige/

talking stick casino az

References:

https://animallovergifts.com/dogtoys/

cash casino calgary

References:

https://cpdbouvxc3m7.blog.fc2.com/blog-entry-376.html

side effects of stackers

References:

http://amur.1gb.ua/user/pearpeony5/

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

pre hormones bodybuilding

References:

https://output.jsbin.com/rehadawasi/

is predisone and testosteone bad to take together

References:

https://ellington-castaneda.federatedjournals.com/top-weight-loss-medications

where do i get steroids

References:

https://telegra.ph/Proposed-United-States-acquisition-of-Greenland-Wikipedia-03-02

steroids facts

References:

https://md.un-hack-bar.de/s/Z3AwBLoZPp

are steroids legal in uk

References:

https://www.udrpsearch.com/user/moononion4

check prescription prices

drugs without prescription

canadian pharmacy meds

list of trusted canadian pharmacies

pharmacy prescription

References:

Play online cricket games

References:

https://uttarakhandkinews.com/ganesh-joshi-342/

legitimate canadian pharmacy online

express pharmacy

References:

Geant casino la foux

References:

https://zenwriting.net/cousininch1/self-exclusion-tools-in-australia-practical-guide-for-aussie-punters-smiths

canadian online pharmacies prescription drugs

References:

Boylecasino

References:

https://yatirimciyiz.net/user/blockguilty9

References:

Hamburg casino

References:

https://matkafasi.com/user/peanutsushi8

Slottica Casino to propozycja dla graczy szukających nowoczesnej platformy do gry online i wygodnego dostępu do szerokiej oferty rozrywki. Serwis wyróżnia się intuicyjnym interfejsem, sprawną obsługą płatności oraz atrakcyjnym wyborem gier dopasowanych do różnych preferencji. Na szczególną uwagę zasługują wysokie standardy bezpieczeństwa, w tym szyfrowanie danych i rozwiązania chroniące prywatność użytkowników na każdym etapie korzystania z platformy. Dzięki temu gracze mogą skupić się na zabawie, mając pewność, że ich dane osobowe i finansowe są odpowiednio zabezpieczone. To jeden z ciekawszych wyborów dla osób zastanawiających się, gdzie grać online w bezpieczny i komfortowy sposób.

References:

Top 5 muscle building supplement

References:

http://124.223.89.168:8080/emiliagunderso

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me? https://www.binance.com/register?ref=IXBIAFVY

References:

Steroids before and after women

References:

https://servus-nachbar.at/Neuigkeiten/index.php/;focus=W4YPRD_com_cm4all_wdn_Flatpress_7491266&path=&frame=W4YPRD_com_cm4all_wdn_Flatpress_7491266?x=entry:entry250510-130344%3Bcomments:1

Vavada to znane kasyno online, które działa również w Polsce. Strona przyciąga graczy szeroką ofertą gier, przejrzystymi warunkami i obsługą w PLN (zł). Bonus powitalny oraz intuicyjna obsługa sprawiają, że platforma zdobyła popularność wśród polskich użytkowników.

References:

All star slots

References:

https://monjournal.top/item/475186

Vavada to znane kasyno online, które działa również w Polsce. Strona przyciąga graczy szeroką ofertą gier, przejrzystymi warunkami i obsługą w PLN (zł). Bonus powitalny oraz intuicyjna obsługa sprawiają, że platforma zdobyła popularność wśród polskich użytkowników.

References:

What is gear bodybuilding

References:

https://onlinevetjobs.com/author/quinceevent0/

References:

Best test stack

References:

https://parnian.app/margob49225207

References:

Anabolic steroids can be ingested in which of the following ways

References:

https://hack.allmende.io/s/MQauc81xQ

References:

Will steroids burn fat

References:

https://md.chaosdorf.de/s/GxoUXqzGYh

References:

Sustanon cycle for beginners

References:

https://jasminsideenreich.de/Blog/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_7099662&path=&frame=STRATP_com_cm4all_wdn_Flatpress_7099662?x=entry:entry221031-095821%3Bcomments:1

References:

Best legal cutting supplement

References:

https://www.jasminsideenreich.de/Blog/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_7099662&path=&frame=STRATP_com_cm4all_wdn_Flatpress_7099662?x=entry:entry210510-095751%3Bcomments:1

References:

Best steroids for muscle gain and fat loss

References:

https://www.grenzlandgruen.de/Blog;amp;frame=&focus=TKOMSI_com_cm4all_wdn_Flatpress_22892279&path=&frame=TKOMSI_com_cm4all_wdn_Flatpress_22892279?x=entry:entry241123-080042%3Bcomments:1

References:

Skyvegas

References:

https://ondashboard.win/story.php?title=get-a-bonus-slots-and-games-with-dealers

References:

Bor Testosteron

References:

https://pads.zapf.in/s/EAOHBrqMgl

advair diskus online pharmacy indian pharmacy online shopping vibramycin online pharmacy

References:

Female steroid cycles

References:

https://essencialponto.com.br/employer/what-is-tren-cough-and-how-to-avoid-it/

amoxil online pharmacy phentermine online pharmacy reviews estrace online pharmacy

legal online pharmacy xanax online pharmacy vicodin no prescription study pharmacy online free

References:

Dianabol cycle for sale

References:

http://223.71.122.54:3000/aguedacollette

With thanks, Useful information.

References:

https://roy-kearns-2.thoughtlanes.net/online-casino-mit-den-schnellsten-auszahlungen-in-deutschland

References:

Instant Casino Login vergessen

References:

https://school-of-safety-russia.ru/user/fingermoat3/

References:

Instant Casino Freispiele

References:

http://amur.1gb.ua/user/hosebell9/

References:

Instant Casino Willkommensbonus

References:

https://zenwriting.net/pocketlamb8/hol-dir-deinen-100-bonus-und-freispiele

References:

Instant Casino mobile spielen

References:

http://karayaz.ru/user/ageclick0/

References:

Salons professionnels

References:

https://harpkettle6.bravejournal.net/willkommensbonus-200

References:

Gewinne bei Instant Casino auszahlen

References:

https://albrechtsen-thorup-4.hubstack.net/online-casino-mit-den-schnellsten-auszahlungen-in-deutschland

References:

Gala casino birmingham

References:

https://mes-favoris.site/item/596720

References:

Instant Casino Auszahlung sofort

References:

https://www.pradaan.org/members/raywriter6/activity/838459/

References:

Beste echtgeld casinos

References:

https://sciencewiki.science/wiki/Beste_Echtgeld_Casinos_2026_Tagesordnungspunkt_Verbunden_Versorger_inside_Teutonia_Bravo_Property_Ltd_Worldnews_com

References:

Instant Casino Einzahlungsmethoden

References:

https://md.chaosdorf.de/s/9MtTb6TgIi

References:

Royal vegas casino

References:

https://www.udrpsearch.com/user/brassoval98

References:

Instant Casino Login vergessen

References:

https://rentry.co/g5t5wktb

References:

Echtgeld casino sofortauszahlung

References:

https://lit-book.ru/user/dryvessel24/

References:

Instant Casino App iOS

References:

https://tvoyaskala.com/user/priesttire2/

viagra usa online pharmacy vipps certified online pharmacy viagra tretinoin online pharmacy

References:

Instant Casino VIP Programm

References:

https://thefreeadforum.top/index.php?page=user&action=pub_profile&id=940398

accutane 40 mg online pharmacy reliable online pharmacy accutane us online viagra pharmacy

References:

Instant Casino Konto erstellen

References:

https://alushta-shirak.ru/user/peonyball6/

Kasyno vavada systematycznie buduje swoją pozycję wśród polskim graczom, oferując kompletną lokalizację w języku polskim. Vavada casino zapewnia metody płatności dostosowane do lokalnego rynku, a vavada pl umożliwia łatwy dostęp dla graczy z Polski. Oficjalną stronę vavada kasyno odwiedzają głównie doświadczonych graczy, którzy doceniają atrakcyjne bonusy i program lojalnościowy.

References:

Beste echtgeld casinos

References:

https://lit-book.ru/user/dryvessel24/

References:

Steroid pills for bodybuilding

References:

https://dev-members.writeappreviews.com/employer/hi-tech-pharmaceuticals-anavar-on-sale-at-allstarhealth-com/

References:

Best test stack

References:

https://mmcon.sakura.ne.jp:443/mmwiki/index.php?fiberfuel3

References:

Sport Testosteron erhöhen

References:

https://scientific-programs.science/wiki/Verify_Before_You_Buy_The_Center_for_Safe_Internet_Pharmacies_CSIP

References:

Testosteron Booster Tabletten

References:

https://barefoot-gates.hubstack.net/win-max-legal-winstrol-alternative

References:

Testosteron Tabletten Vergleich

References:

https://scientific-programs.science/wiki/How_Legal_Is_HGH_Therapy_Can_You_Get_It_Online

goodrx tadalafil bluechew tadalafil review tadalafil 20mg review

sildenafil 20mg sildenafil headache sildenafil cost

References:

Anabolic steroids injections

References:

https://sibze.ru/index.php?subaction=userinfo&user=outputcarrot45

viagra effects when to take viagra pfizer viagra

References:

Gnc pro performance whey protein

References:

https://rentry.co/iv94rmp4

References:

Legal steroids com reviews

References:

https://hack.allmende.io/s/TGFWc7Cvb

References:

Anabolic steroid prescriptions

References:

https://www.giveawayoftheday.com/forums/profile/1600729

References:

Legal steroids information

References:

http://muhaylovakoliba.1gb.ua/user/seedercactus9/

cialis walmart daily cialis cialis daily dose

Your article helped me a lot, is there any more related content? Thanks!

References:

Steroid purchase online

References:

https://www.adpost4u.com/user/profile/4261463

no prescription pharmacy paypal legitimate online pharmacy cialis online pharmacy quick delivery

References:

What types of steroids are there

References:

https://www.24propertyinspain.com/user/profile/1370013

vardenafil hcl 20mg tab cost liquid vardenafil generic vardenafil

References:

How long have steroids been around

References:

https://willard-knight-2.mdwrite.net/der-ultimative-leitfaden-fur-den-sicheren-und-legalen-kauf-von-anavar-24-7-is

References:

Legal deca durabolin

References:

https://abrams-powell-2.mdwrite.net/acheter-prohormone-de-croissance-hgh

References:

Strongest fat burning steroid

References:

https://sciencewiki.science/wiki/Anavar_Oxandrolone_tablets_for_sale_online_in_UK_US

References:

Which body type is more common in men and associated with the most negative health risk?

References:

http://09vodostok.ru/user/roofbeggar31/

References:

Anabolic website

References:

https://travelersqa.com/user/bambooanimal78

viagra for sale does viagra make your dick bigger how to use viagra

cialis half life what does cialis do cialis generic cost

tadalafil max dose tadalafil 20 mg tablet uses tadalafil para que sirve

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://www.binance.com/register?ref=JW3W4Y3A

legitimate canadian pharmacy online metronidazole cream online pharmacy canadian pharmacy world coupon code

References:

4 week muscle building workout

References:

https://interior01.netpro.co.kr:443/bbs/board.php?bo_table=free&wr_id=159

References:

Anabolic steroids are a type of quizlet

References:

https://hikvisiondb.webcam/wiki/Clenbuterol_Cost_Trends_and_Why_Fat_Burner_Legal_Steroids_Are_Gaining_Popularity

daily tadalafil tadalafil effects on kidneys tadalafil blood pressure

zoloft online pharmacy no prescription naturxheal family pharmacy & health store-doral azithromycin online pharmacy no prescription

References:

Online Casino Echtgeld Poker

References:

http://madk-auto.ru/user/sundayray1/

References:

Echtgeld Automaten Online

References:

https://holm-hunter-5.technetbloggers.de/online-casinos-deutschland-2026-liste-von-95-anbietern

References:

Free male enhancement pills with free shipping

References:

https://md.swk-web.com/s/WCxa9L3O3

References:

Rocketplay casino neosurf alternative

References:

https://botdb.win/wiki/Fast_Secure_Rocketplay_Casino_Neosurf_Payments

References:

Clenbuterol kaufen Ohne Rezept

References:

http://ezproxy.cityu.edu.hk/login?url=https://hausarzt-in-steglitz.de/wp-content/pgs/clenbuterol_kaufen_3.html

References:

Hgh kaufen ohne rezept

References:

https://output.jsbin.com/tadebivocu/

References:

Kaufen Clenbuterol problemlos

References:

https://rentry.co/z7fymxws

Zanurz się w fascynujący świat kasyna online Slottica, popularnej platformy hazardowej, która zdobyła uznanie graczy w ponad 15 krajach Europy, w tym w Polsce, Niemczech i Czechach. Nasza oferta obejmuje przeszło 8500 gier kasynowych od czołowych dostawców, takich jak Games Global, Play’n GO, Pragmatic Play czy EGT. Znajdziesz tu zarówno klasyczne automaty w stylu Book of Dead czy Sizzling Hot Deluxe, jak i nowoczesne sloty z progresywnymi jackpotami, np. Mega Moolah, a także gry stołowe i emocjonujące rozgrywki na żywo z krupierami od Evolution Gaming. Możesz także pobrać naszą oficjalną aplikację, zalogować się na swoje konto lub założyć nowe.

References:

Real casino slots

References:

https://notes.io/evZTa

References:

Steroids classification

References:

https://ziegler-bjerring-4.blogbright.net/testosterone-en-ligne-achat-securise

generic tadalafil tadalafil 20 mg tablet uses tadalafil 40mg

online pharmacy valtrex no prescription cialis online pharmacy no prescription what pharmacy sells azithromycin

References:

Safe online casino

References:

https://sme.fund-lab.org/2023/06/22/the-power-of-effective-communication-in-business/

References:

Redwind casino

References:

https://kenbc.nihonjin.jp/album/album.cgi?mode=detail&no=449&page=0

References:

Online poker australia

References:

https://anasmitrap.org.br/em-primeira-reuniao-da-mesa-de-negociacao-permanente-do-mte-entidades-sindicais-de-servidores-administrativos-apresentam-documento-com-diagnostico-propostas-e-criam-plano-de-acao/

References:

Iron horse casino

References:

https://creditoup.com.br/como-comparar-bancos-e-escolher-o-melhor-financiamento/

References:

Slot madness casino

References:

https://bfreetv.com/@dorothyleech65?page=about

References:

Terribles casino

References:

https://cloveebiz.com.ng/@valentinapelle?page=about

good rx tadalafil cialis professional (sublingual) (tadalafil) tadalafil blood pressure

online pharmacy prescription cheapest pharmacy to fill prescriptions without insurance legal online pharmacy coupon code

References:

Roulette strategy to win

References:

https://graph.org/Woo-Casino-Review-Top-Bonuses–Games-04-20

References:

Blackjack hands

References:

https://graph.org/Top-Rated-Best-Online-Casinos-Expert-Reviews–Real-Money-Bonuses-04-20

tadalafil how long does tadalafil take to work how to take tadalafil

pharmacies in canada that ship to the us online pharmacy without insurance online pharmacy viagra no prescription

tadalafil side effects blood pressure does tadalafil expire daily tadalafil

non prescription online pharmacy reviews can you buy viagra at a pharmacy canadian pharmacies that deliver to the us

vipps certified online pharmacy list online pharmacy propecia no prescription amoxicillin online pharmacy no prescription

rx pharmacy no prescription giant food store pharmacy hours generic viagra online pharmacy india

Vavada w Polsce zdobyła popularność dzięki pełnej lokalizacji i wsparciu dla płatności w złotówkach. Gracze doceniają możliwość grania w języku polskim i kontakt z obsługą klienta w rodzimym języku. Oferta promocyjna, w tym stały cashback 10, dodatkowo zwiększa atrakcyjność kasyna. Na tle konkurencji wyróżnia się szeroką gamą gier, szybkim czasem wypłat i aplikacjami mobilnymi. Wszystko to czyni serwis istotnym graczem na polskim rynku gier online. Vavada Polska kusi graczy nie tylko bonusami, ale też prostotą rejestracji i ogromnym katalogiem gier. Wygodne płatności w PLN oraz szybkie wypłaty? To właśnie doceniają użytkownicy. Wielu z nich chwali intuicyjną obsługę i dynamiczne aplikacje mobilne. A cashback? W Polsce uznawany jest niemal za obowiązkowy element, bo pozwala zmniejszyć ryzyko strat. Czy dziwi więc, że platforma zdobyła reputację bezpiecznej i praktycznej alternatywy wobec konkurencji?

reliable online pharmacy accutane safe reliable canadian pharmacy pharmacy no prescription required

cheapest pharmacy to fill prescriptions with insurance no prescription viagra online pharmacy canadian online pharmacy cialis

community rx pharmacy warren mi best canadian online pharmacy viagra canadian pharmacy vipps approved

best online pharmacy no prescription river pharmacy low dose naltrexone safe reliable canadian pharmacy

References:

Paddy power live casino

References:

https://grand-mondial-casino.online-spielhallen.de/

References:

Hooters casino las vegas

References:

https://chicken-casino.online-spielhallen.de/

References:

Paderborn

References:

https://casino-royal-drehorte.online-spielhallen.de/

us pharmacy no prior prescription canadian pharmacy without prescription online pharmacy no prescription augmentin

giant food store pharmacy hours sildenafil citrate online pharmacy health express pharmacy+artane castle

best canadian online pharmacy reviews buying prescription drugs from canada rite aid pharmacy how many store

online pharmacy no prescription provigil online pharmacy fedex overnight shipping non prescription cialis online pharmacy

References:

No deposit codes

References:

https://graph.org/What-Beer-Do-People-Drink-In-Darwin-04-27

References:

The meadows casino

References:

https://graph.org/Best-Casino-Online-In-Australia-04-27

best canadian pharmacy to buy from how much does cialis cost at a pharmacy new at your publix pharmacy free lisinopril

online pharmacy without scripts viagra generic pharmacy online naturxheal family pharmacy & health store-doral

how much does percocet cost at pharmacy cheap viagra online pharmacy prescription legit canadian pharmacy online

what’s the best online pharmacy canadian pharmacy no prescription naturxheal family pharmacy & health store-doral

how much does viagra cost in a pharmacy buy naltrexone from trusted pharmacy canadian pharmacy no prescription needed

foreign pharmacy no prescription can you buy clomid from a pharmacy periactin online pharmacy no prescription

mexico pharmacy order online metoprolol succinate online pharmacy canadian pharmacy online cialis

online pharmacy birth control pills certified online pharmacy cialis safeway pharmacy online prescription refill

References:

Hvilke spillemaskiner giver den højeste udbetaling

References:

https://gitea.visoftware.com.co/albweldon80431

References:

Hvordan

References:

https://carwiki.site/wiki/Bedste_Casino_Bonusser_Uden_Omstningskrav_2026

m fortune https://m-fortune.info/

References:

Udbetalingsvenlige casinoer Danmark

References:

https://quickfixinterim.fr/employer/casino-bad-homburg-unfall-heute/

secure medical online pharmacy canadian compounding pharmacy online shopping pharmacy india

canadian pharmacy discount coupon aarp medicare rx pharmacy directory international pharmacies that ship to the usa

NeoSpin https://adventureallstars.tv/

reputable canadian online pharmacies online pharmacy not requiring prescription online pharmacy price checker

Queen Win https://queenwincasinos.com/

casino https://optimaiweb.com/en/domain/hacksawgaming.uk.com

casino https://siteliner.com/hacksawgaming.uk.com?siteliner=site-dashboard

canadian pharmacy meds review generic viagra online canadiain pharmacy online pharmacy pain relief

casino https://www.optidiscover.com/tools/website-reviewer/domain/pragmaticplay-demo.uk

casino https://alfaqeerbroadcast.com/read-blog/50891_shade-club-redefines-high-quality-customer-retention-programs.html

casino https://3rrend.com/read-blog/78078_shade-club-redefines-provably-fair-gaming-standards.html

Ninewin https://casino-ninewin.net/

casino https://blacktube.in/read-blog/40608_rainbet-039-s-revolutionizes-roulette-playing.html

casino https://konnetin.com/read-blog/159_the-amon-revolutionises-speed-in-rapid-payments.html

casino https://drviet.com/read-blog/20959_unibet-casino-uk-and-the-of-21-proficiency.html

casino https://graph.org/Jokabet-casino-Changes-World-Tournament-Betting-04-16-17

casino https://graph.org/Joka-Bet-casino-Assists-Beginners-Through-Wagering-Essentials-04-16-2

casino https://telegra.ph/Jokabet-casino-Changes-World-Tournament-Betting-04-16-89

casino https://graph.org/Bety-casino-Transforms-Bonus-Buy-Mechanics-04-16-4

casino https://graph.org/Betty-casino-Transforms-Bonus-Buy-Features-04-16-10

casino https://telegra.ph/Bwin-competencias-Transforman-la-Experiencia-de-las-Apuestas-Olímpicas-04-16

References:

Casino online bonus

References:

https://salestracker.realitytraining.com/node/20924

casino https://graph.org/Guía-para-Empezar-en-el-Mundo-de-las-Apuestas-Deportivas-04-16-3

casino https://graph.org/Deportes-bwin-y-la-fenómeno-de-las-apuestas-en-e-sports-04-16-2

References:

Virtual roulette

References:

https://kigalilife.co.rw/author/fredabnk679/

casino https://graph.org/Neospin-Casino-Brings-Live-Gaming-Experience-to-Virtual-Platforms-04-16-2

References:

Hollywood casino tunica ms

References:

https://gitea.nongnghiepso.com/sherlenecheney

casino https://graph.org/Fresh-spin-casino-australia-Changes-Gamble-Entertainment-04-16

References:

Internet casino

References:

https://interior01.netpro.co.kr:443/bbs/board.php?bo_table=free&wr_id=66

casino https://telegra.ph/Harrys-casino-online-and-the-Astronaut-Crash-Game-Phenomenon-04-16-6

casino https://graph.org/Harry-casino-brings-Plinko-into-contemporary-gaming-era-04-16-6

rhino pills vs viagra generic for viagra women viagra

casino https://graph.org/Napoléon-Games-révolutionne-le-domaine-des-cartes-gratter-04-16-3

viagra honey viagra 100mg price how fast does viagra work

casino https://telegra.ph/MisterGreen-Casino-og-Bonus-Buy-Muligheder-04-16-10

casino https://graph.org/Grand-prize-Fruit-machines-und-MrGreen-Spiele-04-16-5

References:

Valley view casino center seating chart

References:

https://internskill.in/companies/candy96-online-casino-australia-100-welcome-bonus-and-other-bonuses/

References:

Nu metro montecasino

References:

https://classifieds.ocala-news.com/author/veta3924481

can you still take viagra with high blood pressure medication will 5 year old viagra work cost of viagra

References:

Blackjack mountain oklahoma

References:

http://www.jobteck.co.in/companies/candy96-no-deposit-bonus-free-spins-no-card-needed/

viagra para hombres is viagra safe can you take viagra daily

References:

Vernon casino

References:

https://www.barbadossothebysrealty.com/story/online-casino-structure-australia

Platforma obsługuje wygodne formy płatności, w tym BLIK kompatybilny z bankami mBank, ING, PKO BP, Pekao i Millennium, a także popularne karty Visa i Mastercard (Maestro). Pozytywne opinie użytkowników publikowane w serwisach Trustpilot oraz Opinie.com potwierdzają wysoki poziom zaufania do marki. Miłośnicy gry na smartfonach mogą korzystać z dedykowanej aplikacji dostępnej na urządzenia z systemem iOS oraz Android, która zapewnia płynną i stabilną rozgrywkę. Slottica to nie tylko polskie kasyno internetowe, lecz także przestrzeń, w której możesz cieszyć się grą i wygrywać na własnych zasadach.

casino https://kaamkaaziclub.com/read-blog/7228_playtech-revolutionises-online-gaming-with-real-dealers.html

NineCasino https://pcassessoria.digital/

viagra before and after size viagra otc viagra for sale

NineCasino https://pcassessoria.digital/

NineCasino https://pcassessoria.digital/

NineCasino https://pcassessoria.digital/

NineCasino https://pcassessoria.digital/

NineCasino https://pcassessoria.digital/

how to get viagra honey viagra can you take viagra with antidepressants

References:

Spongebob blackjack http://bbs.makegs.com/home.php?mod=space&uid=629340

References:

Schecter blackjack atx c 1 https://myreadinglists.com/News/attention-required-cloudflare-1/

References:

William hill mobile betting https://bom.so/msyng7

viagra canada can you get viagra over the counter long term side effects of viagra

References:

Choctaw casino durant ok https://argrathi.stars.ne.jp:443/pukiwiki/index.php?rivashinson222258

References:

Sarnia casino https://is.gd/8QER4P

References:

Blackjack boots https://blender.community/danielsenhede/

cialis and blood pressure difference between viagra and cialis cialis headache

cialis ad cialis doses cialis time to work

cialis dosage how fast does cialis work how fast does cialis work

cialis vs sildenafil cialis headache cialis medication

mixing viagra and cialis reddit buy cialis cialis half life

buying tadalafil online tadalafil 5 mg tadalafil dose

cialis generic name cialis for women cialis pills

güvenilir oyun alma siteleri pin up

tadalafil tablets tadalafil 20mg tadalafil pulmonary hypertension

does cialis raise blood pressure cialis generic name what does cialis look like

tadalafil 60 mg tadalafil 5mg cialis tadalafil

canadian pharmacy cialis side effects of cialis cialis reviews

tadalafil vs cialis maxim peptide tadalafil review tadalafil online

hims cialis cialis goodrx maximum dose of cialis

buy tadalafil tadalafil peptide tadalafil interactions

max dose of cialis when can i take viagra after taking cialis roman cialis

sildenafil 100mg how long does it last sildenafil 20 mg not working how to take sildenafil

viagra para mujer viagra tablet best viagra for men

buy sildenafil how does sildenafil work how does sildenafil work

viagra para mujeres does viagra work how long does it take for viagra to work

maximum dose of sildenafil in 24 hours cialis vs sildenafil is it ok to take 100mg of sildenafil

how does viagra work does viagra work cbd viagra gummies

sildenafil or tadalafil sildenafil 20 mg para que sirve hims sildenafil review

how long does viagra take to work viagra boys how long does it take for viagra to work

References:

George thorogood i drink alone https://employmentabroad.com/companies/instant-withdrawal-casinos-australia-2026-fast-payout-casinos/

U nas założenie konta zajmuje minutę – działamy szybko i bez zbędnych formularzy. Logowanie do Slottica obsługujemy klasycznie przez e-mail i hasło, a dodatkowo łączymy konta z Google, X (Twitter) i Telegramem. Wybierasz to, co dla Ciebie najwygodniejsze.

References:

Caesars casino windsor http://dailyplaza.co.kr/bbs/board.php?bo_table=1302&wr_id=307520

sildenafil 20 mg para que sirve viagra vs sildenafil sildenafil reviews

References:

Casino santa fe https://suprasage.com/noreen12o7268

benefits of taking viagra daily viagra para mujeres herbal viagra

sildenafil prices sildenafil oral jelly 100mg kamagra sildenafil 20 mg tablet

Marka Vavada pojawiła się na scenie w 2017 roku z garścią slotów w ofercie. Od tamtej chwili przeszła długą drogę – dziś w jej katalogu znajdziesz nie tylko automaty, lecz także klasyczne gry stołowe, jackpoty i rozbudowane kasyno na żywo. Z lokalnego debiutanta Vavada stała się graczem globalnym, a w Polsce zdobyła sympatię użytkowników dzięki prostym zasadom, licencji Curaçao oraz wygodnym płatnościom w złotówkach. To konsekwentne podejście sprawia, że marka systematycznie wzmacnia swoją pozycję w świecie iGamingu.

cialis vs viagra what to expect when husband takes viagra generic for viagra

does sildenafil make you last longer roman sildenafil sildenafil prices

viagra without a prescription rhino pills vs viagra viagra cvs

tadalafil generic goodrx tadalafil how long does it take tadalafil to work

tadalafil 10mg reviews tadalafil 20 mg para que sirve tadalafil 20mg cost

cheap tadalafil tadalafil 10mg tadalafil side effects long term

vardenafil vs tadalafil vs sildenafil tadalafil dosage 40 mg buy tadalafil online

tadalafil 20 mg side effects tadalafil generic name 10 mg tadalafil

generic tadalafil 20mg price is tadalafil a controlled substance tadalafil 5mg price

tadalafil cost walmart tadalafil benefits viagra vs tadalafil

tadalafil pill tadalafil over the counter tadalafil 20mg price

side effects of tadalafil tadalafil reviews amino tadalafil

how long does cialis take to work can women take cialis cialis daily dose

tadalafil dosage tadalafil tablets vardenafil vs tadalafil vs sildenafil

cialis and alcohol cialis 5mg cheap cialis

how to take tadalafil tadalafil side effects tadalafil side effects long-term

cialis vs viagra generic cialis name what is cialis

References:

Ameristar casino council bluffs https://https://peatix.com/user/29688388/view/user/29688388/view

References:

Online casino usa https://urlscan.io/result/019e510d-93f3-73d9-9444-2ba6f03ff66f/

tadalafil 20 mg price tadalafil brand name sildenafil vs tadalafil

References:

Casino slots online https://xypid.win/story.php?title=hitnspin-casino-%E1%90%89-bonus-2026-erfahrungen-und-test

cialis or viagra cialis for women cialis 5mg price

References:

Coeur d’alene casino https://prpack.ru/user/smellbolt92/

tadalafil 20 mg tablet how long does it take for tadalafil to work difference between tadalafil and sildenafil

can i take two 5mg cialis at once cialis over the counter viagra and cialis together

tadalafil alcohol tadalafil 10mg reviews tadalafil drug class

liquid cialis cheap cialis max dose of cialis

tadalafil side effects long term tadalafil side effects long-term tadalafil dosage 60 mg

ии для создания презентаций [url=www.litteraesvfu.ru]www.litteraesvfu.ru[/url]

cialis dosage which is better cialis or viagra 10mg cialis

References:

Mr green casino http://lukovich.ru/user/okraton43/

References:

Aspers casino stratford https://forum.board-of-metal.org/user-50234.html

зимние комбинезоны [url=http://detskie-kombinezony-kupit.ru]зимние комбинезоны[/url]

References:

Treasure bay casino https://nutritionwiki.space/wiki/Social_Casino_Deutschland_mit_Top_Slots_Boni

капельница от похмелья цена [url=https://kapelnicza-ot-pokhmelya-samara-39.ru]https://kapelnicza-ot-pokhmelya-samara-39.ru[/url]

выведение из запоя самара [url=https://kapelnicza-ot-pokhmelya-samara-38.ru]https://kapelnicza-ot-pokhmelya-samara-38.ru[/url]

сколько стоит прокапаться [url=https://kapelnicza-ot-pokhmelya-samara-40.ru]https://kapelnicza-ot-pokhmelya-samara-40.ru[/url]

Your article helped me a lot, is there any more related content? Thanks!

when to take cialis side effects of cialis cialis coupon

создать презентацию ии [url=https://www.litteraesvfu.ru]https://www.litteraesvfu.ru[/url]

врач нарколог анонимно [url=https://narkolog-na-dom-moskva-27.ru]врач нарколог анонимно[/url]

мебельные ткани [url=https://tkan-dlya-mebeli.ru]https://tkan-dlya-mebeli.ru[/url]

капельница от запоя на дому круглосуточно [url=https://kapelnicza-ot-pokhmelya-samara-38.ru]капельница от запоя на дому круглосуточно[/url]

прокапаться от алкоголя цена [url=https://kapelnicza-ot-pokhmelya-samara-39.ru]прокапаться от алкоголя цена[/url]

References:

Greenbrier casino http://www.qazaqpen-club.kz/en/user/suedeniece74/

комбинезон для девочки зимний [url=https://www.detskie-kombinezony-kupit.ru]комбинезон для девочки зимний[/url]

капельница на дому сколько стоит [url=https://kapelnicza-ot-pokhmelya-samara-40.ru]https://kapelnicza-ot-pokhmelya-samara-40.ru[/url]

выведение из запоя больница [url=https://vyvod-iz-zapoya-v-staczionare-sankt-peterburg-27.ru]выведение из запоя больница[/url]

купить корпоративные подарки с логотипом [url=https://suvenirnaya-produkcziya-s-logotipom-8.ru]https://suvenirnaya-produkcziya-s-logotipom-8.ru[/url]

сделать презентацию ии [url=http://www.litteraesvfu.ru]http://www.litteraesvfu.ru[/url]

luxury car rental in miami [url=www.luxury-car-rental-miami-1.com]luxury car rental in miami[/url]

мелбет [url=https://tcso-begovoy.ru]мелбет[/url]

мебельные ткани цена [url=https://tkan-dlya-mebeli.ru]https://tkan-dlya-mebeli.ru[/url]

частный нарколог на дом быстро [url=https://narkolog-na-dom-moskva-27.ru]частный нарколог на дом быстро[/url]

References:

Roulette blackshot https://commonwiki.space/wiki/Und_Auszahlungsmethoden_des_HitnSpin_Casinos

melbet скачать [url=https://tcso-begovoy.ru]melbet скачать[/url]

luxury car rental in miami executive airport [url=https://www.luxury-car-rental-miami-1.com]https://www.luxury-car-rental-miami-1.com[/url]

капельница от похмелья самара [url=https://kapelnicza-ot-pokhmelya-samara-38.ru]https://kapelnicza-ot-pokhmelya-samara-38.ru[/url]

капельница от запоя [url=https://kapelnicza-ot-pokhmelya-samara-39.ru]капельница от запоя[/url]

создание презентаций ии [url=http://litteraesvfu.ru]http://litteraesvfu.ru[/url]

капельница от алкоголя в стационаре [url=https://vyvod-iz-zapoya-v-staczionare-sankt-peterburg-27.ru]капельница от алкоголя в стационаре[/url]

бизнес подарки интернет магазин [url=http://www.suvenirnaya-produkcziya-s-logotipom-8.ru]http://www.suvenirnaya-produkcziya-s-logotipom-8.ru[/url]

мелбет приложение [url=https://tcso-begovoy.ru]мелбет приложение[/url]

References:

Red casino https://commonwiki.space/wiki/Offizielle_Website_Schnelle_Auszahlungen_fr_Deutschland

лечение алкоголизма вызов на дом [url=https://narkolog-na-dom-moskva-27.ru]лечение алкоголизма вызов на дом[/url]

комбинезон ярко [url=http://www.detskie-kombinezony-kupit.ru]http://www.detskie-kombinezony-kupit.ru[/url]

References:

Hardrock casino florida https://hedgedoc.info.uqam.ca/s/IHoyqgJ_k

мел бет [url=https://limon-ads.ru]мел бет[/url]

References:

Penny slot machines https://pad.stuve.uni-ulm.de/s/yKoHFiMBp

References:

Silverton casino https://aryba.kg/user/dinnersmoke5//user/dinnersmoke5/

References:

Casinos en las vegas https://materialwiki.site/wiki/Vulkan_Vegas_Bonus_7_Codes_Gutschein_ohne_Einzahlung

References:

Egyptian treasures https://xypid.win/story.php?title=nv-casino-auszahlung-2026-methoden-limits-und-bearbeitungszeit

melbet скачать [url=https://tcso-begovoy.ru]melbet скачать[/url]

ткань мебельная купить в розницу [url=https://tkan-dlya-mebeli.ru]https://tkan-dlya-mebeli.ru[/url]

определить по номеру телефона где находится человек [url=https://kak-najti-cheloveka-po-nomeru-telefona-2.ru]https://kak-najti-cheloveka-po-nomeru-telefona-2.ru[/url]

скачать мелбет на андроид [url=https://elenagatilova.ru]скачать мелбет на андроид[/url]

вывести из запоя в стационаре санкт петербург [url=https://vyvod-iz-zapoya-v-staczionare-sankt-peterburg-27.ru]вывести из запоя в стационаре санкт петербург[/url]

мелбет скачать [url=https://tcso-begovoy.ru]мелбет скачать[/url]

References:

Mystic island casino https://earthwiki.space/wiki/Legiano_Casino_Konto_Verifizierung_Leitfaden

мелбет приложение [url=https://limon-ads.ru]мелбет приложение[/url]

References:

Blackjack hands http://amur.1gb.ua/user/bargeball6/

презентация ии [url=www.litteraesvfu.ru]www.litteraesvfu.ru[/url]

References:

Borgata casino https://https://melton-andresen.mdwrite.net/online-casino-mit-slots-live-casino-und-attraktiven-boni/online-casino-mit-slots-live-casino-und-attraktiven-boni

References:

Best online translator https://a-taxi.com.ua/user/movestone27/

детский комбинезон зимний для новорожденных [url=www.detskie-kombinezony-kupit.ru]детский комбинезон зимний для новорожденных[/url]

скачать melbet на андроид [url=https://elenagatilova.ru]скачать melbet на андроид[/url]

References:

Casinobonus https://https://eggswiki.site/wiki/Spiele_Echtgeldspiele_online_gewinne_tglich_gro/wiki/Spiele_Echtgeldspiele_online_gewinne_tglich_gro

локация по номеру телефона [url=http://kak-najti-cheloveka-po-nomeru-telefona-2.ru]http://kak-najti-cheloveka-po-nomeru-telefona-2.ru[/url]

корпоративные сувениры с логотипом [url=https://suvenirnaya-produkcziya-s-logotipom-8.ru]https://suvenirnaya-produkcziya-s-logotipom-8.ru[/url]

melbet скачать [url=https://limon-ads.ru]melbet скачать[/url]

мелбет казино скачать на андроид [url=https://elenagatilova.ru]мелбет казино скачать на андроид[/url]

References:

Online sport betting https://www.forum-joyingauto.com/member.php?action=profile&uid=145654/member.php?action=profile&uid=145654

References:

Harrah’s new orleans casino https://https://intensedebate.com/people/bonsaicarol12/people/bonsaicarol12

References:

Top online casino https://https://school-of-safety-russia.ru/user/beggarcrayon71//user/beggarcrayon71/

Слушайте, кому актуально, толковый разбор. Многие спрашивали, в итоге скачал отсюда: [url=https://teobit.ru]мелбет скачать приложение[/url].

Этот букмекер радует удобным интерфейсом, коэффициенты вполне адекватные. Порадовало, что трансляции матчей идут без задержек.

Для новых пользователей можно неплохо увеличить первый депозит, рекомендую воспользоваться. Всем удачи!

References:

Fitzgerald casino tunica https://https://bush-yildirim-3.mdwrite.net/casino-blog-casino-spiele-anleitungen-tipps-and-tricks-888-casino/casino-blog-casino-spiele-anleitungen-tipps-and-tricks-888-casino

вызов нарколога круглосуточно [url=https://narkolog-na-dom-moskva-27.ru]вызов нарколога круглосуточно[/url]

References:

Online casino sites https://https://500px.com/p/mcgarrywjdliu/p/mcgarrywjdliu

References:

Mac casino https://www.https://www.forum-joyingauto.com/member.php?action=profile&uid=145706/member.php?action=profile&uid=145706

детский полукомбинезон [url=detskie-kombinezony-kupit.ru]детский полукомбинезон[/url]

мелбет казино скачать на андроид [url=https://elenagatilova.ru]мелбет казино скачать на андроид[/url]

References:

Casino oline https://telegra.ph/HitnSpin-Casino-Erfahrung-2026–800-Bonus-App–Spiele-06-07

выведение из запоя в стационаре [url=https://vyvod-iz-zapoya-v-staczionare-sankt-peterburg-27.ru]выведение из запоя в стационаре[/url]

References:

Casino rewards https://xtuml.org/author/lentileagle28/

Чтобы быстро и эффективно [url=https://kak-najti-cheloveka-po-nomeru-telefona-3.ru]официальный сайт[/url], воспользуйтесь такими штуками которые дают инфу.

В общем, тема такая, не для паники.

Применяйте полученные данные обдуманно и исключительно в рамках закона.

Короче, не нарывайтесь.

Народ, приветствую. Дело деликатное, но решил черкануть пару строк, потому что в экстренной ситуации трудно сориентироваться. Когда нужен проверенный и опытный врач для капельницы, важно, чтобы доктора отреагировали оперативно.

Знакомые вызывали бригаду в похожей ситуации и в итоге нашли клинику, где врачи работают профессионально. Кому тоже нужны подробности и условия, вся информация есть здесь: вывод из запоя санкт петербург стационар [url=https://vyvod-iz-zapoya-v-staczionare-sankt-peterburg-28.ru]вывод из запоя санкт петербург стационар[/url].

Там расписаны все аспекты, которые стоит учитывать, реагируют очень быстро, буквально за час. Надеюсь, эта рекомендация и обращайтесь к настоящим профессионалам. Всем удачи и берегите близких!

Слушайте, кому актуально, толковый разбор. Многие спрашивали, делюсь полезной ссылкой: [url=https://teobit.ru]скачать мелбет на айфон[/url].

Сам сервис сейчас один из лучших, все интуитивно понятно даже новичку. Порадовало, что выплаты приходят достаточно быстро.

Там сейчас можно неплохо увеличить первый депозит, лишним точно не будет. Пишите, если возникнут вопросы.

Народ, приветствую. Тема здоровья всегда на первом месте, потому что в экстренной ситуации трудно сориентироваться. Если ищете анонимного специалиста с быстрым выездом по городу, то не рискуйте и не доверяйте случайным объявлениям.

Знакомые вызывали бригаду в похожей ситуации и в итоге нашли клинику, где врачи работают профессионально. Если вам актуально или ситуация экстренная, советую посмотреть официальный источник: [url=https://narkolog-na-dom-moskva-27.ru/]перейти по ссылке[/url].

На этом сайте действительно дана полная информация, так что найдете ответы на свои вопросы. Надеюсь, эта рекомендация поможет вовремя принять правильные меры. Пусть все будет хорошо!

капельница от алкоголя в стационаре [url=https://vyvod-iz-zapoya-v-staczionare-sankt-peterburg-27.ru]капельница от алкоголя в стационаре[/url]

melbet скачать [url=https://limon-ads.ru]melbet скачать[/url]

узнать где находится человек по номеру телефона [url=www.kak-najti-cheloveka-po-nomeru-telefona-2.ru]www.kak-najti-cheloveka-po-nomeru-telefona-2.ru[/url]

References:

Don johnson blackjack https://topsitenet.com/profile/drawmail97/1872041//profile/drawmail97/1872041/

Слушайте, реально замучилась искать нормальную платформу для дочки. Везде одна вода или заоблачные ценники. Соседка по площадке посоветовала глянуть вот этот проект: [url=https://shkola-onlajn-53.ru]онлайн школа 8 класс[/url] . Пришлось признать, что был не прав. Успеваемость подтянулась, особенно по точным наукам. Объясняют на пальцах, без лишней воды. Плюс огромный – никаких больничных, заболел – смотришь записи. Для современных детей самое то, ИМХО.

психиатр нарколог на дом в москве [url=https://narkolog-na-dom-moskva-28.ru]психиатр нарколог на дом в москве[/url]

Чтобы быстро и эффективно [url=https://kak-najti-cheloveka-po-nomeru-telefona-3.ru]источник[/url], воспользуйтесь такими штуками которые дают инфу.

В общем, тема такая, не для паники.

Во многих случаях имеет смысл начать с проверки общедоступных интернет-ресурсов.

Короче, не нарывайтесь.

References:

Wild rose casino clinton iowa https://gaiaathome.eu/gaiaathome/show_user.php?userid=1977750

Народ, если кто искал, рабочая тема. Сам долго ковырялся, в итоге скачал отсюда: [url=https://teobit.ru]melbet[/url].

Кстати, площадка реально топовый — все интуитивно понятно даже новичку. Плюс ко всему выплаты приходят достаточно быстро.

Там сейчас капает бонус на баланс, так что можно затестить. Кто уже ставил там?

Güvenli bahis deneyimi için [url=https://1xbet-giris-78.com]1xbet spor bahislerinin adresi[/url] adresini kullanabilirsiniz.

günümüzde oldukça basit. Giriş yaparken dikkat edilmesi gereken bazı noktalar vardır. Kullanıcılar giriş yapmak için doğru siteyi seçmelidir. Site güvenliğine verilen önem yüksektir.

1xbet giriş ekranına ulaşmak için sayfanın üst kısmındaki giriş butonuna tıklanmalıdır. Kullanıcı adı ve şifre alanları özenle doldurulmalıdır. Sahte sitelere karşı dikkatli olunması önerilir.

Üyeliğiniz yoksa, kayıt işlemi birkaç dakika içinde tamamlanabilir. Bilgilerin eksiksiz ve doğru doldurulması önem taşır. Doğrulama aşamasında telefon veya e-posta onayı gerekebilir.

1xbet girişi yaptıktan sonra pek çok fırsattan yararlanabilirsiniz. Çeşitli spor dallarında bahis yapma imkanı sunulur. Ayrıca güncel promosyonlar ve bonuslar takip edilebilir.

References:

G casino luton https://https://literaturewiki.site/wiki/1go_Casino_im_Test_Lohnt_sich_der_Einstieg_2026_wirklich/wiki/1go_Casino_im_Test_Lohnt_sich_der_Einstieg_2026_wirklich

Для тех, кто в теме, свежая инфа. Сам долго ковырялся, все работает без проблем здесь: [url=https://teobit.ru]мелбет казино скачать[/url].

Вообще проект сейчас один из лучших, выбор спортивных дисциплин впечатляет. Плюс ко всему выплаты приходят достаточно быстро.

Если только заводите аккаунт активируется стартовый фрибет, так что можно затестить. Что думаете?

Чтобы быстро и эффективно [url=https://kak-najti-cheloveka-po-nomeru-telefona-3.ru]официальный сайт[/url], воспользуйтесь нормальными ребята реально помогают.

Знаете, многие лезут в дебри, а зря.

Оператор не имеет права выдать сведения о подписчике без соответствующего юридического основания.

Надеюсь, понятно объяснил.

References:

Play roulette online https://intensedebate.com/people/womanraven36/people/womanraven36

Давно присматривался к разным предложениям, где реально учат делу. Особенно когда речь про образовательные онлайн школы — тут ведь без фанатизма и воды. У меня сын как раз начал учиться дистанционно, так что пришлось перебрать кучу вариантов. В общем, вся подробная информация вот тут: онлайн школа 8 класс [url=https://shkola-onlajn-55.ru]https://shkola-onlajn-55.ru[/url] Я если кому интересно ещё раньше вообще не верил в онлайн образование школа. Оказалось — реально работает. У них и обратная связь отличная. Сам теперь советую знакомым. Удачи!