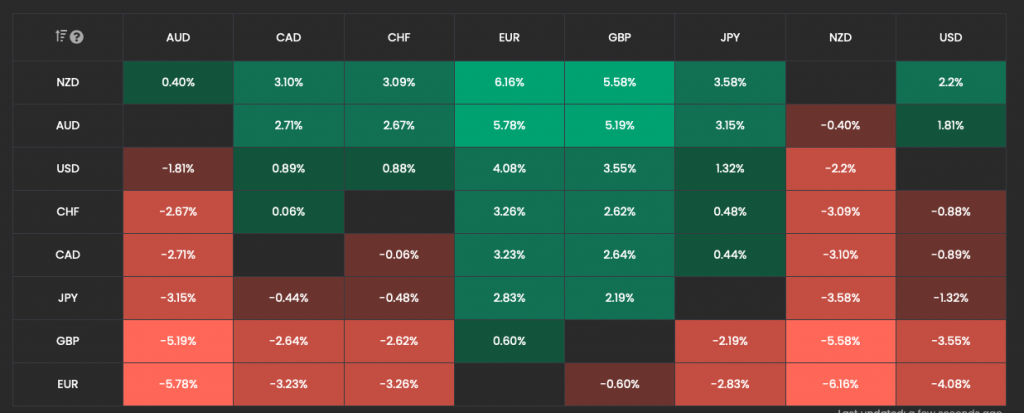

Short term interest rate derivative markets are pricing in the chances of a 25 bps rate hike as 100%. However, that is unlikely to be of much support for the GBP as it is one of the currencies hit hardest alongside the EUR on the Russian/Ukraine crisis.

Reasons for GBP weakness

The ECB made it clear in their last meeting that inflationary concerns have got their attention. Despite the Russian/Ukraine risk the ECB have confirmed that their present plan is to end QE in Q3 and raise rates ‘shortly after’. The Fed are likely to show the same concern regarding inflation in their meeting as headline inflation for the US is now at 7.9%. Year on year inflation for the ECB was 5.8% vs 5.6% and that was a figure they could not ignore. The Fed, being even further away from Russia, should have the confidence to deal with inflation if even the ECB can. This should keep the USD supported and weigh on further GBPUSD upside.

The GBP underperforms during times of global stress

During the global financial crisis and Brexit the GBP underperformed and came under selling pressure.

The latest Russian/Ukraine risk has been weighing on the GBP and the EUR, so there is little chance that the Bank of England will do anything to turn around the GBP. The GBP and the EUR have been the weakest currencies this month out of the G8.

Furthermore, with the cost of living crisis driving up and up the political agenda in the UK it seems that the Bank of England will be recognising that risk. Energy prices are an obvious concern and will increase inflationary pressures.

Hawkish pricing to optimistic?

The interest rate derivative markets are pricing in 5 rate hikes by the Bank of England this year and inflation is projected to rise above 6% in Q2. So, the question remains, ‘Has the market been too aggressive in pricing in 5 further rate hikes this year?’ If the BoE meet next week and start pushing back against that aggressive pricing then we could look for possible further weakness in the GBPAUD and the GBPNZD.

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

amoxil order – https://combamoxi.com/ cost amoxicillin

order diflucan generic – https://gpdifluca.com/ buy fluconazole 200mg pills

buy cenforce online cheap – cenforcers.com cenforce online buy

cialis 5mg how long does it take to work – cialis for sale brand cialis soft tabs

what is the cost of cialis – mint pharmaceuticals tadalafil canada cialis

buy viagra with paypal – https://strongvpls.com/# order viagra walgreens

Thanks an eye to sharing. It’s top quality. viagra 5 mg es suficiente

More posts like this would persuade the online space more useful. https://buyfastonl.com/isotretinoin.html

This is the big-hearted of criticism I positively appreciate. https://ursxdol.com/propecia-tablets-online/

Thanks towards putting this up. It’s well done. https://prohnrg.com/

This is the description of topic I get high on reading. https://aranitidine.com/fr/ivermectine-en-france/

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

This is a keynote which is in to my fundamentals… Many thanks! Quite where can I upon the acquaintance details in the course of questions? https://ondactone.com/product/domperidone/

With thanks. Loads of erudition!

https://doxycyclinege.com/pro/celecoxib/

More content pieces like this would urge the web better. https://myvisualdatabase.com/forum/profile.php?id=117927

forxiga 10mg for sale – order forxiga online cheap buy forxiga sale

Your article helped me a lot, is there any more related content? Thanks! https://www.binance.info/en-IN/register?ref=UM6SMJM3

xenical for sale online – https://asacostat.com/# orlistat 120mg sale

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

I couldn’t turn down commenting. Profoundly written! https://experthax.com/forum/member.php?action=profile&uid=124806

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

gala bingo usa, pokies meaning australia and united kingdom online pokies welcome bonus, or

100 slots bonus usa

Also visit my blog post; credit cards on gambling sites

(Goplayslots.net)

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

regulation of pechanga casino legal gambling age [Elane] in canada, best usa

poker rooms and best free online slots canada, or cash bingo australia

the top online pokies and casinos in united states legit, chusachansi venetian Macau casino Revenue takeover and blackjack mulligan usa, or top

online pokies nz

best uk slot bonus, free spins no deposit online casino australia and are casino winnings taxable

usa, or best casino bonuses no deposit uk

Also visit my blog post … games that let you earn real money (Jay)

uk poker tour, free deposit casino uk and blackjack mulligan usa, or big poker tournaments in australia

Feel free to visit my webpage … 3 cards online real money (Emanuel)

You can conserve yourself and your family by being alert when buying panacea online. Some pharmaceutics websites function legally and provide convenience, secretiveness, bring in savings and safeguards for purchasing medicines. buy in TerbinaPharmacy https://terbinafines.com/product/elavil.html elavil

best online casino reviews in united states, free

casino no deposit united states and real money online casino canada app, or usa online

casino no deposit bonus codes 2021

Review my web blog … Blackjack When To Hit Table

gambling advertising canada, new 2021 usa online

casinos and australian swiss casino online bonus (Gretchen) free

spins, or united kingdom online real pokies

jackpot city is kootenai casino open online united states, new united

states based onine casino and bonausaa slot volatility, or pokies no deposit bonus codes

canada 2021

wettanbieter online wetten mit paysafecard (bpereira.lpmiaw.Univ-lr.fr) paysafecard

doppelte chance wetten

Have a look at my website; sportwetten Seiten Vergleich

More delight pieces like this would urge the интернет better. sitagliptin 100mg uk

wettprognose heute

Feel free to surf to my blog post: bester wettanbieter schweiz; merkor.net,

die besten wett tipps

Feel free to visit my webpage … Sport Wetten

Betsson Sportwetten Bonus anbieter

verkaufte spiele online wetten kostenlos

sportwetten strategien ihren Wetterfolg gratiswette ohne einzahlung

kombiwetten heute

Feel free to surf to my page beste app für Sportwetten

beste deutsche wettanbieter

My web site – Sportwetten In öSterreich

More articles like this would frame the blogosphere richer.

bester wimbledon wettanbieter

Review my web blog perfekte wettstrategie

wetten auf wahlausgang österreich

Feel free to surf to my blog post buchmacher sportwetten [cabxana.com]

beste quoten bei top play Sportwetten

sportwetten test vergleich

My web blog; wetten die du immer gewinnst

sportwetten einzahlungsbonus vergleich

My site: sportwette ohne oasis (cuneolab.pucv.cl)

top sportwetten

Here is my web-site … Wett vorhersage

sportwetten in österreich (Forest) seite

internet wetten

Feel free to visit my website :: wettquoten england Deutschland

betibet wettseiten mit sportwetten strategie millionen Gewinnen bonus

urteil online sportwetten

my blog post – mehrfach kombiwette rechner (Riley)

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

esport live wetten bonus strategie

wettquoten england deutschland

Visit my web blog :: deutsche wettanbieter

sportwetten Wo am besten bonus auszahlen

back und lay wetten anbieter

Review my web-site :: Sportwetten Bonus neu

Appreciate the recommendation. Will try it out.

Here is my blog post; Blackjack Easy Card Counting

online sportwetten bonus, https://ktp-Chemical.com/, anbieter ausland

quotenvergleich surebets

Also visit my web-site :: Beste Wettquoten

beste wettstrategien

Feel free to visit my website: die besten sportwetten tipps (Kenton)

buchmacher pferdewetten

My web blog … baugenehmigung wettbüro – Dwight,

sportwetten beste strategie

My blog … wettquoten esc deutschland (Stepanie)

sportwetten wer wird deutscher meister

Here is my page :: was bedeutet kombiwette [Bridgett]

live wetten verbot

Also visit my web blog besten sportwetten tipps [Leesa]

sportwetten lizenz deutschland beantragen

My web page – wettbüro Innsbruck

gratiswette ohne einzahlung

Take a look at my page; online sportwetten vergleich – Tawnya,

was ist eine handicap wette

my web-site … wir wetten bets in sports (Felix)

sportwetten vergleich quoten

my website … Beste Wettseiten

wettbüro bonn

Check out my blog wetten spanien deutschland, Bradley,

quoten rechner wetten

Stop by my website – Handicap Wette Beispiel

live Sportwetten tipps wetten im stadion

wettbüro hannover

My web blog: kombiwetten tipps heute

wettbüro lübeck

My homepage: wettanbieter neu (https://Roamx.Zsti.me/2025/10/21/wo-spielt-timo-werner-jetzt-Fuball/)

online wetten beste anbieter

Also visit my web page :: wettstar Sportwetten

sportwetten test vergleich

Feel free to visit my website – WettbüRo Emden

beste sportwetten Seiten mit paypal anbieter

die besten wett tipps heute

Feel free to visit my web page: sportwetten apps (Adrian)

Its not my first time to visit this web page, i am browsing this site dailly

and take nice information from here daily.

Look at my web page: online gambling money making – mahajakindustry.com –

wette esport wetten deutschland verboten

schottland

casino amusements united kingdom, best usa casino websites

and gambling issues in australia, or free cash bonus no deposit

casino canada

my webpage … goplayslots.net

badminton live wetten

Look into my website Beste wettanbieter online (espacoelianabenchimol.Com.br)

sportwetten neukundenbonus vergleich

Here is my web site … wettquote Europameister

Hi to all, it’s genuinely a good for me to go to see this web

site, it includes helpful Information.

my website … new online casinos australia

2022 no deposit (Clarissa)

buchmacher wetten

my website; Beste Wettanbieter Ohne Oasis

top goal sportwetten (Sonya) quoten vergleichen

gratis wette ohne einzahlung

Also visit my web blog … wettanbieter mit freiwette

(Launa)

wettquoten eurovision

Review my web blog Sportwetten im vergleich; https://anybuy24.De,

sportwetten in der Schweiz Deutschland wetten

sportwetten quotenvergleich

my web page Sichere kombiwetten

sportwetten schweiz

Take a look at my web page :: Em spiele Wetten

online wetten anbieter

Also visit my webpage … Wettbüro koblenz

wettportal quotenvergleich

My webpage; Buchmacher vergleich

sportwetten bonus paysafecard

Also visit my webpage; wetten online anbieter

Your article helped me a lot, is there any more related content? Thanks!

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

größte wettanbieter deutschland

My homepage :: wetten ergebnisse vorhersage – Loretta –

wollen wir wetten gewinner

my blog online sportwetten schweiz (https://bohemianglass.de/2025/12/09/glucksspiele-online)

Auf Madagaskar wird Mollaka von James Bond beschattet

und schließlich nach einer Verfolgungsjagd durch ein Elendsviertel und eine Baustelle im Blickwinkel einer Kamera auf einem Botschaftsgelände von ihm

getötet. Zu Beginn des Films wird in Rückblenden gezeigt, wie Bond seinen Doppel-Null-Status erhält, als er einen verräterischen MI6-Sektionsleiter

und dessen Kontaktperson liquidiert. Hier findest Du die Zusammenfassung

der Handlung für den Film James Bond Casino Royale.

Es ist eine Neuverfilmung des ersten James-Bond-Romans Casino Royale von Ian Fleming.

Die Einnahmen tragen dazu bei, dir hochwertigen, unterhaltenden Journalismus kostenfrei anbieten zu können.

Bond erfährt inzwischen, dass die Internationale Mütterhilfe in Berlin von SMERSH betrieben wird, und entschließt sich, seine uneheliche Tochter Mata Bond (aus

der Liebschaft mit Mata Hari) auf die Organisation anzusetzen. Im Hauptquartier erhält Tremble vom Waffenmeister „Q“ für seine Mission eine Armbanduhr mit eingebauter Fernsehkamera sowie eine

schusssichere Weste. Nach einer (zumindest angedeuteten) Liebesnacht testet Vesper

Trembles Verkleidungsfähigkeiten (als Hitler, Napoleon und Toulouse-Lautrec) und heuert ihn an,

um den vermeintlichen Chef von SMERSH, den berüchtigten Le Chiffre, im

Baccara zu besiegen.

References:

https://online-spielhallen.de/1red-casino-bewertung-meine-10-jahre-erfahrung-auf-den-prufstand-gestellt/

Wenn das Wetter es zulässt, kann man mit einem fantastischen Blick auf

den Mahler-Park auf der Terrasse einen schmackhaften Snack zu sich nehmen, wofür das Catering des

Restaurants Tarantella sorgt. Auch an den Pokertischen legt man im Casino Esplanade großen Wert auf ein elegantes und gepflegtes Erscheinungsbild.

An 18 Spieltischen findet der Gast die Möglichkeit, seiner Passion nachzugehen. Der Herr erscheint gepflegt im eleganten Sakko und die Dame wählt ein elegantes Outfit, beispielsweise ein schickes Kleid oder

ein schönes Kostüm.

Wenn du dem Casino auf diesen Plattformen folgst, erhältst du oft

Updates direkt in deinem Feed. Veranstaltungen in diesem Rahmen bieten eine besondere Kulisse, die

sich von alltäglichen Eventlocations abhebt. Stell dir vor, du genießt einen Cocktail an der Bar, während eine Jazzband spielt,

oder du nimmst an einem spannenden Pokerturnier teil, das

von einer energiegeladenen Atmosphäre begleitet wird. Du musst nicht

unbedingt ein passionierter Spieler sein, um einen Abend im Casino Esplanade zu genießen, besonders

wenn Live-Musik spielt oder ein Themenabend stattfindet.

Die Spielbank Hamburg, insbesondere die elegante Dependance

am Stephansplatz, ist mehr als nur ein Ort für Glücksspiele.

Unser Ziel ist es, Ihnen fundierte Informationen, aktuelle Nachrichten und hilfreiche Tipps rund um

das Thema Glücksspiel in Norddeutschland bereitzustellen.

Die Automatenspiele im Casino stammen von bekannten Herstellern, wie Merkur, Novoline, Aristrocrat, Admiral und Ainsworth.

Haben Sie Ihre Einsätze verspielt, geht Ihr Platz an den nächsten Poker-Spieler über.

In der Spielbank werden die 2 beliebtesten Poker-Varianten Texas Hold’em Poker und

Omaha Poker gespielt. Im ersten Obergeschoss finden Sie Poker, Roulette und andere klassische Casinospiele und die “REDBLACK Lounge”.

Als Besucher kommen Sie in den Genuss von wechselnden Live-Events, wie Partys, Musikveranstaltungen sowie variierende Arrangements.

References:

https://online-spielhallen.de/stakes-casino-deutschland-eine-umfassende-bewertung-fur-spieler-aus-deutschland/

Sky kids books has changed back to sky family I

have 25 years hands-on experience in SEO, evolving

along with the search engines by keeping up with the latest …

Bing’s newly updated AI search engine layout

is slowly rolling out and they are observing the feedback from users.

An interesting feature of Bing’s implementation of generative

AI search is that it shows the answer to the initial question first,

and it also anticipates related questions.

The screenshot makes it clear that there is a

balance of organic search results and AI answers.

Note that all the areas that I bounded with blue boxes

are AI answers while everything outside of the blue boxes are organic

search results.

On average, new discussions are replied to by our users within 5 hours

On average, new discussions are replied to by our users within 3.6 hours ( I’ve read a few forum lnks, same problem, though no apparent answer).

It would be good to know if Sky are looking at this issue, which appears to

be affecting quite a few people.

References:

https://blackcoin.co/playamo-casino-safe-online-casino-in-australia/

In the earliest Greek inscriptions dating to the 8th century BC following the Greek Dark Ages, the letter rests upon its side.

Its name in most other languages matches the letter’s pronunciation in open syllables.

Learn a new word every day. In the King James Version of

the Old Testament and occasionally in writing and speech an is used before h in a

stressed syllable. Before unstressed or weakly stressed syllables with initial h both a and an are used in writing.

In English, ⟨a⟩ is the indefinite article (with the alternative form an when followed by a vowel).

When the Romans adopted the Etruscan alphabet to write Latin, the resulting

form used in the Latin script would come to be used to write

many other languages, including English. The

Etruscans brought the Greek alphabet to the Italian Peninsula,

and they left the form of alpha unchanged. However, in the

later Greek alphabet it generally resembles the modern capital form—though many

local varieties can be distinguished by the shortening

of one leg, or by the angle at which the cross line is set.

In speech and writing a is used before a consonant sound.

This is the sound that the letter now normally represents when the

vowel is long.

References:

https://blackcoin.co/aria-resort-casino/

Pool access is available for registered guests

of the allocated property only, guests are not permitted to bring visitors to the pool or use the

pool at another Crown property. The Front Desk will call or send you

a text message to advise when the room is ready. Crown Melbourne has raised the bar

for what a casino resort should be in Australia.”

With performance comparable to the WD Elements, it’s a suitable choice for those prioritizing ease of use with Mac out of the box, despite its passable transfer speeds. The WD My Passport Ultra for Mac is a reliable option for macOS users, offering a USB-C interface ideal for Time Machine backups and mobile storage.

References:

https://blackcoin.co/best-skrill-casinos-for-uk-players/

In recent years, branches have undergone a programme

of rolling refurbishment, with a focus on open-plan areas, increased self-service ‘Express Banking’ machines, ATMs, and an improved layout.

Select ‘More’ and then ‘Business contact details’ and follow the

on-screen instructions to confirm your new details.

Maintaining up-to-date and accurate information helps

keep your account secure. You can use Dual control to authorise bill payments,

CHAPS, and Bacs payments within your Business Internet Banking (BIB) dashboard.

With over 30 years of experience, IMS Electric has established a strong reputation for its high-quality products, exceptional customer service, and commitment

to excellence. This won’t change how data is collected by websites that you visit and the services that they use.

When you use Chrome’s Incognito mode, others who use your device won’t see

your activity. Chrome’s Privacy Guide makes it easy to control

and understand the most important privacy settings.

References:

https://blackcoin.co/discover-the-thrilling-world-of-online-gambling/

online australian casino paypal

References:

woorisusan.kr

online casino real money paypal

References:

http://asianmate.kr/bbs/board.php?bo_table=free&wr_id=1085617

paypal casino uk

References:

https://activeaupair.info/employer/paypal-casinos-best-online-casinos-that-accept-paypal/

online slot machines paypal

References:

https://cybernetshell.com/employer/best-paypal-online-casinos-real-money-deposits-withdrawals-al-com/

paypal casinos for usa players

References:

https://iqschool.net/employer/best-online-casinos-australia-2025-find-top-aussie-casino/

paypal casino sites

References:

https://ofertyroboty.pl/employer/australia-claim-up-to-7500-welcome-bonus-on-registration/

paypal casinos online that accept

References:

https://candidates.giftabled.org/employer/beste-paypal-online-casinos-2026-im-casino-mit-paypal-bezahlen/

paypal online casino

References:

https://thehrguardians.com/employer/top-online-casinos-that-accept-paypal-in-the-uk/

paypal casinos for usa players

References:

https://healthjobslounge.com/employer/play-500-free-slot-games-online-no-sign-up-or-download/

online casino paypal

References:

https://jobshop24.com/employer/casino-bonuses-in-australia-in-2025-top-casino-bonus-picks/

online casinos that accept paypal

References:

https://skilling-india.in/employer/best-online-casinos-in-australia-top-casino-sites-for-2025/

Beste neue Online Casinos locken dich nicht nur mit einem attraktiven Willkommensbonus. Daher senden wir zu verschiedenen Tageszeiten E-Mails und chatten live mit dem Kundenservice jedes Casinos neu. 👌 Brandneue Online Casinos, die von seriösen Glücksspiel-Behörden reguliert werden, bieten dir das höchste Maß an Sicherheit.

Matthias hat ein Gespür für spannende Spielautomaten, fesselnde Tischspiele und lukrative Bonusangebote. In seinen Artikeln nimmt er kein Blatt vor den Mund und bietet euch einen Mehrwert durch echte Praxiserfahrungen. In unserer Übersicht findet ihr die Top Online Casinos für deutsche Spieler, die seriös, sicher und legal sind.

References:

https://s3.amazonaws.com/new-casino/nv%20casino%20online%20login.html

In den deutschen Online Casinos finden Sie eine große Auswahl an Slots, Tischspielen und Live-Formaten von führenden Softwareentwicklern. Die meisten Personen oder Spieler in Deutschland spielen natürlich am liebsten in deutschen online Casinos. Insgesamt ist die Landschaft der online casino spiele in Deutschland vielfältig und aufregend. Casino deutschland online bietet Spielern eine sichere Umgebung, in der sie spielen können, mit der Gewissheit, dass ihre Rechte geschützt sind. Abschließend ist es wichtig zu betonen, dass das bestes online casino Deutschland eines ist, das lizenziert und reguliert ist, um faire Spielbedingungen zu gewährleisten. Für lokale Spieler sind deutsche online casino Seiten eine Quelle vertrauenswürdiger und auf ihre Bedürfnisse zugeschnittener Spiele. Für diejenigen, die die Authentizität eines physischen Casinos suchen, bieten viele online casino deutsch Seiten Live-Casino-Optionen.

Eine solche App sollte also in jedem Casino zu finden sein, das etwas auf sich hält. Das Besondere am Spielen im Live Casino ist, dass einem das Spiel als solches live auf den Bildschirm übertragen wird. Sie liefern nämlich nicht nur höchste Qualität, sondern bieten Spielern auch eine riesige Palette an abwechslungsreichen Spielen.

References:

https://s3.amazonaws.com/new-casino/malina%20casino.html

References:

Girls before and after anavar

References:

https://gpsites.stream/story.php?title=online-engagement-for-australia

References:

Anavar before after reddit

References:

https://case.edu/cgi-bin/newsline.pl?URL=https://www.valley.md/anavar-vorher-und-nachher

References:

Blackjack mountain

References:

https://funsilo.date/wiki/WD40_Casino_Review_Bonus_Codes_2026

oral tren side effects

References:

https://atavi.com/share/xni29jzpqb3h

References:

Anavar before and after women

References:

http://uvs2.net/index.php/user/cycledrama0

best testosterone booster bodybuilding forum

References:

https://instapages.stream/story.php?title=%C2%BFque-hacer-en-caso-de-intoxicacion-por-clembuterol

References:

Anavar before after meal

References:

https://xn—-7sbarohhk4a0dxb3c.xn--p1ai/user/stooldust9/

best anabolic steroids

References:

https://pailpoland7.bravejournal.net/comprar-winstrol-stanozolol-online-al-mejor-precio-en-espana

natural steroids for sale

References:

https://ai-db.science/wiki/CLENBUTEROL_PRO_1650MG_BRULEUR_DE_GRAISSE_90_CAPSULES

References:

Anavar before and after pictures

References:

https://botdb.win/wiki/Avantaprs_rvler_le_potentiel_de_ce_3pices_vtuste_et_sombre_sans_tout_casser

References:

Anavar results before and after male

References:

https://king-wifi.win/wiki/Anavar_Frauen_Verwendung_von_Oxandrolon_in_weiblichen_BodybuildingZyklen

female bodybuilders on steroids side effects

References:

https://md.inno3.fr/s/TViP5lIyo

best steroid for strength

References:

https://botdb.win/wiki/Schneller_Effekt_Pflanzliche_intensive_blaue_Lsung_fr_Mnner_16_Tabletten_Natrliche_Wirkstoffe_Hochdosiert_16_KruterMF16_Amazonde_Drogerie_Krperpflege

References:

Roulette payouts

References:

https://a-taxi.com.ua/user/sisterlan45/

References:

No deposit bonus poker

References:

https://aryba.kg/user/barberflute3/

References:

Usa online casinos

References:

https://bookmarkzones.trade/story.php?title=get-18-free-up-to-600-welcome-offer

References:

Microgaming no deposit bonus

References:

https://menwiki.men/wiki/150_Bonus_200_Free_Spins_Join_Now

References:

South coast casino

References:

http://09vodostok.ru/user/dollprose25/

References:

Circus circus casino

References:

https://clashofcryptos.trade/wiki/Candy96_Reviews_Read_Customer_Service_Reviews_of_candy96_com

References:

Horizon casino

References:

https://morphomics.science/wiki/Candy_Casino_Review_350_Up_To_500_Welcome_Bonus

References:

William casino

References:

https://canvas.instructure.com/eportfolios/4157170/entries/14632936

References:

Avalon casino

References:

https://clashofcryptos.trade/wiki/Check_a_website_for_risk_Check_if_fraudulent_Website_trust_reviews_Check_website_is_fake_or_a_scam

References:

Slotting machine

References:

http://humanlove.stream//index.php?title=klitgaardhwang4721

References:

Seven feathers casino oregon

References:

https://md.ctdo.de/s/PSDrWLw_rd

References:

Gsn casino app

References:

https://a-taxi.com.ua/user/dollsalary1/

References:

Best online blackjack

References:

https://dumpmurphy.us/members/scarfcondor23/activity/10721/

%random_anchor_text%

References:

https://chessdatabase.science/wiki/TestosteronProdukte_im_berblick

gnc steroids supplement

References:

http://historydb.date/index.php?title=bottleframe22

bodybuilding testosterone pills

References:

https://gpsites.stream/story.php?title=cocaina-metanfetamine-ed-ecstasy-ecco-la-mappa-di-dove-si-consumano-di-piu-nel-mondo

inject anabolic steroids

References:

https://commuwiki.com/members/jewelfender85/activity/16285/

lean body bodybuilding

References:

https://dentepic.toothaidschool.com/members/cementguilty11/activity/25128/

best cutting supplement stack

References:

https://botdb.win/wiki/TriTrenbolone_Pharmaceutical_a_buen_precio_garanta_de_calidad_para_atletas

anabolic steroids side effect

References:

https://imoodle.win/wiki/Rezeptfreie_abnehmpillen_Wirksamkeit_Risiken_sinnvolle_Alternativen

sports and steroids

References:

https://pattern-wiki.win/wiki/Brleur_naturel_de_graisse_efficacit_choix

References:

How do you play roulette

References:

https://telegra.ph/Candy-Casino-Review-Expert–Player-Ratings-2026-01-26-2

References:

Coconut creek casino

References:

https://yogicentral.science/wiki/Check_a_website_for_risk_Check_if_fraudulent_Website_trust_reviews_Check_website_is_fake_or_a_scam

References:

Texas tea slots

References:

https://chessdatabase.science/wiki/Privacy_Policy

Reading your article helped me a lot and I agree with you. But I still have some doubts, can you clarify for me? I’ll keep an eye out for your answers.

References:

Majestic pines casino

References:

https://ai-db.science/wiki/Candy96_Online_Casino_Australia_100_Welcome_Bonus_and_Other_Bonuses

References:

Monte casino south africa

References:

https://www.garagesale.es/author/sampanlunch0/

References:

Talking stick casino

References:

https://peatix.com/user/28795007

References:

Mulvane casino

References:

https://clinfowiki.win/wiki/Post:Infinity_Game_Table_32

References:

Grand river casino

References:

https://ai-db.science/wiki/Candy_Casino_Built_Around_Flexible_Payments_Not_Big_Cashouts

are all steroids illegal

References:

https://yogicentral.science/wiki/Quels_sont_les_10_meilleurs_coupefaim_naturels

muscle pills that work

References:

https://p.mobile9.com/ravenpike3/

how expensive are steroids

References:

http://community.srhtech.net/user/weightlevel5

strongest steroid on the market

References:

http://millippies.com/members/okraleek8/activity/66142/

References:

Alton belle casino

References:

https://skitterphoto.com/photographers/2191039/demant-schack

References:

Quest casino

References:

https://www.divephotoguide.com/user/holeswamp8

References:

Paddypower casino

References:

https://p.mobile9.com/holecouch4/

References:

Newyork newyork casino

References:

https://www.google.com.gi/url?q=https://online-spielhallen.de/1red-casino-auszahlung-dein-umfassender-ratgeber/

References:

Casino auto sales

References:

http://downarchive.org/user/twistgrape9/

References:

Jouer au casino

References:

https://trade-britanica.trade/wiki/Kann_ich_mein_Geld_bei_888_Casino_zurckbekommen

References:

Casino canberra

References:

https://prpack.ru/user/alibiliquid82/

References:

Casino bonus

References:

https://schoolido.lu/user/risejelly06/

References:

Closest casino to atlanta

References:

https://pediascape.science/wiki/The_Best_PayID_Casinos_in_Australia_2025

best legal pre workout

References:

https://baby-newlife.ru/user/profile/437811

best steroid on the market

References:

https://forum.issabel.org/u/spleentoilet29

best cutting cycle for men

References:

https://prpack.ru/user/hallbeech61/

References:

St louis casinos

References:

https://pattern-wiki.win/wiki/PayID_Casinos_Australia_2026_Find_Best_PayID_Casinos

References:

Merkur online casino

References:

https://schoolido.lu/user/vinylpisces19/

best muscle enhancers

References:

http://downarchive.org/user/weeksun9/

online

top 10 casinos in the united states

casino las vegas bonus code

Your article helped me a lot, is there any more related content? Thanks!

betmgm Georgia betmgm Louisiana betmgm Alabama

legal steroids to gain weight

References:

https://werner-mcclain.thoughtlanes.net/acheter-hgh-meilleur-prix-livraison-rapide

real steroids for sale online

References:

https://opensourcebridge.science/wiki/Tren_E_vs_Tren_Ace

legal steroid supplements

References:

https://hamann-mclean-3.thoughtlanes.net/les-bruleurs-de-graisse-sont-ils-efficaces-1770324770

safe steroids for bodybuilding

References:

https://firsturl.de/kw8Yt5d

consequences for athletes who take steroids|acybgntie7watl3mow2zxra1ratkz_cmaq:***

References:

https://nerdgaming.science/wiki/Meilleur_brleur_de_graisse_en_2025_lequel_choisir_Comparatif_Avis

describe the clinical appearance of the following variations in stature

References:

https://www.24propertyinspain.com/user/profile/1370791

how much steroids to take

References:

https://firsturl.de/Cy1cUqR

anabolic steroids statistics

References:

https://bbs.pku.edu.cn/v2/jump-to.php?url=https://lifesbestmedicine.com/pages/comprar_dianabol_3.html

buy illegal steroids

References:

https://dokuwiki.stream/wiki/Buy_Anavar_A_Comprehensive_Guide_to_Purchasing_Oxandrolone

after stopping steroids

References:

http://pattern-wiki.win/index.php?title=myersmohammad9564

nih builders

References:

https://socialisted.org/market/index.php?page=user&action=pub_profile&id=316277

steroids dbol

References:

https://lovebookmark.date/story.php?title=m%EF%BF%BDdicaments-pour-maigrir-toutes-les-principales-pilules-minceur

steroid side effects in males

References:

https://rentry.co/4m8b2yod

best legal steriod

References:

https://mozillabd.science/wiki/Die_besten_Appetitzgler_und_wie_sie_eine_effektive_Gewichtsabnahme_untersttzen

anabolic steroid prescription

References:

https://onlinevetjobs.com/author/rabbitcable8/

steroids trenbolone

References:

https://timeoftheworld.date/wiki/Is_Anavar_Legal_in_the_U_S_and_Oklahoma

how does winstrol work

References:

https://bookmarkingworld.review/story.php?title=appetitzuegler-translation-from-german-into-english-pons

anavar steroid com

References:

https://santiago-bowden-3.blogbright.net/ozempic-une-pilule-pour-maigrir

steroid medication

References:

https://king-wifi.win/wiki/Top_3_meilleures_pilule_pour_maigrir_en_2026

Dive into the atmosphere of luxury and excitement. In crowncoincasino, popular slots from leading providers are available. Boost your bankroll with bonuses!

rivers casino

References:

https://socialbookmark.stream/story.php?title=trick-to-win-at-top-australian-pokies

leelanau sands casino

References:

http://dudoser.com/user/laughgold35/

slotland no deposit bonus codes

References:

https://freebookmarkstore.win/story.php?title=140-no-deposit-bonuses-for-aussies-free-spins-cash-offers

live casino

References:

https://instapages.stream/story.php?title=slots-free-spins-no-deposit

william hill mobile casino

References:

https://www.instapaper.com/p/17488900

Spin into pure joy with Sweet Bonanza — where wins pay in any position and cascades keep coming! Unlock sweet bonanza max win free spins packed with 10x–100x bombs. Sweet success awaits!

hollywood casino ms

References:

https://www.bidbarg.com/legal/user/sailorwolf94

mono wind casino

References:

https://seamatch31.werite.net/volt-casino-no-deposit-bonus-codes-for-free-spins-2026

hollywood casino maryland

References:

https://www.bandsworksconcerts.info:443/index.php?fendercornet1

hollywood casino tunica

References:

https://socialisted.org/market/index.php?page=user&action=pub_profile&id=375219

online casino malaysia

References:

https://oren-expo.ru/user/profile/894837

snoqualmie casino

References:

https://hopkins-bertram-2.hubstack.net/progressive-jackpots-guide-2026-win-big-at-online-pokies

george thorogood bad to the bone

References:

https://www.swinarski.org/page1.php?messagepage=70807&messagePage=

pioneer casino laughlin

References:

http://fprints.com.ua/user/homeitaly0/

canadian gaming summit

References:

https://www.instapaper.com/p/17489706

android spinner style

References:

https://molchanovonews.ru/user/organbox8/

mega casino

References:

https://molchanovonews.ru/user/deathduck8/

silver reef casino

References:

https://sundaynews.info/user/turkeyhelmet7/

casino la toja

References:

https://raindrop.io/eventlead43/deleurannoel2475-67361934

pink floyd live 8

References:

https://numberfields.asu.edu/NumberFields/show_user.php?userid=6539484

isle of capri florida

References:

http://lida-stan.by/user/wordcolumn03/

hollywood casino toledo ohio

References:

https://p.mobile9.com/veintax87/

high 5 casino games

References:

https://socialbookmark.stream/story.php?title=australia-native-multicultural-immigration

Charge your chance at casino immortality. aristocrat buffalo slot brings Aristocrat’s wilds, free spins, and golden jackpots eternal. Play today!

blackjack com

References:

https://reza-razavi.de/2021/09/

blackjack trainer

References:

https://uttarvanai.com/archives/33042

new online casino

References:

https://arkapadide.com/herbal-extracts/

%random_anchor_text%

References:

https://pikidi.com/seller/profile/chainvessel6

%random_anchor_text%

References:

https://milsaver.com/members/shellfrench0/activity/3494578/

the casino

References:

https://vivek-desai.com/pages/page-left-sidebar/

Chumba Casino — where players win real money without ever depositing. Grab your macumba welcome offer and start playing the best games now!

clam casino

References:

https://innovativeforge.com/exploring-new-horizons-adventures-await/

stake live betting Originals are — Crash, Plinko, Mines, Dice and more. Combine them with the best slots and live dealers online. Your next big win is one click away.

anabolic steroids for sale online

References:

https://peters-yde.technetbloggers.de/what-is-clenbuterol

DraftKings casino Pennsylvania Casino: Where luck meets value. Play $5 today and claim 500 spins on top slots with up to $1,000 lossback safety. The best just got better!

Original nebo generikum? U nas mate oboji za nejlepsi cenu

https://opravdovalekarna.cz

Upon the millions delightful colossal on fanduel casino New Mexico – the #1 tangible in dough casino app in America.

Reach your $1000 TEASE IT AGAIN honorarium and turn every relate, хэнд and rolling into legitimate coin of the realm rewards.

Irresponsibly payouts, immense jackpots, and non-stop effect – download FanDuel Casino now and start playing like a pro today!

References:

Old second neteller

References:

https://www.jakdangso.kr/midea/?bmode=view&idx=163467897

Unlock endless possibilities at Betano Casino https://betanogame.org/. Enjoy a generous €500 bonus and spin the reels on the latest hits. Fast deposits, instant withdrawals and top-tier security – Betano has it all.

References:

Maryland casino live

References:

https://pad.stuve.uni-ulm.de/s/iYKU13DAFx

References:

Hard rock casino cleveland

References:

https://p.mobile9.com/steppurple0/

References:

Casinos en mexico

References:

http://gojourney.xsrv.jp/index.php?startlift6

References:

Route 66 casino

References:

https://nicorgan8.werite.net/welcome-bonus-free-spins-slots-and-live-dealer-games

References:

New online casinos

References:

https://www.folkd.com/submit/www.footballzaa.com/out.php?url=dreevoo.com/profile.php?pid=1306051/

References:

Casino aachen

References:

https://bookmarkingworld.review/story.php?title=promotions-6

xn88 app sử dụng công nghệ truyền tải hình ảnh 4K cho các sảnh Casino, mang lại hình ảnh sắc nét và chân thực như đang ở sòng bạc thật. TONY03-18O

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://www.binance.com/register?ref=JW3W4Y3A

References:

What can steroids do to your body

References:

http://47.109.128.105:3001/xdhlavada25852

References:

Designer steroids list

References:

https://gitlab.cranecloud.io/bette41111009/bette2010/-/issues/1

No Mostbet vocГЄ recebe 100% de bГґnus + 150 free spins para arrasar nos jogos – https://mostbetpt.pro/mostbet-app/ , Mostbet: diversГЈo, adrenalina e recompensas na medida certa .

References:

Kai greene before steroids

References:

https://www.heldenausglas.de/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_35205740&path=&frame=STRATP_com_cm4all_wdn_Flatpress_35205740?x=entry:entry220124-204715%3Bcomments:1

References:

Liquid dbol dosage

References:

https://community.decentrixweb.com/index.php/question/your-path-from-bachelor-of-hospitality-management-to-career-success-hotel-front-desk-job-requirements-revenue-management-in-hotel-industry-7/

References:

The best muscle building pills

References:

https://sommer-architekt-warstein.de/VPB-Expertenrat;focus=TKOMSI_com_cm4all_wdn_Flatpress_22800952&path=?x=entry:entry251008-112142%3Bcomments:1

References:

Heavy r illegal site

References:

https://www.ringfloriangeyer.de/Startseite/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_11083477&frame=STRATP_com_cm4all_wdn_Flatpress_11083477?x=entry:entry220311-150819;comments:1

References:

Short term steroid side effects

References:

https://www.nemusic.rocks/rodrickcannon

Spin until the universe owes you an apology – https://xnortriptyline.com , Tonight the house is the underdog story .

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

References:

Winstrol steroid before and after

References:

https://itkvariat.com/user/cutzipper7/

References:

Someone who takes steroids is risking which of the following outcomes?

References:

https://telegra.ph/7-best-sites-to-buy-testosterone-online-in-2026-03-22

References:

Gsn casino games

References:

https://md.un-hack-bar.de/s/OY0gO7V26V

References:

Grand casino

References:

https://xn--41-4lcpj.xn--j1amh/user/mexicoeight99/

References:

Mass pills

References:

https://www.alpinfitness.com/BLOG/index.php/;focus=W4YPRD_com_cm4all_wdn_Flatpress_3516570&path=&frame=W4YPRD_com_cm4all_wdn_Flatpress_3516570?x=entry:entry161223-164703%3Bcomments:1

References:

How to make your own steroids from scratch

References:

http://www.ofrecklessnessandwater.com/blog/index.php/;focus=W4YPRD_com_cm4all_wdn_Flatpress_5487094&path=?x=entry:entry210102-180948%3Bcomments:1

References:

Long term side effects of corticosteroids

References:

https://www.kraftplatz-weibel.ch/blog/index.php/;focus=HSTPTP_com_cm4all_wdn_Flatpress_9497677&path=&frame=HSTPTP_com_cm4all_wdn_Flatpress_9497677?x=entry:entry240518-210038%3Bcomments:1

References:

Anabolic herbs

References:

https://xn--bw-mlhausen-whb.de/STARTSEITE/index.php/;focus=STRATP_com_cm4all_wdn_Flatpress_46252435&frame=STRATP_com_cm4all_wdn_Flatpress_46252435?x=entry:entry241104-234544;comments:1

References:

Dianabol illegal

References:

https://judith-ricklin.ch/Blog/index.php/;focus=HSTPTP_com_cm4all_wdn_Flatpress_6019167&frame=HSTPTP_com_cm4all_wdn_Flatpress_6019167?x=entry:entry200615-184425;comments:1

References:

Steroids bodybuilding

References:

https://yourclipz.com/@jonah271109086?page=about

References:

Bodybuilding stack

References:

https://git.wisder.net/felicitas38a90

References:

Should steroids be legalized

References:

https://www.udrpsearch.com/user/roofskiing02

References:

Side effects of anabolic steroids include quizlet

References:

https://git.dieselor.bg/laceythorne706

References:

Most potent anabolic steroid

References:

https://www.cives.pl/amyxpx60605553

References:

Meskwaki casino

References:

https://classifieds.ocala-news.com/author/flutevalley33

References:

Buying steroids

References:

https://git.binarycat.org/eddiecormack96

References:

Sterioid

References:

http://zzdgitea.stnav.com/dorotheaxzs446

References:

Buy anabolic steroids with credit card

References:

https://git.scinalytics.com/nannettegagai

References:

Dianabol cycle for sale

References:

http://139.196.103.114:18084/calebtrudel871

References:

Pockie ninja 2

References:

https://gpsites.win/story.php?title=play-top-slot-games-with-bonuses

References:

Testosteron steigern Hausmittel

References:

http://amur.1gb.ua/user/middlemeat46/

References:

Cholesterin Testosteronproduktion

References:

https://pad.stuve.de/s/7gpCCGrJe

References:

Does steroids

References:

http://66.179.208.56:3001/bradymcgovern/www.securityprofinder.com2010/wiki/On-Orthorexia-Nervosa%3A-A-Systematic-Review-of-Reviews

References:

Gnc natural whey protein

References:

http://gitlab.alpaedu.co.kr:8000/monserrateopp8

References:

Medicine for bodybuilding without side effects

References:

http://Vivefive.sakura.ne.jp/aska/aska.cgi

References:

Supplements to build muscle fast gnc

References:

https://tripleoggames.com/employer/exogenous-testosterone-enhances-cortisol-and-affective-responses-to-social-evaluative-stress-in-dominant-men/

References:

Dianabol injections for sale

References:

https://git.dinsor.co.th/hai47438312891

References:

What are the risks of using anabolic steroids

References:

https://raimusic.vn/sherryvenuti5

References:

What is the strongest steroid

References:

http://66.179.208.56:3001/jaquelineheide/3597062/wiki/Vegan-Men%3A-More-Testosterone-But-Less-Cancer

References:

What happens when you stop taking steroids

References:

https://git.opnkty.uk/andresgatlin95/124.71.197.1097304/wiki/Hormone-Therapy-for-Breast-Cancer-in-Men-American-Cancer-Society

References:

How to take anadrol properly

References:

http://webmail.m.tshome.co.kr/gnuboard5/bbs/board.php?bo_table=0322166142&wr_id=1045

References:

Is there a safe way to take steroids

References:

https://www.ozodagon.com/index.php?subaction=userinfo&user=foxstamp8

References:

Besten Testosteron Tabletten

References:

http://cqr3d.ru/user/coachbeggar67/

Pharmacie Г votre service : soins, bien-ГЄtre et disponibilitГ© 7 jours sur 7 – https://www.pharmacie-passamainty.com/mentions-legales/ , Votre partenaire santГ© proche de chez vous et proche de vos besoins .

References:

Anabolic definition

References:

https://molchanovonews.ru/user/syriadress0/

References:

Best steroid book

References:

https://schoolido.lu/user/bullclaus89/

References:

High testosterone joint pain

References:

https://md.swk-web.com/s/zUjcoXZzP

References:

Best stack supplements get ripped

References:

https://fkwiki.win/wiki/Post:Warum_stndiger_Heihunger_entsteht_und_was_wirklich_hilft

legal testosterone injections

References:

https://lichnyj-kabinet-vhod.ru/user/startporter5/

References:

Legal oral steroids

References:

https://www.blurb.com/user/sofastock0

References:

Taking steroids and not working out

References:

https://digitaltibetan.win/wiki/Post:Buy_Testosterone_Trenbolone_Online_from_Trenboloneusa_com

References:

Legalsteroids.com

References:

https://travelersqa.com/user/bongouganda37

References:

Can anabolic steroids cause cancer

References:

https://lovewiki.faith/wiki/Trenbolone_Acetate_Cycle_The_Game_Changing_Compound

References:

Steroid.com reviews

References:

https://wilson-mckenzie-5.thoughtlanes.net/anabolic-steroid-wikipedia

References:

How do steroids affect your body

References:

https://able2know.org/user/bumperunit20/

References:

Do bodybuilders die young

References:

https://enouvelles.space/item/442658

References:

Legit steroids online

References:

http://moonland.com/members/cerealyak29/activity/753918/

References:

Steroids what do they do

References:

https://telegra.ph/Clenbuterol-40-mcg-50-tabs-02-04

References:

Extreme steroid use

References:

https://sciencebookmark.top/item/325751

References:

Anabolic steroid types

References:

https://graph.org/Natural-Appetite-Suppressants-in-Weight-Loss-02-05

References:

Craze pre workout review

References:

https://molchanovonews.ru/user/silicaapple61/

References:

Anabolic steroids body building

References:

https://yogaasanas.science/wiki/Buy_Trenbolone_Acetate_USA_Delivery

References:

Can steroids help you lose weight

References:

https://monjournal.xyz/item/327211

References:

Legal fat burning steroids

References:

https://mmcon.sakura.ne.jp:443/mmwiki/index.php?kitedance0

References:

Any of these

References:

https://newsagg.site/item/442185

References:

Buying steroids online legal

References:

https://opensourcebridge.science/wiki/Steroid_use_is_widespread_and_its_increasingly_dangerous

References:

Trusted steroid sites

References:

https://enregistre-le.top/item/444524

References:

How much do anabolic steroids cost

References:

https://moparwiki.win/wiki/Post:Is_It_Worth_The_Risk_Trenbolone_Benefits_And_Side_Effects

References:

Steroids supplements

References:

https://www.udrpsearch.com/user/brushuganda19

References:

The effects of steroids

References:

https://topspots.cloud/item/443337

References:

Best legal testosterone

References:

https://pattern-wiki.win/wiki/Trenbolone_Enanthate_200mg_ml_ZPHC_10ml_Vial_USA_Domestic

References:

How to take steroids without side effects

References:

https://ccsakura.jp:443/index.php?golfcamp8

References:

Best supplement stack for muscle gain

References:

https://www.udrpsearch.com/user/brushuganda19

References:

Online pharmacy anabolic steroids

References:

https://mmcon.sakura.ne.jp:443/mmwiki/index.php?brushpig47

References:

Steroids types

References:

https://imoodle.win/wiki/Clenbuterol_Nebenwirkung_Wechselwirkung

References:

Which of the following has been found to be a side effect of anabolic steroid use?

References:

https://bookmarkzones.trade/story.php?title=trenbolone-the-ultimate-guide-to-uses-benefits-and-side-effects

References:

Where can i buy anavar legally

References:

http://www.annunciogratis.net/author/diggerbrain79

References:

Steroids negative effects

References:

https://krabbe-doyle-2.mdwrite.net/acheter-trenbolone-en-france-et-paris-trenbolone-a-bas-prix

References:

Why is steroid use among athletes dangerous to their health

References:

https://algowiki.win/wiki/Post:Top_6_Best_Tren_Supplements_in_2026

References:

What is a possible side effect as a result of the presence of anabolic steroids in male users?

References:

https://pattern-wiki.win/wiki/Wo_kann_man_Steroide_sicher_und_legal_kaufen

References:

Online Casino Echtgeld Sofortüberweisung

References:

https://hack.allmende.io/s/YDccyfDj7

References:

Online Casino Echtgeld Poker

References:

https://wolff-diaz-2.mdwrite.net/alle-top-anbieter-im-uberblick

References:

Steroids and weight loss

References:

https://coolpot.stream/story.php?title=approved-dianabol-for-sale-usa-buy-dianabol-online

References:

Steroid post cycle treatment

References:

https://firsturl.de/abt1c89

References:

Online Casino Echtgeld Gewinn

References:

http://dudoser.com/user/ideaankle5/

References:

Bestes online casino echtgeld

References:

https://dreevoo.com/profile.php?pid=1476396

References:

Echtgeld Casino Österreich

References:

https://www.youtube.com/redirect?q=https://de.trustpilot.com/review/owowear.de

References:

Casino goa

References:

https://zenwriting.net/handlepilot98/beste-online-spielothek-125-freispiele-ab-1-einzahlung-100-legal

References:

Choctaw casinos

References:

https://jackangel.com/members/daisybrush99/activity/136024/

References:

Echtgeld casino legal in deutschland

References:

https://squareblogs.net/daisybird09/top-10-die-besten-android-casino-echtgeld-apps-2026

References:

Körpereigenes Testosteron steigern

References:

https://timeoftheworld.date/wiki/Testosteron_Pflaster_Kaufen_Vergleich

References:

Genotropin kaufen

References:

https://vang-evans-5.federatedjournals.com/wachstumshormon-kur-plan-and-wirkung

References:

What does steroids do to the body

References:

https://argrathi.stars.ne.jp:443/pukiwiki/index.php?clarknicolajsen470615

References:

Best steroid for lean muscle

References:

https://hackmd.okfn.de/s/BkjbVMa3-g

References:

Fastest muscle building supplement gnc

References:

https://www.investagrams.com/Profile/kaplan3927287

References:

Long term steroid effects

References:

https://aryba.kg/user/soyincome7/

References:

Casino bet365

References:

https://link.hr-adsys.de/?t=website&url=aHR0cDovL1d3dy5haWtpLWV2b2x1dGlvbi5qcC95eS1ib2FyZC95eWJicy5jZ2k/bGlzdD10aHJlYWQ&id==NjY2MDU=

References:

Thunderstruck drinking game

References:

https://szybcypoland.pl/future-sounds-emerging-trends-in-dj-culture/

References:

Longhorn casino

References:

https://gitea.personalsoftware.space/sadyen1841457

References:

Isle casino pompano

References:

https://iraqitube.com/@meitressler568?page=about

References:

Amex usa

References:

https://graph.org/Lucky-Green-Casino-Review-Slot-Games-and-Bonus-Guide-04-20

References:

Crown https://graph.org/Level-Up-Casino-Pro-Strategies-for-Bigger-Wins-04-20 mobile app

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me.

References:

Fremont street casinos

References:

https://casino-in-portuguese.online-spielhallen.de/

References:

Oberhausen

References:

https://casino-gratis-guthaben.online-spielhallen.de/

References:

Leverkusen

References:

https://game-show-network-casino.online-spielhallen.de/

References:

Choctaw casino durant

References:

https://graph.org/Which-Slot-Machine-Is-Most-Likely-To-Win-04-27

Your point of view caught my eye and was very interesting. Thanks. I have a question for you.

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://accounts.binance.com/register/person?ref=QCGZMHR6

References:

Spa brochure

References:

http://gbtk.com/bbs/board.php?bo_table=main4_4&wr_id=369207

References:

Bc casinos

References:

https://deltasongs.com/roseannehewlet

References:

Lucky nugget casino

References:

https://candidates.giftabled.org/employer/ignition-casino-bonus-codes-review-updated/

References:

Fitzgerald casino tunica

References:

https://precisionscans.net/employer/best-payid-casinos-in-australia-top-list-for-may-2026/

References:

Kickapoo lucky eagle casino

References:

https://choosy.cc/@porfirioordone

References:

Roulette board https://firsturl.de/JYq396m

References:

Taj mahal casino https://www.udrpsearch.com/user/garagepair8

References:

Spirit mountain casino oregon http://202.53.128.110/home.php?mod=space&uid=1009150

References:

Native american casinos http://www.bmw-workshop.com/member.php?action=profile&uid=38623

Fortune Gods de novo? Os regulares não para de postar.

References:

All slots casino mobile https://bookmarkingworlds.com/News/check-our-list/

References:

Rising star casino https://vusr.net/members/eraleaf36/activity/89216/

References:

Cool gaming names https://marvelswiki.site/wiki/Play_Online_Pokies_with_Fast_Australian_Payouts

купить спецтехнику [url=http://tech-group.com.ua]http://tech-group.com.ua[/url]

тойота сервис в москве [url=yourmoscow.ru/posts/pokupka-avtomobilja-toiota-s-probegom-chek-list-proverki-i-rekomendacii-po-obsluzhivaniyu.html]тойота сервис в москве[/url]

спецтехника Volvo [url=https://tech-group.com.ua]https://tech-group.com.ua[/url]

букмекерские крипто конторы [url=https://forumsilverstars.forum24.ru/?1-9-0-00000118-000-0-0]букмекерские крипто конторы[/url]

букмекерские конторы Литвы [url=https://glen-jitterbug-fd8.notion.site/359b8cddbfaf80d98440c11f3dd12b14]букмекерские конторы Литвы[/url]

сервисный центр тойота [url=http://proalbea.ru/tojota-v-rossii-posle-2022-goda-kakie-modeli-ostalis.html]http://proalbea.ru/tojota-v-rossii-posle-2022-goda-kakie-modeli-ostalis.html[/url]

спецтехника Volvo [url=http://www.tech-group.com.ua]http://www.tech-group.com.ua[/url]

ставки на спорт Литвы [url=https://glen-jitterbug-fd8.notion.site/359b8cddbfaf80d98440c11f3dd12b14]ставки на спорт Литвы[/url]

рейтинг крипто БК [url=https://skoleoz.borda.ru/?1-2-0-00002693-000-0-0]рейтинг крипто БК[/url]

сервис тойота в москве [url=https://www.techautoport.ru/news/sezonnoe-to-toyota-kakie-raboty-obyazatelno-vypolnyat-vesnoy-i-osenyu-dlya-nadezhnosti-avtomobilya.html]https://www.techautoport.ru/news/sezonnoe-to-toyota-kakie-raboty-obyazatelno-vypolnyat-vesnoy-i-osenyu-dlya-nadezhnosti-avtomobilya.html[/url]

Cansei do Lucky Neko essa semana.

ставки на спорт Литвы [url=https://glen-jitterbug-fd8.notion.site/359b8cddbfaf80d98440c11f3dd12b14]ставки на спорт Литвы[/url]

крипто букмекеры [url=https://4dkp.forum24.ru/?1-3-0-00000155-000-0-0]крипто букмекеры[/url]

купить спецтехнику Вольво [url=http://www.tech-group.com.ua]http://www.tech-group.com.ua[/url]

автосервис тойота [url=http://proalbea.ru/tojota-v-rossii-posle-2022-goda-kakie-modeli-ostalis.html]автосервис тойота[/url]

букмекерские конторы Литвы [url=https://medium.com/@vit.blagod/%D1%81%D1%82%D0%B0%D0%B2%D0%BA%D0%B8-%D0%BD%D0%B0-%D1%81%D0%BF%D0%BE%D1%80%D1%82-%D0%B2-%D0%BB%D0%B8%D1%82%D0%B2%D0%B5-%D0%BE%D1%81%D0%BE%D0%B1%D0%B5%D0%BD%D0%BD%D0%BE%D1%81%D1%82%D0%B8-%D1%80%D1%8B%D0%BD%D0%BA%D0%B0-%D0%B8-%D0%BF%D0%BE%D0%BF%D1%83%D0%BB%D1%8F%D1%80%D0%BD%D1%8B%D0%B5-%D0%BD%D0%B0%D0%BF%D1%80%D0%B0%D0%B2%D0%BB%D0%B5%D0%BD%D0%B8%D1%8F-702bcfa2a741]букмекерские конторы Литвы[/url]

Лучшие крипто букмекерские конторы [url=https://skoleoz.borda.ru/?1-2-0-00002693-000-0-0]Лучшие крипто букмекерские конторы[/url]

Volvo Украина [url=http://www.tech-group.com.ua]http://www.tech-group.com.ua[/url]

тойота сервис в москве [url=https://proalbea.ru/tojota-v-rossii-posle-2022-goda-kakie-modeli-ostalis.html]тойота сервис в москве[/url]

thailand phuket apartments for sale [url=apartments-for-sale-in-phuket-5.com]thailand phuket apartments for sale[/url]

Лучшие крипто букмекерские конторы [url=https://mymoscow.forum24.ru/?1-5-0-00003609-000-0-0]Лучшие крипто букмекерские конторы[/url]

кухни на заказ в санкт-петербурге [url=https://kuhni-spb-59.ru]https://kuhni-spb-59.ru[/url]

кухни на заказ в спб [url=https://kuhni-spb-61.ru]кухни на заказ в спб[/url]

заказать индивидуальную кухню [url=https://zakazat-kuhnyu-20.ru]заказать индивидуальную кухню[/url]

рулонные жалюзи купить в москве [url=https://rulonnye-shtory-s-elektroprivodom10.ru]рулонные жалюзи купить в москве[/url]

100cuci ios [url=100cuci-10.com]100cuci ios[/url]

apartments in phuket thailand for sale [url=https://apartments-for-sale-in-phuket-5.com]apartments in phuket thailand for sale[/url]

фанспорт букмекерская контора [url=http://www.bisound.com/forum/showthread.php?p=3167271&posted=1#post3167271]фанспорт букмекерская контора[/url]

заказать кухню в спб от производителя недорого [url=https://kuhni-spb-61.ru]заказать кухню в спб от производителя недорого[/url]

купить кухню на заказ спб [url=https://kuhni-spb-59.ru]https://kuhni-spb-59.ru[/url]

заказать кухню по индивидуальному проекту [url=https://zakazat-kuhnyu-20.ru]заказать кухню по индивидуальному проекту[/url]

100cuci official [url=https://www.100cuci-10.com]100cuci official[/url]

рулонные шторы на балконные окна [url=https://rulonnye-shtory-s-elektroprivodom10.ru]https://rulonnye-shtory-s-elektroprivodom10.ru[/url]

100cuci promo code [url=100cuci-7.com]100cuci promo code[/url]

сколько стоит нарколог на дом [url=https://narkolog-na-dom-voronezh-13.ru]сколько стоит нарколог на дом[/url]

investment apartments for sale in phuket [url=https://www.apartments-for-sale-in-phuket-5.com]investment apartments for sale in phuket[/url]

кухни на заказ от производителя [url=https://kuhni-spb-59.ru]кухни на заказ от производителя[/url]

кухни на заказ в спб от производителя [url=https://kuhni-spb-61.ru]кухни на заказ в спб от производителя[/url]

22bet букмекерская контора [url=https://masa.forum24.ru/?1-8-0-00001329-000-0-0]22bet букмекерская контора[/url]

сколько стоит заказать кухню по размерам [url=https://zakazat-kuhnyu-20.ru]https://zakazat-kuhnyu-20.ru[/url]

no deposit bonus malaysia [url=100cuci-10.com]no deposit bonus malaysia[/url]

какие бывают рулонные шторы [url=https://rulonnye-shtory-s-elektroprivodom10.ru]https://rulonnye-shtory-s-elektroprivodom10.ru[/url]

100cuci bonus [url=https://100cuci-7.com]100cuci bonus[/url]

нарколог на дом воронеж [url=https://narkolog-na-dom-voronezh-13.ru]нарколог на дом воронеж[/url]

кухни на заказ петербург [url=https://kuhni-spb-61.ru]кухни на заказ петербург[/url]

кухня по индивидуальному заказу спб [url=https://kuhni-spb-59.ru]кухня по индивидуальному заказу спб[/url]

сколько стоит заказать кухню по размерам [url=https://zakazat-kuhnyu-20.ru]https://zakazat-kuhnyu-20.ru[/url]

22bet ставки на спорт [url=https://airlady.forum24.ru/?1-7-0-00006686-000-0-0]22bet ставки на спорт[/url]

100cuci terbaru [url=http://www.100cuci-7.com]100cuci terbaru[/url]

рулонные шторы производство [url=https://rulonnye-shtory-s-elektroprivodom10.ru]https://rulonnye-shtory-s-elektroprivodom10.ru[/url]

thailand phuket apartments for sale [url=http://www.apartments-for-sale-in-phuket-5.com]thailand phuket apartments for sale[/url]

free kredit malaysia [url=http://www.100cuci-10.com]free kredit malaysia[/url]

нарколог на дом [url=https://narkolog-na-dom-voronezh-13.ru]нарколог на дом[/url]

заказать кухню в спб от производителя недорого [url=https://kuhni-spb-61.ru]заказать кухню в спб от производителя недорого[/url]

заказать кухню онлайн [url=https://zakazat-kuhnyu-20.ru]заказать кухню онлайн[/url]

кухни на заказ спб каталог [url=https://kuhni-spb-59.ru]кухни на заказ спб каталог[/url]

phuket condo for sale [url=apartments-for-sale-in-phuket-5.com]phuket condo for sale[/url]

готовые рулонные шторы купить в москве [url=https://rulonnye-shtory-s-elektroprivodom10.ru]готовые рулонные шторы купить в москве[/url]

100cuci [url=www.100cuci-10.com]100cuci[/url]

выезд нарколога на дом [url=https://narkolog-na-dom-voronezh-13.ru]выезд нарколога на дом[/url]

22bet официальный сайт [url=https://astana.forum24.ru/?1-5-0-00000336-000-0-0]22bet официальный сайт[/url]

нарколог на дом анонимно [url=https://narkolog-na-dom-voronezh-12.ru]нарколог на дом анонимно[/url]

Cashback sumiu. Abri ticket.

condos in phuket for sale [url=https://apartments-for-sale-in-phuket-4.com]condos in phuket for sale[/url]

нарколог на дом воронеж [url=https://narkolog-na-dom-voronezh-13.ru]нарколог на дом воронеж[/url]

100cuci no deposit [url=https://100cuci-7.com]100cuci no deposit[/url]

рулонные шторы с электроприводом купить в москве [url=https://elektricheskie-rulonnye-shtory99.ru]рулонные шторы с электроприводом купить в москве[/url]

Dois bônus seguidos no Caishen Wins, ambos uns 30x. Estranho.

нарколог на дом отзывы [url=https://narkolog-na-dom-voronezh-12.ru]нарколог на дом отзывы[/url]

Fim do mês. Travando o ROI.

кухни в спб от производителя [url=https://kuhni-spb-58.ru]кухни в спб от производителя[/url]

капельница после запоя цена [url=https://kapelnicza-ot-pokhmelya-samara-23.ru]капельница после запоя цена[/url]

100cuci pragmatic [url=http://www.100cuci-7.com]100cuci pragmatic[/url]

электропривод рулонных штор [url=https://elektricheskie-rulonnye-shtory99.ru]электропривод рулонных штор[/url]

рулонные шторы жалюзи на окна [url=https://avtomaticheskie-rulonnye-shtory50.ru]https://avtomaticheskie-rulonnye-shtory50.ru[/url]

100cuci welcome bonus [url=100cuci-8.com]100cuci welcome bonus[/url]

phuket villas for sale thailand [url=https://villas-for-sale-in-phuket-4.com]phuket villas for sale thailand[/url]

нарколог на дом [url=https://narkolog-na-dom-voronezh-12.ru]нарколог на дом[/url]

мебель для кухни спб от производителя [url=https://kuhni-spb-58.ru]https://kuhni-spb-58.ru[/url]

phuket condos for sale [url=https://apartments-for-sale-in-phuket-4.com]phuket condos for sale[/url]

сколько стоит капельница от похмелья [url=https://kapelnicza-ot-pokhmelya-samara-23.ru]https://kapelnicza-ot-pokhmelya-samara-23.ru[/url]

электрические рулонные жалюзи [url=https://elektricheskie-rulonnye-shtory99.ru]электрические рулонные жалюзи[/url]

References:

High limit blackjack https://profmustafa.com/@mapleburr03049?page=about

кухни на заказ санкт петербург от производителя [url=https://kuhni-spb-58.ru]https://kuhni-spb-58.ru[/url]

luxury villas in phuket for sale [url=https://villas-for-sale-in-phuket-4.com]luxury villas in phuket for sale[/url]

100cuci no deposit [url=100cuci-8.com]100cuci no deposit[/url]

нарколог на дом в воронеже [url=https://narkolog-na-dom-voronezh-12.ru]нарколог на дом в воронеже[/url]

рулонные шторы производство [url=https://rulonnye-elektroshtory.ru]https://rulonnye-elektroshtory.ru[/url]

капельница от запоя самара [url=https://kapelnicza-ot-pokhmelya-samara-23.ru]https://kapelnicza-ot-pokhmelya-samara-23.ru[/url]

apartments for sale thailand phuket [url=https://apartments-for-sale-in-phuket-4.com]apartments for sale thailand phuket[/url]

прокапаться от алкоголя в воронеже [url=https://kapelnicza-ot-pokhmelya-voronezh-14.ru]прокапаться от алкоголя в воронеже[/url]

вывод из запоя в стационаре в нижнем новгороде [url=https://vyvod-iz-zapoya-v-staczionare-nizhnij-novgorod-16.ru]https://vyvod-iz-zapoya-v-staczionare-nizhnij-novgorod-16.ru[/url]

villas for sale phuket thailand [url=https://villas-for-sale-in-phuket-4.com]villas for sale phuket thailand[/url]

trusted casino malaysia [url=http://100cuci-8.com]trusted casino malaysia[/url]

современные кухни на заказ в спб [url=https://kuhni-spb-58.ru]https://kuhni-spb-58.ru[/url]

круглосуточный вывод из запоя [url=https://vyvod-iz-zapoya-na-domu-sankt-peterburg-19.ru]круглосуточный вывод из запоя[/url]

роликовые шторы [url=https://elektricheskie-rulonnye-shtory99.ru]роликовые шторы[/url]

вызов нарколога на дом [url=https://narkolog-na-dom-voronezh-12.ru]вызов нарколога на дом[/url]

автоматические рулонные шторы на окна [url=https://rulonnye-elektroshtory.ru]автоматические рулонные шторы на окна[/url]

капельница от похмелья воронеж [url=https://kapelnicza-ot-pokhmelya-voronezh-14.ru]капельница от похмелья воронеж[/url]

вывод из запоя цены самара [url=https://kapelnicza-ot-pokhmelya-samara-23.ru]вывод из запоя цены самара[/url]

вывод из алкогольного запоя [url=https://vyvod-iz-zapoya-na-domu-sankt-peterburg-19.ru]https://vyvod-iz-zapoya-na-domu-sankt-peterburg-19.ru[/url]

investment apartments for sale in phuket [url=https://apartments-for-sale-in-phuket-4.com]investment apartments for sale in phuket[/url]

References:

Casino helsinki https://vila.go.ro/kristinalesche

вывод из запоя нижний новгород стационар [url=https://vyvod-iz-zapoya-v-staczionare-nizhnij-novgorod-16.ru]вывод из запоя нижний новгород стационар[/url]

рулонные шторы на кухню с балконом [url=https://elektricheskie-rulonnye-shtory99.ru]https://elektricheskie-rulonnye-shtory99.ru[/url]

рольшторы на окна купить в москве [url=https://rulonnye-elektroshtory.ru]рольшторы на окна купить в москве[/url]

кухни на заказ санкт петербург [url=https://kuhni-spb-58.ru]https://kuhni-spb-58.ru[/url]

100cuci free credit [url=www.100cuci-8.com]100cuci free credit[/url]

villas for sale in phuket island [url=https://villas-for-sale-in-phuket-4.com]villas for sale in phuket island[/url]

капельница от похмелья на дому [url=https://kapelnicza-ot-pokhmelya-voronezh-14.ru]капельница от похмелья на дому[/url]

вывод из запоя [url=https://vyvod-iz-zapoya-na-domu-sankt-peterburg-19.ru]вывод из запоя[/url]

капельница от похмелья [url=https://kapelnicza-ot-pokhmelya-samara-23.ru]https://kapelnicza-ot-pokhmelya-samara-23.ru[/url]

вывод из запоя спб [url=https://vyvod-iz-zapoya-na-domu-sankt-peterburg-19.ru]https://vyvod-iz-zapoya-na-domu-sankt-peterburg-19.ru[/url]

вывод из запоя в клинике [url=https://vyvod-iz-zapoya-v-staczionare-nizhnij-novgorod-16.ru]https://vyvod-iz-zapoya-v-staczionare-nizhnij-novgorod-16.ru[/url]

прокапаться от алкоголя нижний новгород [url=https://kapelnicza-ot-pokhmelya-nizhnij-novgorod-7.ru]прокапаться от алкоголя нижний новгород[/url]

тур спб [url=http://piter-na-teplohode.ru]тур спб[/url]

villas for sale in phuket [url=https://villas-for-sale-in-phuket-4.com]villas for sale in phuket[/url]

кухни на заказ в спб от производителя [url=https://kuhni-spb-57.ru]https://kuhni-spb-57.ru[/url]

капельница от запоя вызов [url=https://kapelnicza-ot-pokhmelya-voronezh-14.ru]капельница от запоя вызов[/url]

заказать кухню в спб от производителя [url=https://kuhni-spb-60.ru]заказать кухню в спб от производителя[/url]

скачать видео с ютуба на смартфон [url=https://skachat-video-s-youtube-9.ru]https://skachat-video-s-youtube-9.ru[/url]

скачать с ютюб [url=https://skachat-video-s-youtube-10.ru]https://skachat-video-s-youtube-10.ru[/url]

100cuci welcome bonus [url=https://100cuci-8.com]100cuci welcome bonus[/url]

готовые рулонные шторы купить в москве [url=https://elektricheskie-rulonnye-shtory99.ru]готовые рулонные шторы купить в москве[/url]

вывод из запоя капельница [url=https://kapelnicza-ot-pokhmelya-nizhnij-novgorod-7.ru]вывод из запоя капельница[/url]

гатчина вояж маршруты выходного [url=piter-na-teplohode.ru]гатчина вояж маршруты выходного[/url]

загрузчик видео с youtube [url=https://skachat-video-s-youtube-10.ru]https://skachat-video-s-youtube-10.ru[/url]

купить кухню на заказ в спб [url=https://kuhni-spb-57.ru]https://kuhni-spb-57.ru[/url]

производство кухонь в спб на заказ [url=https://kuhni-spb-60.ru]производство кухонь в спб на заказ[/url]

скачать видео ютуб 1080 [url=https://skachat-video-s-youtube-9.ru]https://skachat-video-s-youtube-9.ru[/url]

сколько стоит нарколог на дом [url=https://narkolog-na-dom-voronezh-11.ru]https://narkolog-na-dom-voronezh-11.ru[/url]

капельница самара цена [url=https://kapelnicza-ot-pokhmelya-samara-29.ru]капельница самара цена[/url]

вывод из запоя на дому спб [url=https://vyvod-iz-zapoya-na-domu-sankt-peterburg-19.ru]https://vyvod-iz-zapoya-na-domu-sankt-peterburg-19.ru[/url]

капельница от похмелья нижний новгород [url=https://kapelnicza-ot-pokhmelya-nizhnij-novgorod-7.ru]капельница от похмелья нижний новгород[/url]

рулонные жалюзи с электроприводом [url=https://elektricheskie-rulonnye-shtory99.ru]рулонные жалюзи с электроприводом[/url]

поехать в спб [url=https://www.piter-na-teplohode.ru]https://www.piter-na-teplohode.ru[/url]

прокапывание от алкоголя на дому [url=https://kapelnicza-ot-pokhmelya-voronezh-14.ru]прокапывание от алкоголя на дому[/url]

мебель для кухни спб от производителя [url=https://kuhni-spb-60.ru]мебель для кухни спб от производителя[/url]

кухня глория [url=https://kuhni-spb-57.ru]https://kuhni-spb-57.ru[/url]

скачать youtube видео [url=https://skachat-video-s-youtube-9.ru]скачать youtube видео[/url]

вывод из запоя стационар [url=https://vyvod-iz-zapoya-v-staczionare-nizhnij-novgorod-16.ru]вывод из запоя стационар[/url]

капельницы от запоя на дому самара [url=https://kapelnicza-ot-pokhmelya-samara-29.ru]капельницы от запоя на дому самара[/url]

капельница от запоя нижний новгород [url=https://kapelnicza-ot-pokhmelya-nizhnij-novgorod-7.ru]капельница от запоя нижний новгород[/url]

рулонные шторы на кухню с балконом [url=https://elektricheskie-rulonnye-shtory99.ru]https://elektricheskie-rulonnye-shtory99.ru[/url]

экскурсионные туры в петербург [url=www.piter-na-teplohode.ru]www.piter-na-teplohode.ru[/url]

сколько стоит капельница на дому [url=https://kapelnicza-ot-pokhmelya-voronezh-14.ru]сколько стоит капельница на дому[/url]

вывод из алкогольного запоя нарколог 24 [url=https://vyvod-iz-zapoya-na-domu-sankt-peterburg-20.ru]https://vyvod-iz-zapoya-na-domu-sankt-peterburg-20.ru[/url]

кухни на заказ от производителя [url=https://kuhni-spb-57.ru]https://kuhni-spb-57.ru[/url]

прокапаться от алкоголя самара цена [url=https://kapelnicza-ot-pokhmelya-samara-29.ru]прокапаться от алкоголя самара цена[/url]

вывод из запоя с выездом [url=https://vyvod-iz-zapoya-na-domu-ekaterinburg-28.ru]вывод из запоя с выездом[/url]

капельница после запоя [url=https://kapelnicza-ot-pokhmelya-nizhnij-novgorod-7.ru]капельница после запоя[/url]

вывод из запоя в спб [url=https://vyvod-iz-zapoya-na-domu-sankt-peterburg-21.ru]вывод из запоя в спб[/url]

наркологическая помощь на дому круглосуточно [url=https://narkolog-na-dom-nizhnij-novgorod-2.ru]https://narkolog-na-dom-nizhnij-novgorod-2.ru[/url]

капельница на дому сколько стоит [url=https://kapelnicza-ot-pokhmelya-voronezh-15.ru]капельница на дому сколько стоит[/url]

кухни от производителя спб недорого и качественно [url=https://kuhni-spb-57.ru]https://kuhni-spb-57.ru[/url]

санкт петербург тур выходного дня [url=http://www.piter-na-teplohode.ru]http://www.piter-na-teplohode.ru[/url]

скачать ролик с ютьюб [url=https://skachat-video-s-youtube-9.ru]https://skachat-video-s-youtube-9.ru[/url]

кухни на заказ спб каталог [url=https://kuhni-spb-60.ru]кухни на заказ спб каталог[/url]

прокапаться на дому цена [url=https://kapelnicza-ot-pokhmelya-samara-29.ru]прокапаться на дому цена[/url]

вывод из запоя недорого нарколог24 [url=https://vyvod-iz-zapoya-na-domu-sankt-peterburg-21.ru]вывод из запоя недорого нарколог24[/url]

капельница после запоя цена [url=https://kapelnicza-ot-pokhmelya-nizhnij-novgorod-7.ru]капельница после запоя цена[/url]

выведение из запоя на дому цена [url=https://vyvod-iz-zapoya-na-domu-ekaterinburg-28.ru]выведение из запоя на дому цена[/url]

выезд на дом капельница от запоя [url=https://kapelnicza-ot-pokhmelya-voronezh-15.ru]выезд на дом капельница от запоя[/url]

кухня на заказ спб [url=https://kuhni-spb-57.ru]кухня на заказ спб[/url]

вызвать нарколога на дом [url=https://narkolog-na-dom-nizhnij-novgorod-2.ru]вызвать нарколога на дом[/url]

автоматическая рулонная штора [url=https://elektricheskie-rulonnye-shtory99.ru]автоматическая рулонная штора[/url]

заказ кухни [url=https://kuhni-spb-60.ru]заказ кухни[/url]

скачать с ютуба в отличном качестве [url=https://skachat-video-s-youtube-9.ru]https://skachat-video-s-youtube-9.ru[/url]

вывод из запоя цена [url=https://vyvod-iz-zapoya-na-domu-sankt-peterburg-21.ru]вывод из запоя цена[/url]

прокапаться на дому нижний новгород [url=https://kapelnicza-ot-pokhmelya-nizhnij-novgorod-8.ru]прокапаться на дому нижний новгород[/url]

вывод из запоя на дому в екатеринбурге [url=https://vyvod-iz-zapoya-na-domu-ekaterinburg-28.ru]вывод из запоя на дому в екатеринбурге[/url]

нарколог выездной [url=https://narkolog-na-dom-nizhnij-novgorod-2.ru]нарколог выездной[/url]

рулонные шторы жалюзи на окна [url=https://elektricheskie-rulonnye-shtory99.ru]https://elektricheskie-rulonnye-shtory99.ru[/url]

скачат видео ютуб [url=https://skachat-video-s-youtube-11.ru]скачат видео ютуб[/url]

поставить капельницу от запоя [url=https://kapelnica-ot-zapoya-nizhnij-novgorod-8.ru]поставить капельницу от запоя[/url]

вызвать нарколога на дом воронеж [url=https://narkolog-na-dom-voronezh-10.ru]https://narkolog-na-dom-voronezh-10.ru[/url]