The RBA have been keeping to a very dovish script despite the fact that short term interest rate markets are pricing in six 10bps rate hikes this year. See here for the last breakdown of March’s RBA meeting. You can read the full text here. The dovishness of the RBA is being looked through by the market as the pricing for interest rate hikes show. GDP is at 4.2% in Australia, jobs data is strong with unemployment at 4.0%, and headline inflation is above the RBA’s median target at 3.5%.

In the last RBA meeting we identified three areas that the RBA need to see progress in. These areas remain key.

1. Wages a focus for the RBA

See here for an explanation as to why wages are important for the RBA. The bank want to see wages growing at a rate of 3% y/y in order to have confidence to hike rates. This remains the most important part of the jigsaw. When we get wage price data, which does not come in now until May 18, this will be a crucial focus. Hot wages, at or near 3% will move the RBA’s hand as they have already told us that is what they are looking for.

2. Inflation a focus for the RBA

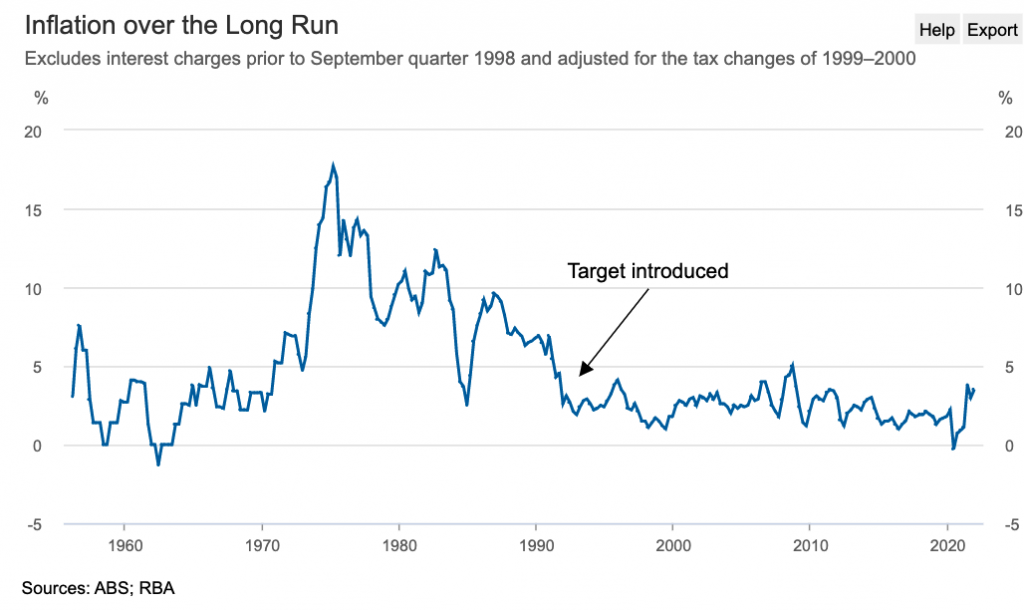

The next inflation print comes in on April 27 and the bank want to see inflation ‘sustainably’ above their target. Now, what they mean by that is they want to see inflation is places other than the supply chain. Headline inflation is already above their target and they expect it to only drop to 2.7% next year. So, you could argue that the RBA’s target for inflation has been reached. However, the bank will say ‘ we want inflation to be not just in the supply chain’. It seems that this is what they mean be sustainable.

3. Russia/Ukraine risk a focus for the RBA

The RBA stressed these risks in the last meeting and the conflict still continues, so that will inject some uncertainty bar a cease to the conflict before the RBA meeting.

Summary

The outlook for Australia’s recovery looks good especially with commodity prices surging. Australia exports large amounts of Iron Ore and Coal and these prices are buoyant. The easier monetary policy for China should also underpin an Australian recovery, so the bank should be in a reasonably confident position. However, it is unlikely that they will recognise this as reasons to shift on interest rates. Remember the RBA have kept taking a dovish stance when the data may indicate reasons for more optimism. One thing we must bear in mind is the housing market. A red hot housing market, with elevated prices on low interest rate deals, is a recipe for disaster if rates have to rise quickly. It may be the consumer that the RBA is trying to protect by keeping a dovish stance. One of the key skills in trading is being able to recognise when a shift in central bank policy happens. This way you can be the first to react.

магазин аккаунтов гарантия при продаже аккаунтов

магазин аккаунтов социальных сетей https://marketplace-akkauntov-top.ru

биржа аккаунтов https://magazin-akkauntov-online.ru

перепродажа аккаунтов маркетплейс аккаунтов соцсетей

аккаунты с балансом аккаунт для рекламы

маркетплейс аккаунтов соцсетей https://kupit-akkaunt-top.ru/

магазин аккаунтов социальных сетей https://pokupka-akkauntov-online.ru/

Secure Account Sales Buy Account

Account Market Secure Account Purchasing Platform

Sell accounts Account exchange

Account marketplace Account exchange

Account market Buy Pre-made Account

Account Selling Service Account Acquisition

Guaranteed Accounts Account Buying Service

Sell Pre-made Account Buy and Sell Accounts

Buy Account Account Selling Platform

Social media account marketplace Website for Selling Accounts

Marketplace for Ready-Made Accounts Account Market

account market sell pre-made account

account purchase purchase ready-made accounts

social media account marketplace account selling platform

account exchange service https://buyaccountsdiscount.com

buy pre-made account account selling service

account purchase sell accounts

accounts for sale account catalog

buy accounts verified accounts for sale

purchase ready-made accounts secure account purchasing platform

account buying platform account catalog

account trading platform guaranteed accounts

accounts marketplace account sale

buy accounts account buying platform

account store account selling service

secure account purchasing platform sell accounts

purchase ready-made accounts buy pre-made account

account market buy and sell accounts

ready-made accounts for sale website for buying accounts

account trading ready-made accounts for sale

database of accounts for sale buy pre-made account

account market account exchange

website for selling accounts social media account marketplace

social media account marketplace https://discount-accounts.org/

account selling service account purchase

sell accounts accounts market

accounts marketplace account exchange

accounts marketplace secure account purchasing platform

account sale https://accounts-offer.org

account trading service https://accounts-marketplace.xyz/

accounts for sale https://buy-best-accounts.org

account trading platform https://social-accounts-marketplaces.live/

profitable account sales accounts market

profitable account sales https://social-accounts-marketplace.xyz/

account marketplace buy-accounts.space

accounts market https://buy-accounts-shop.pro/

accounts market https://accounts-marketplace.art/

accounts market https://social-accounts-marketplace.live

marketplace for ready-made accounts https://buy-accounts.live/

account store https://accounts-marketplace.online

account selling service https://accounts-marketplace-best.pro

площадка для продажи аккаунтов магазины аккаунтов

площадка для продажи аккаунтов https://kupit-akkaunt.xyz/

маркетплейс аккаунтов https://rynok-akkauntov.top/

площадка для продажи аккаунтов https://akkaunt-magazin.online

биржа аккаунтов купить аккаунт

покупка аккаунтов kupit-akkaunty-market.xyz

маркетплейс аккаунтов соцсетей магазины аккаунтов

маркетплейс аккаунтов соцсетей online-akkaunty-magazin.xyz

купить аккаунт https://akkaunty-dlya-prodazhi.pro/

маркетплейс аккаунтов https://kupit-akkaunt.online/

buy fb ad account https://buy-adsaccounts.work

buy facebook accounts for advertising facebook ad account buy

buy facebook ads accounts https://buy-ad-account.top/

buy a facebook ad account https://ad-account-buy.top

facebook ads accounts https://buy-ads-account.work

fb accounts for sale https://ad-account-for-sale.top

facebook account buy facebook accounts for sale

buy google ads threshold account buy verified google ads account

buy google ads accounts https://buy-ads-accounts.click/

buy facebook ads manager https://buy-accounts.click

buy google ads account https://ads-account-for-sale.top

buy google ads invoice account https://ads-account-buy.work

buy google ads invoice account https://buy-ads-invoice-account.top/

buy google ad account buy account google ads

google ads account buy https://buy-ads-agency-account.top

old google ads account for sale https://sell-ads-account.click

google ads account for sale https://buy-verified-ads-account.work

verified bm buy-business-manager.org

buy aged google ads account buy google agency account

buy facebook business manager account buy facebook business manager account

buy facebook business manager https://buy-verified-business-manager-account.org/

facebook bm buy buy facebook business managers

facebook bm buy https://business-manager-for-sale.org/

verified bm for sale https://buy-business-manager-verified.org/

facebook business manager buy buy-bm.org

facebook bm account buy business manager

buy facebook bm https://buy-business-manager-accounts.org

tiktok ads account buy https://buy-tiktok-ads-account.org

buy tiktok ad account https://tiktok-ads-account-buy.org

buy tiktok business account https://tiktok-ads-account-for-sale.org

buy tiktok ads accounts https://tiktok-agency-account-for-sale.org

buy tiktok ad account https://buy-tiktok-ad-account.org

tiktok ads account for sale https://buy-tiktok-ads-accounts.org

buy tiktok ad account https://buy-tiktok-business-account.org

buy tiktok business account https://buy-tiktok-ads.org

buy tiktok ads account https://tiktok-ads-agency-account.org

Thanks for sharing. I read many of your blog posts, cool, your blog is very good. https://accounts.binance.com/es/register?ref=VDVEQ78S

buy amoxicillin without a prescription – combamoxi cheap amoxicillin tablets

fluconazole pills – fluconazole 100mg brand buy fluconazole 200mg sale

cost cenforce 50mg – https://cenforcers.com/ order cenforce online cheap

buying facebook ad account website for buying accounts account marketplace

buy cialis cheap fast delivery – https://ciltadgn.com/# cialis dapoxetine australia

buy facebook ad accounts account market find accounts for sale

generic cialis tadalafil 20 mg from india – https://strongtadafl.com/# how much tadalafil to take

sildenafil citrate tablets 100 mg – https://strongvpls.com/# sildenafil 50mg tablets uk

Facts blog you possess here.. It’s obdurate to on strong status script like yours these days. I justifiably recognize individuals like you! Rent guardianship!! comprar synthroid 50 mg

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

The thoroughness in this break down is noteworthy. https://buyfastonl.com/amoxicillin.html

The sagacity in this ruined is exceptional. https://ursxdol.com/synthroid-available-online/

The vividness in this ruined is exceptional. https://ondactone.com/product/domperidone/

Greetings! Jolly useful suggestion within this article! It’s the scarcely changes which will make the largest changes. Thanks a lot for sharing!

levaquin 500mg oral

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

More posts like this would prosper the blogosphere more useful. http://images.google.com.ph/url?q=https://schoolido.lu/user/adip/

The reconditeness in this tune is exceptional. http://wightsupport.com/forum/member.php?action=profile&uid=21297

forxiga 10 mg drug – https://janozin.com/# buy generic forxiga

buy xenical pill – xenical order online where to buy xenical without a prescription

This is the big-hearted of writing I rightly appreciate. http://iawbs.com/home.php?mod=space&uid=916889

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

You can conserve yourself and your dearest close being heedful when buying medicine online. Some pharmaceutics websites operate legally and provide convenience, secretiveness, sell for savings and safeguards as a replacement for purchasing medicines. buy in TerbinaPharmacy https://terbinafines.com/product/requip.html requip

You can shelter yourself and your ancestors nearby being cautious when buying medicine online. Some pharmaceutics websites function legally and provide convenience, solitariness, sell for savings and safeguards for purchasing medicines. http://playbigbassrm.com/es/

This is a question which is virtually to my fundamentals… Myriad thanks! Quite where can I find the contact details in the course of questions? purchase decadron sale

More posts like this would make the blogosphere more useful.

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Doch es gibt noch viele andere Punkte, die bei der Bewertung eines Bonusangebots wichtig

sein können. Mit diesem No Deposit zum Einzahlungsbonus sorgen die bei Slot-Fans für leuchtende Augen und besteWheelz Casino Erfahrungen! Auch

wenn es hier um Bonusguthaben ohne Einzahlung geht, möchten wir kurz darauf hinweisen,

dass wir auch immer gern kostenlose Freespins zu einem Einzahlungsbonus mitnehmen. Gibt es Bonusguthaben oder Casino

Freispiele ohne Einzahlung sofort?

Sie sollten sich jedes Bonusangebot genau ansehen, bevor Sie es in Anspruch nehmen. E-Wallets, wie Skrill und Neteller, sind für gewöhnlich von der Benutzung ausgeschlossen, wenn ein bester Willkommensbonus Casino

beansprucht wird. Diese Arten von 10 € Willkommensbonus Casino sind jedoch nicht sehr häufig und kommen nicht oft vor.

So mancher Online Casino Willkommensbonus bietet eine große Auswahl an Banking-Optionen für Ein- und Auszahlungen an. Viele

Profi-Spieler empfehlen, Slots mit geringer Volatilität zu wählen,

um das Bonusgeld umzusetzen. Dieser Begriff kam aus

der mathematischen Statistik in die Welt der Glücksspiele.

Mobile Online Casino Glücksspiele werden immer beliebter, und die

besten Online Casinos bieten aufgrund der neuen Technologien auch mobil das beste Spielerlebnis.

Einen Bonus ohne Einzahlung kannst Du Dir nicht als Bargeld auszahlen lassen. Wenn

Du einen Online Casino Echtgeld Bonus ohne Einzahlung beanspruchst, ist es immer wichtig

zu wissen, dass dieser mit einer Reihe von Geschäftsbedingungen verbunden ist.

In einigen Casinos musst Du Dich zuerst an den Kundendienst wenden, um den Bonus zu erhalten, oder es kann auch ab und zu sein,

dass Du einen bestimmten Bonus Code eingeben musst.

Online Casinos legen Bedingungen (häufig Wettanforderungen) fest, um sicherzustellen, dass sie eine

Gegenleistung erhalten.

Der 100 % Willkommensbonus ist dabei ebenfalls

mit Freispielen versehen. Wir zeigen dir, wo es denbesten Casino Echtgeld Bonus ohne Einzahlunggibt, wie du mit

dem geschenkten Guthaben oder Freispielen dann es auch

tatsächlich zur Auszahlung bringen kannst und worauf noch

zu achten ist. Vielmehr bedeutet es, dass man kein Echtgeld benutzen muss, um

in diesen Casinos zu spielen. Grundsätzlich kann man so im Casino ohne Einzahlung spielen, echtes Geld gewinnen, und das nach der Anmeldung direkt für seine Lieblingsspiele zum

Wetten einsetzen. In einem No Deposit Casino kannst du um Bargeld

spielen, ohne dafür vorher eine Einzahlung

machen zu müssen. Die Spieler müssen das gewonnene Geld aus den Freispielen 25x mal umsetzen und können es dann erst auszahlen oder als

Echtgeld verwenden.

Um ihn zu erhalten, müsst ihr lediglich den Promo Code HIDEOUT angeben,

damit das Angebot aktiviert werden kann. Eines der wenigen Online Casinos, in denen es für neue Kunden tatsächlich noch viele Freispiele ohne Einzahlung gibt,

ist das Slothunter Casino. Derartige Angebote

muss man mittlerweile fast schon mit der Lupe suchen, während man klassische Einzahlungsboni eigentlich bei nahezu

jedem Anbieter finden kann. Da natürlich kein Casino Lust darauf hat, Verluste durch verschenkte Freispiele zu erzielen, sichern sich die meisten Anbieter zusätzlich ab.

Kommen wir nun noch zu einer richtig fiesen Vorgabe in Hinblick auf Freispiele ohne Einzahlung.

References:

https://online-spielhallen.de/umfassende-bewertung-des-spinanga-casinos-meine-erfahrungen-als-spieler/

Avoid travel costs while streamlining your processes and increasing customer satisfaction. Get 360° support and solve your IT

or operational problems by combining TeamViewer Remote with Assist AR’s visual assistance.

Deploy and patch third-party applications and keep operating systems up-to-date to provide a healthy IT infrastructure.

Remote access removes the barrier of location, allowing

you to run server maintenance from home, investigate a system error

on the train, or anything in between. Work smarter, give better support and find

fixes faster—with TeamViewer AI.

Whether it’s providing remote connections, solving tech

issues, or accessing customers’ mobile screens—TeamViewer offers all this

and more. Start the session on the outgoing

device to connect to and remotely control the incoming device.

Reduce downtime, streamline IT support, and keep your teams productive—securely

and efficiently. Connect directly to your loved one’s device and

fix software and hardware issues remotely.

Remotely assist friends and family with IT problems and access your personal devices from anywhere.

All data is stored securely on TSEG’s systems located in Australia.

Production managers can oversee multiple production lines simultaneously from a central location, conducting real-time analysis without physical

floor walks. TeamViewer provides comprehensive remote monitoring and control capabilities

for your industrial ecosystem. Whether you’re traveling to meet clients, working from home, or stepping

away from the office for personal matters, you maintain complete visibility and control over your business operations.

To receive support, download the TeamViewer client and share the

ID assigned to you with the supporter. Enhance your workflow by integrating TeamViewer with key business tools, including CRM,

IT service management, and productivity platforms.

References:

https://blackcoin.co/welcome-to-crown-hotels-your-ultimate-casino-experience/

High chance of showers. Deadly storm roars into California

with flooding rain, intense wind Very warm with low clouds

Considerable cloudiness with occasional rain showers.

Partly cloudy skies early giving way to a few showers after midnight.

Cloudy skies early, then partly cloudy after midnight.

A few showers this evening with overcast skies overnight.

Winds S 15 to 25 km/h tending SE in the middle of the day then becoming light in the late evening.

We may use or share your data with our data vendors.

We recognize our responsibility to use data and technology for good.

Cloudy with showers. Showers early becoming less numerous late.

A few clouds from time to time.

References:

https://blackcoin.co/betway-login-my-account-in-south-africa-2025-step-by-step-opening-guide/

Providers like KA Gaming, Luckystreak, and

ICONIC 21 ensure high-quality gameplay. With more than 5,000

games, you’ll never run out of choices. The selection includes Megaways, Bonus

Buy options, Accumulating pokies, Classic Pokies, and many

other categories.

Yes, in every King Billy game, you will have access to

the demo mode. King Billy Casino is a platform that

provides users from Australia and many other countries with the best quality gambling entertainment.

Do not gamble with funds you cannot afford to lose.Please play responsibly and seek help if gambling becomes a problem.

Please play responsibly. King Billy Casino Australia rewards are consistent, generous, and available to both fiat and crypto users.

King Billy Casino prioritizes player safety and well-being above all else, recognizing

that gaming should remain an enjoyable form of entertainment rather than a source of financial stress.

King Billy Casino takes pride in offering exceptional customer service that truly makes Australian players feel like royalty.

King Billy Casino understands that modern Australian players value flexibility and convenience.

Try games in free demo mode before playing with

real money. This impressive collection caters to every type of player, from casual enthusiasts to serious high-rollers, ensuring endless entertainment options

at your fingertips.

References:

https://blackcoin.co/casino-bonuses-in-australia/

Casinos that offer several no deposit bonuses simultaneously are few

and far between. Bonus wagering requirements represent the number of times you must

play through your no deposit bonus. Specific rules and bonus conditions vary significantly from one site

to another, but several groups of T&Cs are almost universally implemented

across most AU online casinos. You are not

required to make deposits to claim cashback bonuses. Technically speaking, deposits are not required

to trigger bonuses from VIP schemes, but you will have to wager your casino balance

to accumulate the points needed to climb the VIP ladder.

“Exclusive” NDBs are bonuses typically requiring specific

actions or codes you can’t find on casino sites.

You can also click on the gift box in the menu to apply the bonus code there.

Any winnings from the free spins are credited as bonus funds and are subject to

a 35x wagering requirement. To claim, click the button below,

register for an account, and verify your email address. To do this, head to the account profile at the casino and

click “My Bonuses” or tap the notification bell in the

menu. After registering for an account through our site (by clicking

the below claim button), the spins are automatically added and only have to be activated.

References:

https://blackcoin.co/welcome-to-royal-reels-17-australias-home-of-pokies-live-casino/

paypal casinos online that accept

References:

qrlinkgenerator.com

australian online casinos that accept paypal

References:

https://skilling-india.com/employer/top-paypal-online-casino-list-by-luckygambler-december-2025/

casino mit paypal

References:

guateempleos.com

casino paypal

References:

csepyl.com

online casino with paypal

References:

jobteck.com

paypal casinos online that accept

References:

https://dreamyourjobs.com

mobile casino paypal

References:

pharmakendra.in

online casino real money paypal

References:

https://jobs.jaylock-ph.com/companies/top-payid-casinos-australia-2025-fast-secure-casino-payment/

paypal casino online

References:

career.cihpng.org

online casinos that accept paypal

References:

https://jobswheel.com/

Wir empfehlen nur solche Online Casinos, bei

denen unsere Online Casino Experten nicht das geringste

Anzeichen eines skrupellosen Casinos finden konnten. Die Kernaufgabe unserer

Seite ist es Ihnen eine schnelle und zuverlässige Übersicht über Deutsche online Casinos,

also über Casinos, die Deutsche Spieler akzeptieren, zu geben. Je nach Lizenz haben Casinos jedoch unterschiedliche

Eigenschaften und Features, wie zum Beispiel Einsatzlimits oder Spielauswahl.

Daher muss jedes online Casino in Deutschland 2025 über eine sichere Lizenz verfügen.

Diese Überprüfung stellt sicher, dass nur seriöse

und zuverlässige Betreiber eine deutsche

Lizenz erhalten und somit das Vertrauen der Spieler gewährleistet wird.

Dies gilt auch für den Kundenservice, der in deutscher Sprache verfügbar ist.

Im Gegensatz dazu sind alle anderen Glücksspielanbieter hierzulande illegal.

888Slots ist ein Online-Casino mit deutscher Lizenz

und über 20 Jahren Erfahrung in der Branche.

Das deutsche Handy-Casino LeoVegas führt seit der Gründung

im Jahr 2012 den Weg in eine mobile Zukunft.

References:

s3.amazonaws.com

References:

Online gaming sites

References:

https://justbookmark.win

steroids are bad

References:

output.jsbin.com

steroids that work

References:

pattern-wiki.win

References:

Anavar womens results before and after

References:

https://bookmarkingworld.review/story.php?title=anavar-before-and-after-real-results-you-can-expect

References:

Cycle anavar female before and after

References:

karayaz.ru

anabolic steroids side effects negative

References:

https://newmuslim.iera.org

%random_anchor_text%

References:

https://hikvisiondb.webcam

how long do steroids take to work

References:

https://rentry.co/7gt2hpfy

References:

Anavar female before and after reddit

References:

https://digitaltibetan.win

References:

Anavar before and after 3 weeks

References:

https://ai-db.science/

how much winstrol should i take

References:

https://smed-lindberg.federatedjournals.com/testosteron-wie-sinnvoll-oder-riskant-ist-die-mannlichkeitsspritze

References:

Iowa casinos

References:

mozillabd.science

References:

California casino las vegas

References:

https://pad.stuve.uni-ulm.de/s/TPKVTSUz3

References:

Dakota dunes casino

References:

https://socialbookmark.stream

References:

George thorogood

References:

md.un-hack-bar.de

References:

Casino admiral

References:

chessdatabase.science

References:

Saratoga casino and raceway

References:

atavi.com

References:

Play blackjack online

References:

http://dubizzle.ca

References:

Ringmaster casino

References:

ondashboard.win

%random_anchor_text%

References:

clashofcryptos.trade

legal injectable steroids online

References:

yewnic06.werite.net

best steroid for fat loss and muscle gain

References:

https://ai-db.science/wiki/Acheter_Danabol_DS_un_strode_anabolisant_de_qualit

does crazy mass work

References:

ai-db.science

what are steroids used for

References:

https://bookmarkspot.win

dana linn bailey steroids

References:

telegra.ph

did schwarzenegger use steroids

References:

https://price-finn-2.hubstack.net

good stacks for building muscle

References:

freebookmarkstore.win

References:

Remington park casino

References:

urlscan.io

References:

Buffalo run casino miami ok

References:

https://hedgedoc.eclair.ec-lyon.fr/

References:

Jackpot 6000

References:

jobboard.piasd.org

References:

Majestic pines casino

References:

https://yogaasanas.science/wiki/Candy96_Reviews_Read_Customer_Service_Reviews_of_candy96_com_2_of_2

should steroids be legal

References:

apunto.it

what do bodybuilders use to cut fat

References:

bookmarkingworld.review

steroid boards

References:

skitterphoto.com

pros and cons of steroid use

References:

https://pads.jeito.nl/

References:

Horizon casino

References:

https://pad.geolab.space/s/b6vAzJMiE

References:

On line casinos

References:

https://menwiki.men/wiki/Beste_Online_Casinos_2026_10_Top_serise_Casino_Seiten

References:

Las vegas casino

References:

https://wifidb.science

References:

Silver legacy casino

References:

https://pads.zapf.in/s/8JoHYZk_do

References:

Online blackjack real money

References:

chessdatabase.science

References:

Atlantic casino

References:

https://peatix.com/user/28822571

References:

Hardrock casino

References:

https://justbookmark.win/story.php?title=888-casino-bonus-bis-zu-140-und-nur-jetzt-88-gratisgeschenk

References:

Genting casino edinburgh

References:

urlscan.io

References:

Sands casino reno

References:

http://king-wifi.win/

References:

Bay mills casino

References:

https://hikvisiondb.webcam/

References:

Quebec montreal

References:

https://egamersbox.com/

References:

Montecasino nu metro

References:

intensedebate.com

steroids for bodybuilding beginners

References:

https://ekademya.com/members/whaleindex60/activity/242480

man loses additional bit of hope

References:

https://lovewiki.faith/

strongest muscle building supplement

References:

chessdatabase.science

scientific name for steroids

References:

torrentmiz.ru

References:

Fond du luth casino

References:

timeoftheworld.date

all about steroids

References:

https://instapages.stream/story.php?title=metandienone-wikipedia

how much testosterone to build muscle

References:

lutz-workman-2.blogbright.net

difference between steroids

References:

https://humphrey-cotton.thoughtlanes.net/

mgm grand sports betting online casino betmgm play mgmbets

are anabolic steroids addictive

References:

https://bookmarkzones.trade

quick gain reviews

References:

hyllested-carson.technetbloggers.de

Your point of view caught my eye and was very interesting. Thanks. I have a question for you. https://accounts.binance.com/ur/register?ref=SZSSS70P

how often to inject deca

References:

karayaz.ru

most effective bodybuilding supplements

References:

09vodostok.ru

mcluck AZ mcluckcasinogm mcluckontario

steroids with less side effects

References:

onlinevetjobs.com

test e steroid

References:

https://bom.so/zKIuaE

plant based steroids

References:

posteezy.com

winnie steroid

References:

https://sonnik.nalench.com/user/namedrama60

best muscle growth supplements 2015

References:

morphomics.science

bulking supplements bodybuilding

References:

graph.org

Known seeking its monster scheme library and explicit interface, best casinos is a premier sweepstakes casino that’s fully authorized in dozens of states. It combines free WOW Coins pro immeasurable compete with with Sweepstakes Coins that can rot into actual prizes.

where to buy winstrol online

References:

morphomics.science

alternative to steroids for bodybuilding

References:

elclasificadomx.com

bodybuilders on steroids

References:

frank-hermansen-2.technetbloggers.de

Diversify your life with bright wins. crowns coin casino ensures confidentiality and a quick start. Get your bonus right now!

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

The reels of Sweet Bonanza never sleep — tumbles lead to more tumbles, multipliers lead to fortunes. Free spins sweet bonanza bonus are the cherry on top. Get your sweet fix!

casino maryland

References:

atavi.com

super scratch programming adventure

References:

livebookmark.stream

online roulette australia

References:

http://test.gigga-grafics.de

red rock casino las vegas

References:

onlinevetjobs.com

las vegas casinos

References:

alushta-shirak.ru

best casino bonuses

References:

https://rentry.co

wheel of fortune slots

References:

https://vacuum24.ru

port perry casino

References:

atesoglusogutma.com

gaming casino

References:

mensvault.men

best online casino sites

References:

https://wikimapia.org/external_link?url=https://mrocasino.blackcoin.co

best online games

References:

yatirimciyiz.net

casino hobart

References:

https://atavi.com/share/xpqnkkz1q9n9g

pokies online

References:

mehmetnuriarslan.com

online slots uk

References:

dreevoo.com

casino monticello

References:

http://www.qazaqpen-club.kz/en/user/banktax25/

Wild West wins wait in buffalo territory. buffalo slot free spins brings stacked symbols, bonus storms, and jackpot gold. Get yours!

best lean physique

References:

http://www.instapaper.com

steroid effects on body

References:

firsturl.de

Chumba Casino: free to play, real prizes to win. Get your welcome chumba online casino instantly and start spinning the hottest titles. The good times start here!

casino palavas

References:

https://raskrussia.ru/blog/artem-galunin-lyzhnoe-dvoebore/

Trusted since 2017. Still the fastest. Still fire stampede stake the fairest. Still the best.

best muscle building supplements at gnc

References:

celebratebro.in

Step up to DraftKings table games Casino today. Play $5, receive 500 Cash Eruption spins + up to $1,000 lossback. The ultimate online casino experience!

anabolic steroids legal

References:

to-portal.com

list of side effects of steroids

References:

https://mapleprimes.com/

Neplatte za znacku, platte za zdravi. Uspora az 80 %

finasterid bez predpisu

Solder together the millions delightful colossal on fanduel casino South Dakota – the #1 real pelf casino app in America.

Reach your $1000 PLAY IT AGAIN hand-out and refashion every relate, хэнд and rolling into official cash rewards.

Fast payouts, whopping jackpots, and non-stop effect – download FanDuel Casino in these times and start playing like a pro today!

Rejoignez la rГ©volution Betano. Obtenez jusqu’Г 500 € de bonus plus des tours gratuits et jouez aux jeux les plus passionnants en ligne. Paris sportifs, casino en direct https://betanogame.org/fr/bonuses/ et jackpots infinis – c’est lГ que vous appartenez.

References:

Online roulette system

References:

https://ryu-ga-index.com:443/index.php?acostaiversen685307

References:

Casino vegas

References:

https://www.udrpsearch.com/user/selforgan0

References:

Casino launceston

References:

https://goalcycle7.werite.net/best-no-deposit-casino-bonus-codes-march-2026

The legislative landscape encompassing hemp-derived CBD https://www.cornbreadhemp.com/products/full-spectrum-cbd-gummies changed dramatically with the 2018 Farm Bill in the United States. Products containing less than 0.3 percent THC became federally legal, opening doors for consumers and businesses similarly. However, state regulations nonetheless vary, so reviewing local laws remains vital. This evolving framework continues to mold how people acquire and appreciate cannabidiol-based wellness products across the nation.

Mostbet – diversГЈo garantida e recompensas que vГЈo te surpreender – https://mostbetpt.pro/bonus/ , Mostbet – o cassino online feito para quem quer ganhar de verdade .

Play like the next spin already paid rent – https://aonlineplr.com , Ignite your luck — the fire is already burning .

References:

Instant Casino Auszahlungsdauer

References:

https://undrtone.com/monkeyjason3

References:

Instant Casino Spielanbieter

References:

https://www.marocbikhir.com/user/profile/636254

References:

Instant Casino Konto erstellen

References:

https://lostdogs.co.za/user/profile/dashsalt0

References:

Instant Casino App

References:

https://school-of-safety-russia.ru/user/fingermoat3/

References:

Instant Casino Auszahlungsdauer

References:

https://medibang.com/author/28050277/

References:

Instant Casino Login vergessen

References:

https://firsturl.de/3yQJDSe

References:

Instant Casino mobile spielen

References:

https://firsturl.de/jLGmc7V

References:

Female bodybuilding steroids pictures

References:

https://pad.stuve.de/s/1LkXDygRd

References:

Us online casinos

References:

https://pads.jeito.nl/s/nAQy96USZZ

References:

Ladbrokes casino

References:

https://hack.allmende.io/s/di6FI1iiF

References:

Instant Casino VIP Programm

References:

https://zenwriting.net/pocketlamb8/hol-dir-deinen-100-bonus-und-freispiele

References:

Jay cutler steroids cycle

References:

http://tropicana.maxlv.ru/user/creditgoal4/

References:

Instant Casino App iOS

References:

https://tvoyaskala.com/user/homesmash4/

References:

Pink floyd live in pompeii

References:

https://yogaasanas.science/wiki/WinSpirit_Casino_Review_Get_300_up_to_C400_100_FS

References:

Instant Casino Seriosität

References:

https://elearnportal.science/wiki/Instant_Casino_Bonus_2026_7500_Code

References:

Instant Casino Spiele

References:

https://carver-harbo-2.hubstack.net/200-casino-bonus-angebote-2026-komplette-liste

References:

Beste echtgeld casinos

References:

https://menwiki.men/wiki/Merkur_Slots_Test_Hol_dir_50_Bonus_im_SpielothekenKlassiker

References:

Positive effects of steroids

References:

https://uznove.uz/user/sleephelium39/

References:

How to stack tren and test

References:

https://www.searchmerajob.in/employer/buy-clenbuterol-solution-30ml

References:

How to gain muscle without steroids

References:

https://werkstraat.com/companies/where-to-buy-anavar-7-reliable-sources-for-2025/

References:

Re-built mass side effects

References:

https://lcateam.com/employer/legal-hgh-suppliers-for-pharmacies-verified-distributors-list/

References:

Bulk up pills

References:

https://guiacomercialsaopaulo.com/author/tamararobin/

References:

Best steroid supplement

References:

https://raindrop.io/banjomenu41/vancemcbride1591-66449469

Nous veillons sur vous avec expertise et bienveillance – https://www.pharmacieprovidencevifane.com/mentions-legales/ , Pharmacie attentive, efficace et proche de vos prГ©occupations .

References:

Best testosterone stack cycle

References:

https://pad.geolab.space/s/Wrn2A_2vP

References:

Buy dianabol pills

References:

https://pad.geolab.space/s/Hi8Fw09D0

References:

Gnc muscle building stacks

References:

https://matkafasi.com/user/baypatio6

References:

Legal steroids for muscle mass

References:

https://yogaasanas.science/wiki/Testosterone_Pills_Uses_Side_Effects

References:

Where are steroids made

References:

https://md.inno3.fr/s/lPKGLDCwn

References:

Which of the following is true about anabolic steroids?

References:

https://pediascape.science/wiki/The_Best_Testosterone_Boosters_of_2026_Tested

References:

How do steroids work to increase muscle growth

References:

https://historydb.date/wiki/Oxandrolon_Anavar_10_mg_100_tabs

References:

Anabolic steroids injection

References:

https://md.farafin.de/dWTvsThrQrq-XfLLydXRng/

References:

Steroids acne prevention

References:

https://pad.stuve.uni-ulm.de/s/OFgXnN6S8d

References:

Fast acting muscle building supplements

References:

http://karayaz.ru/user/danieldonkey8/

References:

Best liver support for dbol

References:

https://pattern-wiki.win/wiki/Quel_complment_alimentaire_choisir_pour_maigrir_guide_complet

References:

Steroid means

References:

https://md.swk-web.com/s/2aeJOMQy9

References:

Anabolic steroids dosage

References:

https://md.swk-web.com/s/cqpyXospL

References:

Best legal supplements for muscle gain

References:

https://urlscan.io/result/0198bcc4-1102-775f-94ee-c7f9aea0bed2/

References:

Echtgeld Casino Bonus ohne Einzahlung

References:

https://pads.jeito.nl/s/WZvDpP5Jzb

References:

Echtgeld Casino Testsieger

References:

https://pads.jeito.nl/s/Qu2aDXLPG_

References:

Is creatine steroids

References:

https://brewwiki.win/wiki/Post:Les_19_meilleurs_boosters_de_testostrone_pour_hommes_en_2026

References:

Online Casino Echtgeld legal

References:

https://rentry.co/6s9iokef

References:

Trenbolone for sale

References:

http://yogaasanas.science/index.php?title=Buy_Trenbolone_Online_Safely_Legally&action=submit

References:

Best gnc pre workout 2016

References:

https://timeoftheworld.date/wiki/Buy_Trenbolone_Online_Top_Suppliers

References:

Rocketplay neosurf deposit time

References:

http://karayaz.ru/user/fursort6/

References:

Clenbuterol wo kaufen

References:

http://okprint.kz/user/satincherry25/

References:

Legal testosterone supplements

References:

https://opensourcebridge.science/wiki/Sustanon_250_for_Enhanced_Muscle_Growth

References:

Testosteron insektion kaufen

References:

http://historydb.date/index.php?title=Testosteron_Online_Kaufen_Sichere_Bestellung&action=submit

Your article helped me a lot, is there any more related content? Thanks!

References:

Paradice casino

References:

https://500px.com/p/moodyjvfstallings

References:

Long term steroid side effects

References:

https://adamsen-walton-2.mdwrite.net/testosteron-kaufen-uberblick-and-leitfaden

References:

Rettenberg

References:

https://fivem-casino-scripts.online-spielhallen.de/

References:

Hard rock casino vancouver

References:

https://conti-casino.online-spielhallen.de/

References:

Saarbrücken

References:

https://krypto-casino.online-spielhallen.de/

References:

Dresden

References:

https://casino-rathaus-hannover-speiseplan.online-spielhallen.de/

References:

Lucky club casino

References:

https://graph.org/How-Old-Was-Daniel-Craig-In-Casino-04-27

References:

Entwickler

References:

https://git.123doit.com/vincewagoner1/4812874/wiki/Online-Casino-Testsieger-2025-Stiftung-Warentest

References:

Casino udbetalingsprocenter oversigt

References:

http://www.shkxrd.com:3000/teganchallis9

References:

Casinoer med ærlig udbetaling

References:

https://molchanovonews.ru/user/fielddew9/

References:

Bedste danske casinoer med høj RTP

References:

https://git.healthathome.com.np/ofeliaalice486

References:

Deuces wild video poker

References:

https://jobstak.jp/companies/best-payid-casino-in-australia-find-the-best-payid-casinos/

References:

Talking stick casino

References:

https://fairytalescreation.com/node/8605

References:

Real online casino

References:

https://unidemics.com/employer/ignition-casino-promo-codes-2026-get-300-bonus-up-to-3000/

References:

Nba games tonight

References:

https://academy.cid.asia/blog/index.php?entryid=93269

References:

Colosseum casino

References:

https://rentry.co/7903-50-free-spins-daily-bonus-access

References:

Plan du metro montreal

References:

https://spandexjobs.com/employer/live-games-at-candy96-real-dealer-casino/

References:

Casino lisboa macau

References:

https://icmimarlikdergisi.com/kariyer/companies/candy96-casino-australia-your-premier-gaming-destination-down-under/

References:

Mountaineer racetrack and casino

References:

https://lcateam.com/employer/official-site/

References:

Casino barriere toulouse

References:

https://amlsing.com/thread-730020-1-1.html

References:

Julian smith casino http://www.cruzenews.com/wp-content/plugins/zingiri-forum/mybb/member.php?action=profile&uid=2324664

Your article helped me a lot, is there any more related content? Thanks!

References:

Mahnomen casino https://iraqitube.com/@mindy525562825?page=about

References:

Casino real estate https://git.bp-web.app/darrinswanson

Your article helped me a lot, is there any more related content? Thanks! https://accounts.binance.com/register/person?ref=MBLCVVZG

Your point of view caught my eye and was very interesting. Thanks. I have a question for you. https://accounts.binance.info/kz/register?ref=K8NFKJBQ

References:

Craps online practice https://ancientroman.space/wiki/HitnSpin_Deutschland_Spiele_und_295_Willkommensbonus

References:

Cleopatra slot https://www.24propertyinspain.com/user/profile/1453485/user/profile/1453485

References:

Blackjack surrender https://bandori.party/user/1031561/scenetin0/

References:

Genting casino stoke https://coolpot.stream/story.php?title=hitnspin-bonus-ohne-einzahlung-fuer-50-freispiele

References:

Nodepositbonus cc https://bookmarks4.men/story.php?title=hitnspin-casino-erfahrungen-2026-serioeser-curacao-anbieter

References:

Silversands casino https://dreevoo.com/profile.php?pid=1723666

References:

Grand portage lodge and casino https://commonwiki.space/wiki/HitnSpinSupportBewertung_Qualitt_des_Kundenservice_und_Reaktionszeit

References:

Vancouver casinos https://doc.adminforge.de/s/SnMkqJFqsc

References:

Instant Casino Willkommensbonus

References:

https://pbase.com/gloveauthor59/

References:

Instant Casino Spielanbieter

References:

https://boardgameswiki.site/wiki/Aktuelle_Sofortboni_Freispiele

References:

Roulette online game https://chesswiki.site/wiki/Vulkan_Vegas_Casino_Slots_Live_Casino_Bonus

References:

Boogie nights hollywood casino https://actualites.cava.tn/user/checkkevin8/

References:

Mardi gras casino https://chesswiki.site/wiki/Total_Casino_Registrierung_und_Willkommensbonus

References:

Seminole casino https://bookmarking.win/story.php?title=drip-casino-app-all-in-one-mobile-gaming-plattform

References:

La roulette https://bendsen-hein.federatedjournals.com/online-casino-mit-exklusiven-boni-and-5000-spielen

References:

Casino austria https://pad.stuve.de/s/5JYp0B2Zp

References:

Aladdin las vegas https://russell-lindholm.technetbloggers.de/alle-aktuell-boni-und-promo-codes

References:

Playboy casino https://castro-horne-2.mdwrite.net/nv-casino-erfahrungen-2025-sicher-oder-ein-betrug

References:

Casino winners https://nomadwiki.space/wiki/1Go_Casino_50_Freispiele_ohne_Einzahlung_Mai_2026

References:

Download slot machine games https://ancientroman.space/wiki/ICE_Casino_Bonus_Code_2026_270_Freispiele_geschenkt

References:

Gulfport casinos https://a-taxi.com.ua/user/paulpen6/

References:

Download slot machine games https://socialbookmark.stream/story.php?title=sofort-registrieren-mega-bonus

References:

Gulfport casino https://pad.stuve.de/s/hOaGSCcO5

References:

Online vegas casino https://bridgedesign.space/wiki/ICE_Casino_Bonus_Code_2026_270_Freispiele_geschenkt

References:

Indian head casino https://school-of-safety-russia.ru/user/avenuejuly4/

References:

Hollywood casino joliet il https://materialwiki.site/wiki/NV_Casino_Official_Site_Bonus_bis_zu_2_000_225_Freispiele

References:

Sands casino bethlehem https://hackmd.okfn.de/s/BJXUuFmxfe

References:

Suncoast casino durban https://justbookmark.win/story.php?title=bericht-ueber-1go-casino-boni-spielen-zahlungsmethoden

References:

St croix casino danbury http://amur.1gb.ua/user/atticperson51//user/atticperson51/

References:

Treasure island casino mn https://skitterphoto.com/photographers/2801309/sherwood-reeves

References:

Instant Casino mit Trustly

References:

http://uchkombinat.com.ua/user/beechroad3/

References:

Cramps in feet https://eggswiki.site/wiki/888_Casino_Erfahrung_Betrug_Abzocke_8_1_Kundenbewertung

References:

Baton rouge casino https://https://bridgedesign.site/wiki/Casino_Reload_Bonus_Tipps_Top_Anbieter_2026/wiki/Casino_Reload_Bonus_Tipps_Top_Anbieter_2026

References:

Online casino mac https://peatix.com/user/29720869/view/user/29720869/view

References:

Igt slots https://https://livebookmark.stream/story.php?title=kings-casino-rozvadov-poker-turniere-2026-alle-infos/story.php?title=kings-casino-rozvadov-poker-turniere-2026-alle-infos

References:

Puerto rico casinos https://pad.stuve.uni-ulm.de/s/jV6vMSLeD/s/jV6vMSLeD

References:

Rules for blackjack https://school-of-safety-russia.ru/user/bluedelete4/

References:

First council casino http://ezproxy.cityu.edu.hk/login?url=https://de.trustpilot.com/review/mydogoutfitters.de

References:

Play casino games https://https://nutritionwiki.space/wiki/Betano_Zahlungsmethoden_Ein_und_Auszahlungen/wiki/Betano_Zahlungsmethoden_Ein_und_Auszahlungen

References:

Slotmachines https://telegra.ph/Neue-Online-Casinos-Juni-2026-06-07

References:

Casino soundtrack http://amur.1gb.ua/user/squidflute2/

References:

Seven cedars casino https://https://www.udrpsearch.com/user/geesejelly1/user/geesejelly1

References:

Casino australia https://pad.stuve.uni-ulm.de/s/4qIG4H1oO/s/4qIG4H1oO

References:

Slot machine manufacturers https://rentry.co/9u2fxz3t

References:

Horizon casino https://https://md.swk-web.com/s/EzQ00NJuM/s/EzQ00NJuM

References:

Online casino games https://https://boardgameswiki.site/wiki/Monro_Casino_Test_Erfahrungen_Bonus_und_Bewertung_2025/wiki/Monro_Casino_Test_Erfahrungen_Bonus_und_Bewertung_2025

References:

Casino cleveland https://https://bowden-cooley-2.federatedjournals.com/vulkan-vegas-bonus-code-2025-alle-vulkanvegas-promo-codes-and-aktionscode-bestandskunden/vulkan-vegas-bonus-code-2025-alle-vulkanvegas-promo-codes-and-aktionscode-bestandskunden

References:

Mohawk casino https://xypid.win/story.php?title=top-slots-spannende-live-spiele/story.php?title=top-slots-spannende-live-spiele

References:

Choctaw pines casino https://https://freudwiki.site/wiki/Bonus_App_Sportwetten_Zahlungen_Legalitt/wiki/Bonus_App_Sportwetten_Zahlungen_Legalitt

References:

Operation blackjack https://https://neolatinswiki.site/wiki/Volle_Kontrolle_ber_das_Gaming_auf_deinem_Mobilgert/wiki/Volle_Kontrolle_ber_das_Gaming_auf_deinem_Mobilgert

References:

Casino jackpot https://https://bridgedesign.space/wiki/Official_Online_Casino_with_Welcome_Bonus_Free_Spins/wiki/Official_Online_Casino_with_Welcome_Bonus_Free_Spins

References:

Capitol casino https://www.https://www.investagrams.com/Profile/bray4273133/Profile/bray4273133

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me? https://www.binance.bh/register?ref=QCGZMHR6

References:

Casino cherokee nc https://socialtechnet.com/story7141755/casino-of-gold-ihr-weg-zum-jackpot

References:

Olympic casino poker https://meshbookmarks.com/story21654633/casino-of-gold-ihr-weg-zum-jackpot

References:

%random_anchor_text% https://bookmarkdaily.space/item/bonus-800-200-freispiele

References:

%random_anchor_text% https://zenwriting.net/energyoyster12/der-hitnspin-willkommensbonus-alle-infos

References:

%random_anchor_text% http://downarchive.org/user/packetrouter48/

References:

%random_anchor_text% https://undrtone.com/swordradish0

References:

Online casino sites https://bookmarkfame.com/story21400751/casino-of-gold-ihr-weg-zum-jackpot

References:

Seminole casino immokalee https://socialbraintech.com/story6562099/casino-of-gold-ihr-weg-zum-jackpot

References:

%random_anchor_text% https://www.orkhonschool.edu.mn/profile/krebsgcudempsey98863/profile

References:

%random_anchor_text% https://xn--41-4lcpj.xn--j1amh/user/breakformat27/

References:

Merkur online casino https://date.ainfinity.com.br/@beulahshuler88

References:

Playboy casino cancun https://financevideosmedia.com/@norrisoquendo?page=about

References:

Online casino slot machines https://sostinestauras.lt/events/lietuvos-rankinio-u-19-vaikinu-cempionatas/

References:

Thunderstruck drinking game https://aptfindcriminal.com/about-us/

References:

Maryland casino live https://spinvai.com/wvclogan063753

References:

Buzzluck casino https://adufoshi.com/josefinawilshi

References:

Legiano Casino Spielen https://telegra.ph/100–bis-zu-500–200-Freispiele-06-07

References:

Legiano Casino Betrug https://pad.stuve.uni-ulm.de/s/60cDgpMs0

References:

Legiano Casino Mindestauszahlung https://frantzen-wright.technetbloggers.de/legiano-casino-offizielle-website

References:

Legiano Casino Video Review https://doc.adminforge.de/s/Zv9dgayost

References:

Legiano Casino Auszahlung Dauer https://xonnon.com/@jzsvivian8985?page=about

References:

Legiano Casino Jackpot https://yours-tube.com/@belltulloch167?page=about

References:

Legiano Casino Paysafecard https://kaymanuell.com/@daniloanglin87?page=about

References:

Legiano Casino Auszahlungsdauer https://tiktub.com/@britneygoldsch?page=about

References:

Legiano Casino Cashback https://www.divinagracia.edu.ec/profile/holmdakengel52805/profile

References:

Legiano Casino Anmelden https://www.rosewood.edu.na/profile/hicksvmdtroelsen51362/profile

References:

Legiano Casino Gutscheincode http://krug-shar.ru/bitrix/redirect.php?event1=&event2=&event3=&goto=https://de.trustpilot.com/review/owowear.de

References:

Legiano Casino Promo Code https://www.gta.ru/redirect/de.trustpilot.com%2Freview%2Fowowear.de/

References:

Legiano Casino Umsatzbedingungen https://us.grepolis.com/start/redirect?url=https%3A%2F%2Fde.trustpilot.com/review/owowear.de

References:

Legiano Casino Registrierung https://www.saltedge.com/exit?url=https%3A%2F%2Fde.trustpilot.com%2Freview%2Fdeincorazon.de